Huynh Toan Luu Duc, Foglia Matteo, Nasir Muhammad Ali, Angelini Eliana

WHU - Otto Beisheim School of Management (Germany), Chair of Behavioral Finance.

University of Economics Ho Chi Minh City (Vietnam), School of Banking.

J Econ Behav Organ. 2021 Aug;188:1088-1108. doi: 10.1016/j.jebo.2021.06.016. Epub 2021 Jun 19.

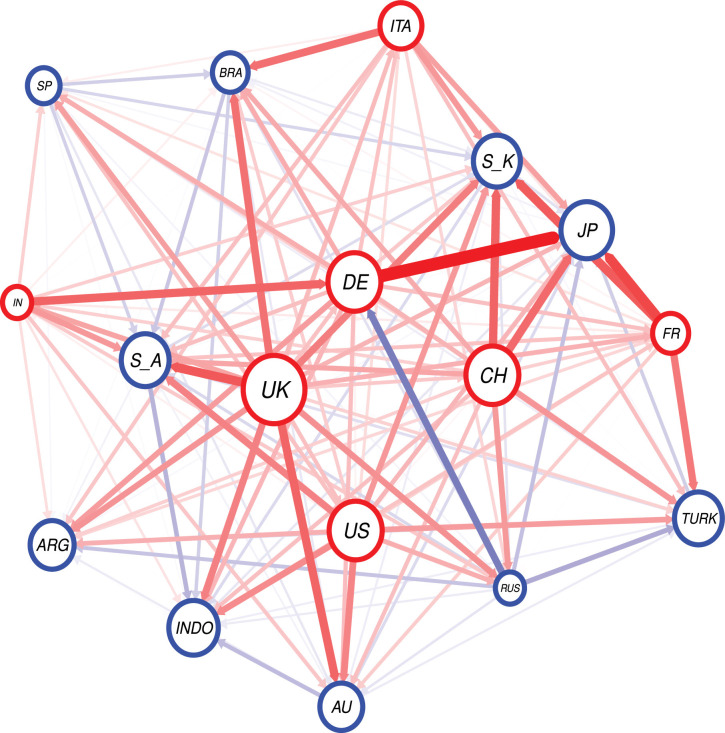

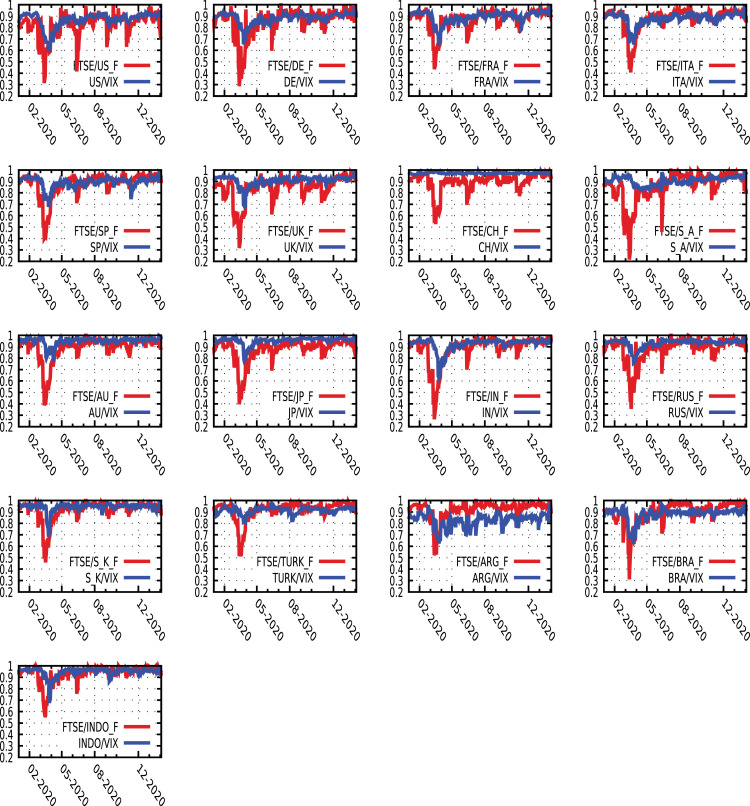

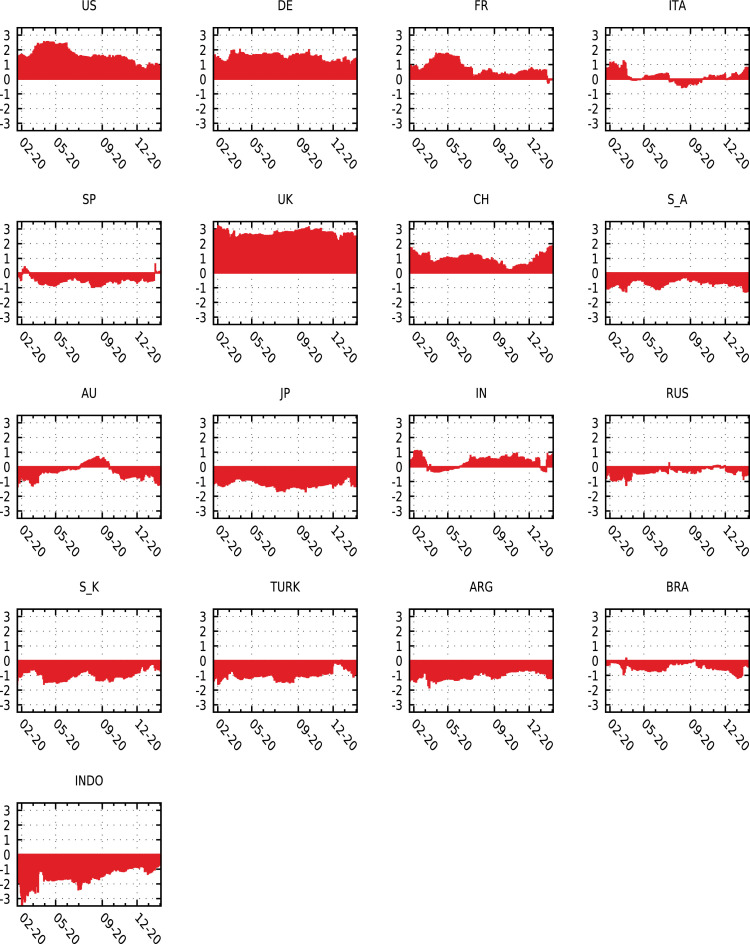

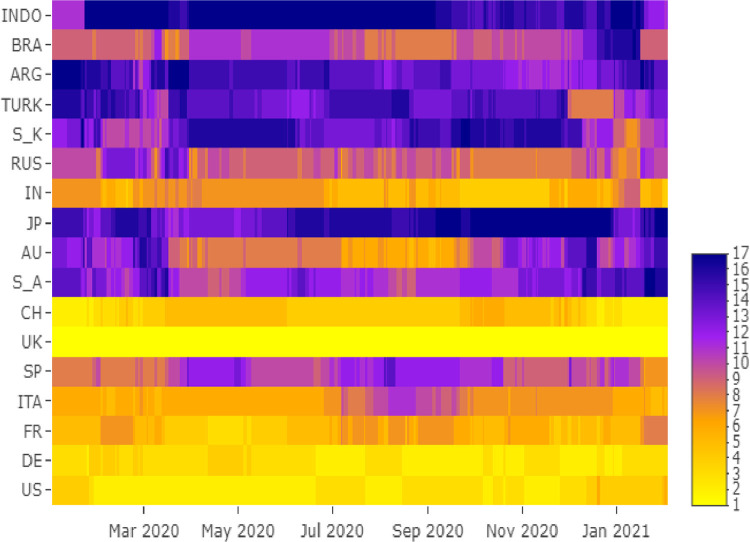

This paper proposes a new approach to estimating investor sentiments and their implications for the global financial markets. Contextualising the COVID-19 pandemic, we draw on the six behavioural indicators (media coverage, fake news, panic, sentiment, media hype and infodemic) of the 17 largest economies and data from January 2020 to February 2021. Our key findings, obtained using a time-varying parameter-vector auto-regression (TVP-VAR) model, indicate the total and net connectedness for the new index, entitled 'feverish sentiment'. This index provides us insight into economies that send or receive the sentiment shocks. The construction of the network structures indicates that the United Kingdom, China, the United States and Germany became the epicentres of the sentimental shocks that were transmitted to other economies. Furthermore, we also explore the predictive power of the newly constructed index on stock returns and volatility. It turns out that investor sentiment positively (negatively) predicts the stock volatility (return) at the onset of COVID-19. This is the first study of its kind to assess international feverish sentiments by proposing a novel approach and its impacts on the equity market. Based on empirical findings, the study also offers some policy directions to mitigate the fear and panic during the pandemic.

本文提出了一种估计投资者情绪及其对全球金融市场影响的新方法。结合新冠疫情背景,我们利用17个最大经济体的六个行为指标(媒体报道、假新闻、恐慌、情绪、媒体炒作和信息疫情)以及2020年1月至2021年2月的数据。我们使用时变参数向量自回归(TVP-VAR)模型得出的主要发现,表明了名为“狂热情绪”的新指数的总关联性和净关联性。该指数让我们深入了解了发送或接收情绪冲击的经济体。网络结构的构建表明,英国、中国、美国和德国成为了向其他经济体传播情绪冲击的中心。此外,我们还探讨了新构建的指数对股票回报和波动率的预测能力。结果表明,在新冠疫情初期,投资者情绪对股票波动率(回报)有正向(负向)预测作用。这是同类研究中首次通过提出一种新颖方法来评估国际狂热情绪及其对股票市场的影响。基于实证结果,该研究还提供了一些政策方向,以减轻疫情期间的恐惧和恐慌。