Sharma Gagan Deep, Tiwari Aviral Kumar, Jain Mansi, Yadav Anshita, Erkut Burak

University School of Management Studies, Guru Gobind Singh Indraprastha University, Sector 16 C, Dwarka, New Delhi, India.

Department of Finance and Economics, Rajagiri Business School, Rajagiri, Valley Campus, Kochi, India.

Heliyon. 2021 Feb 2;7(2):e06181. doi: 10.1016/j.heliyon.2021.e06181. eCollection 2021 Feb.

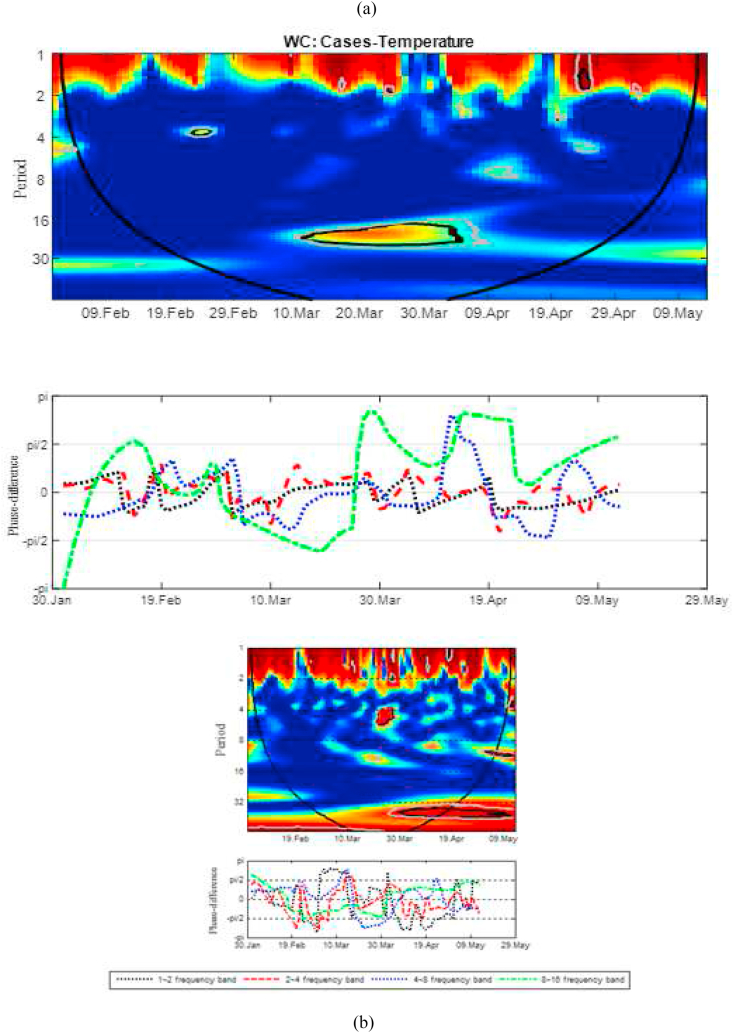

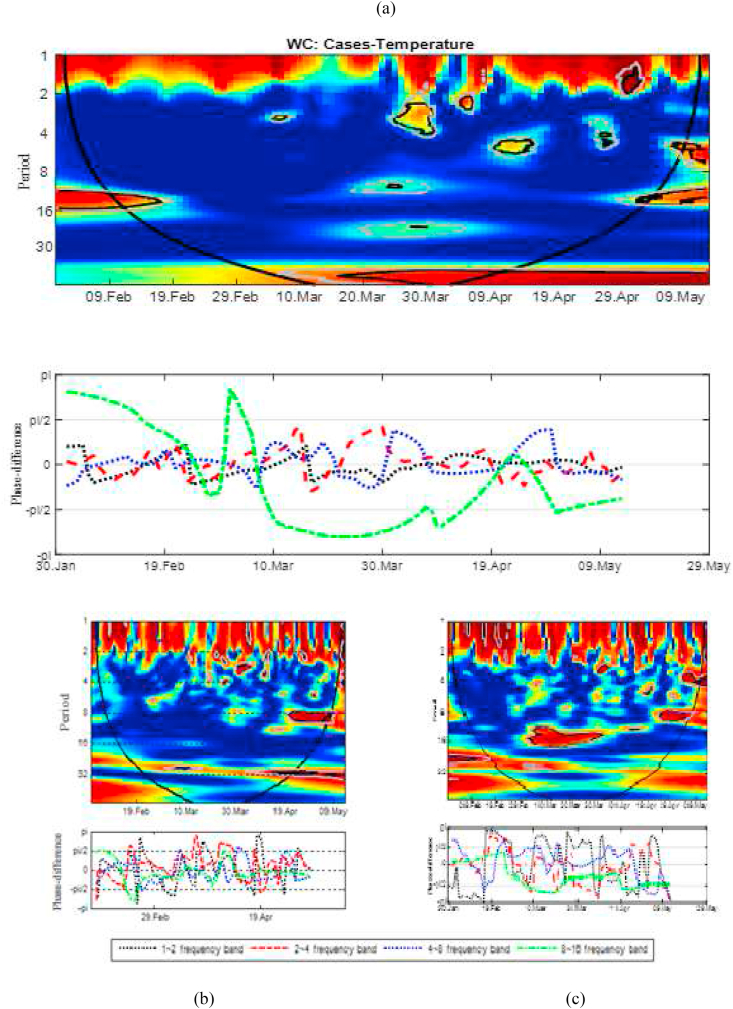

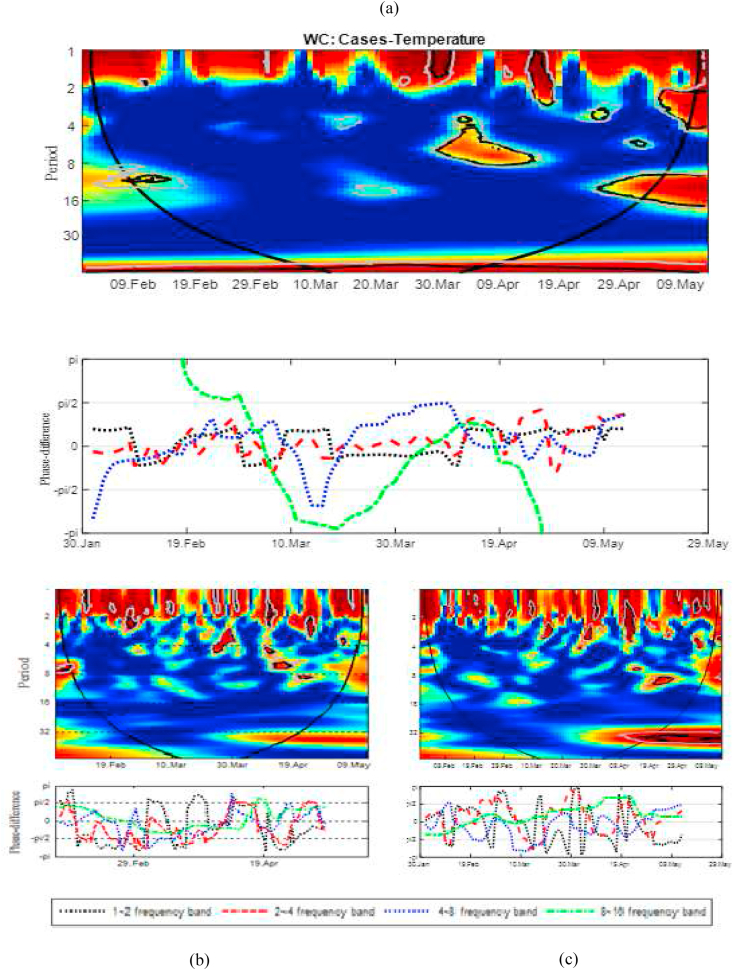

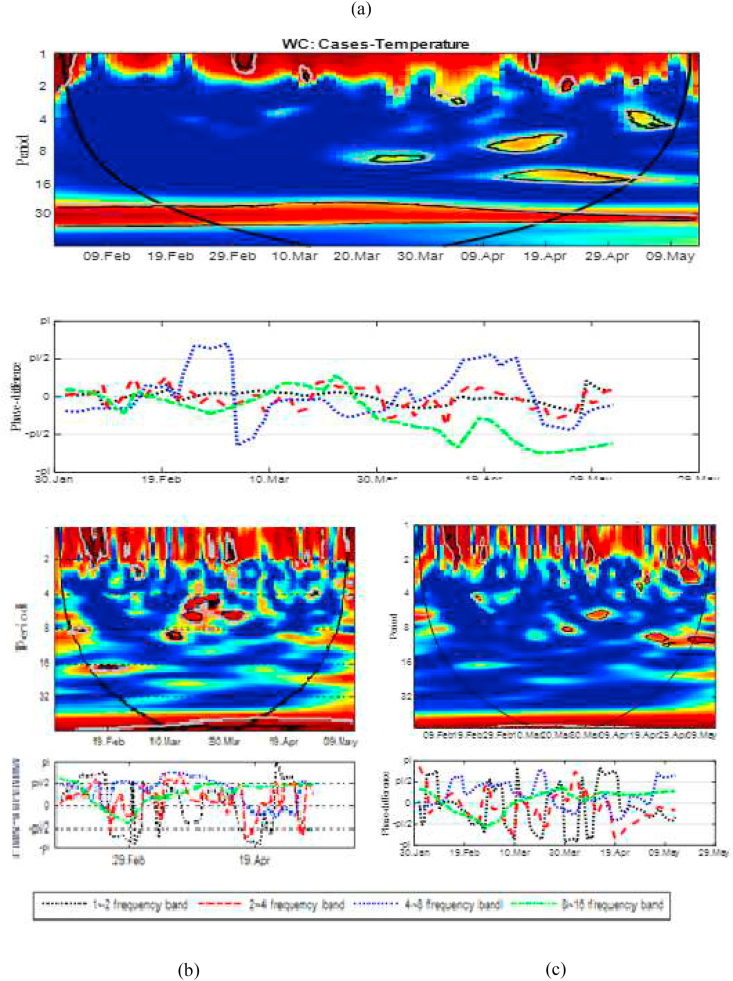

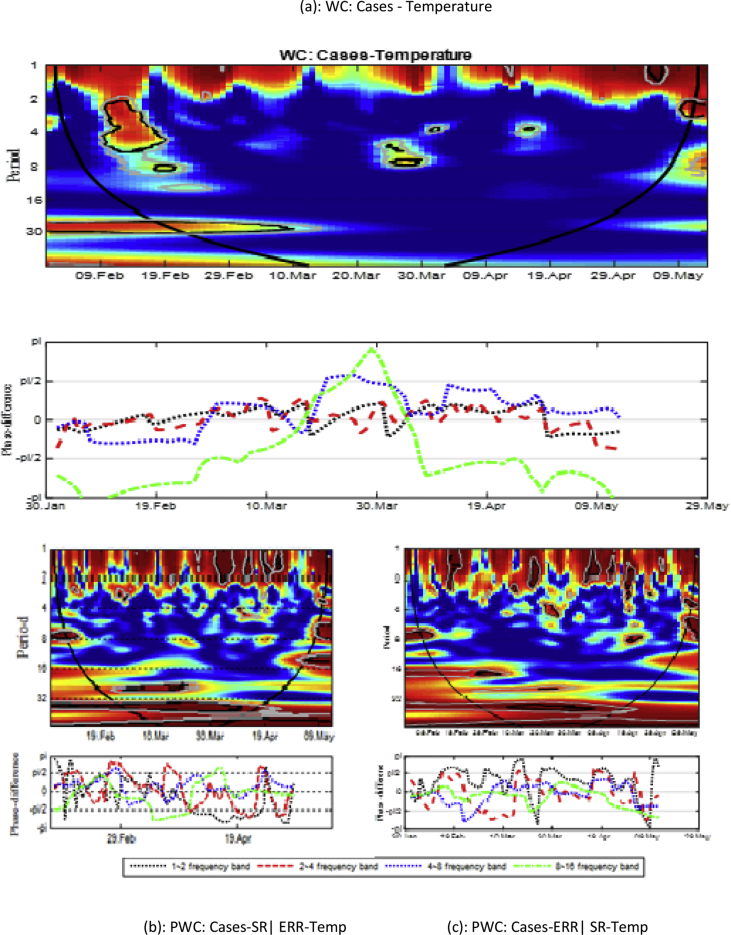

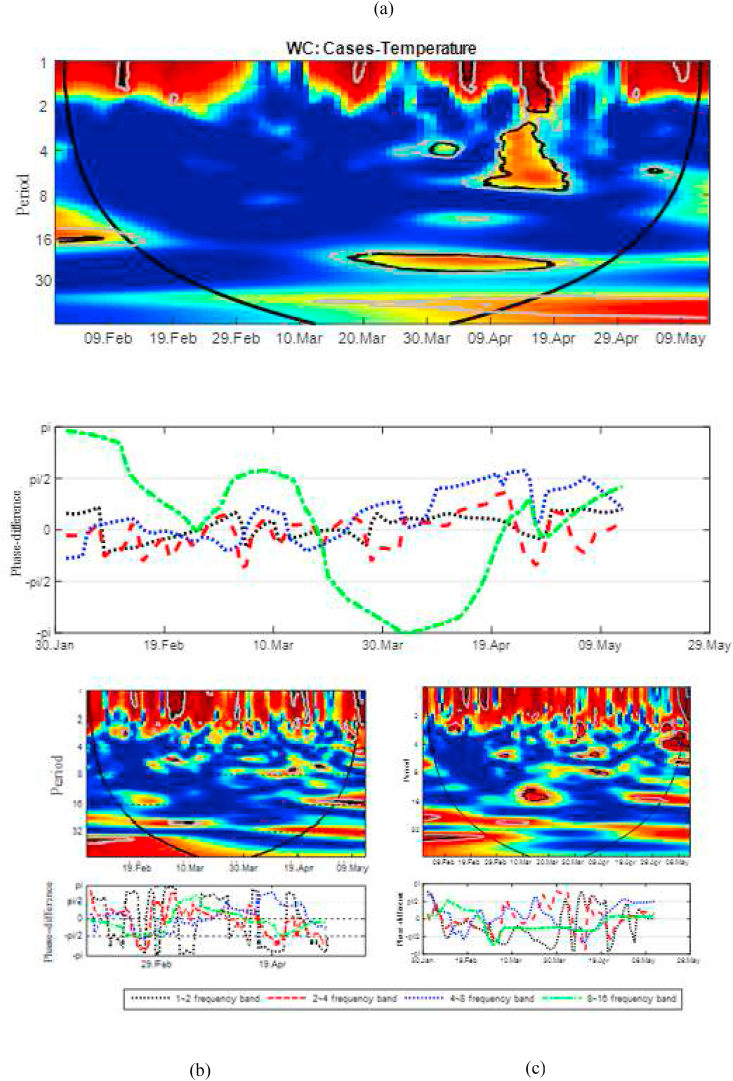

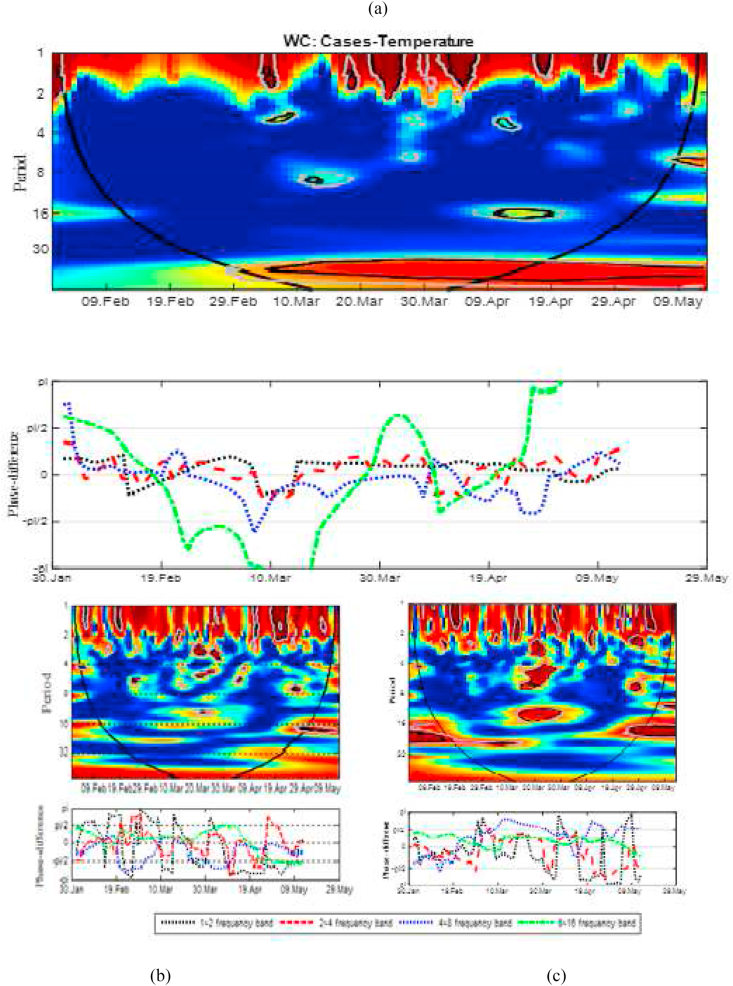

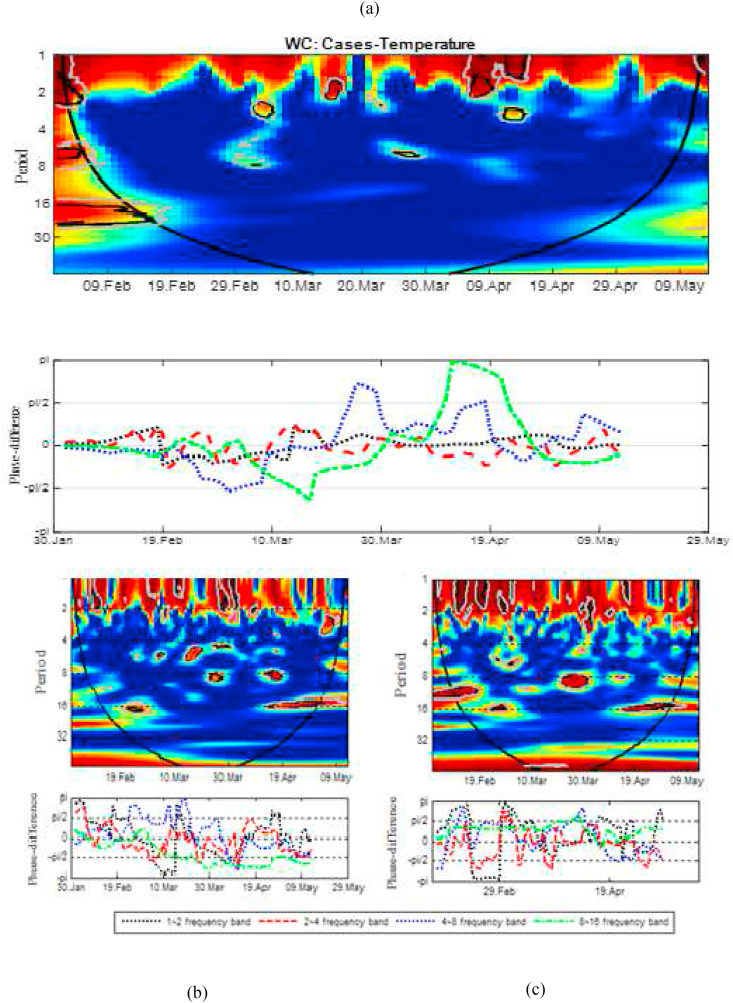

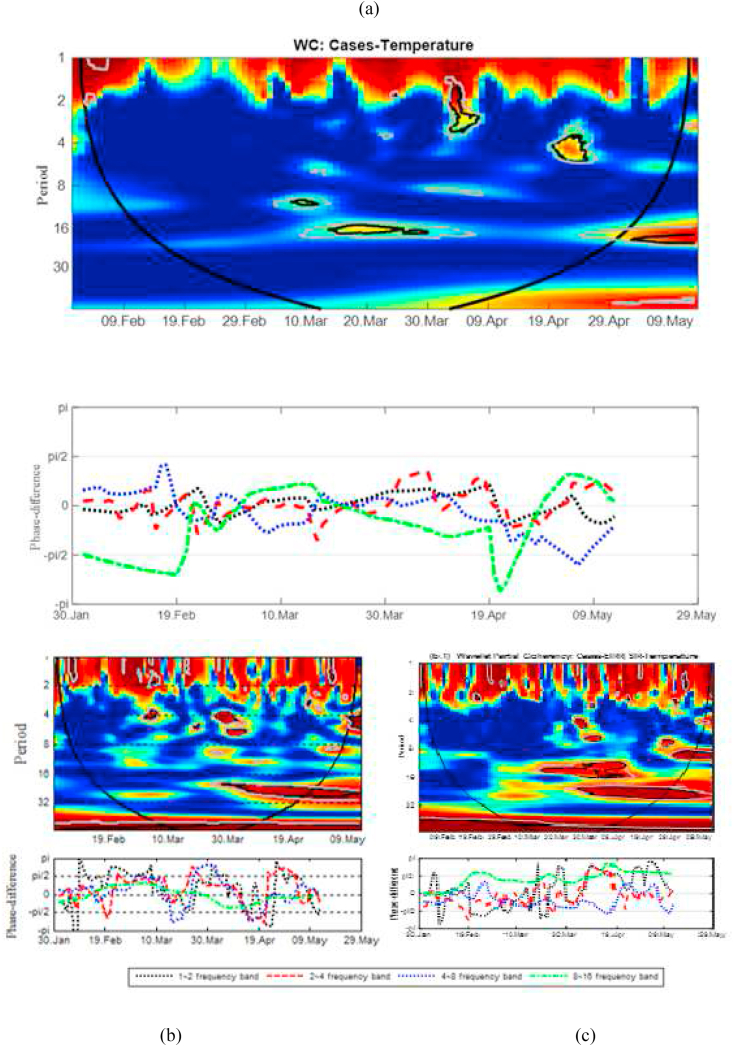

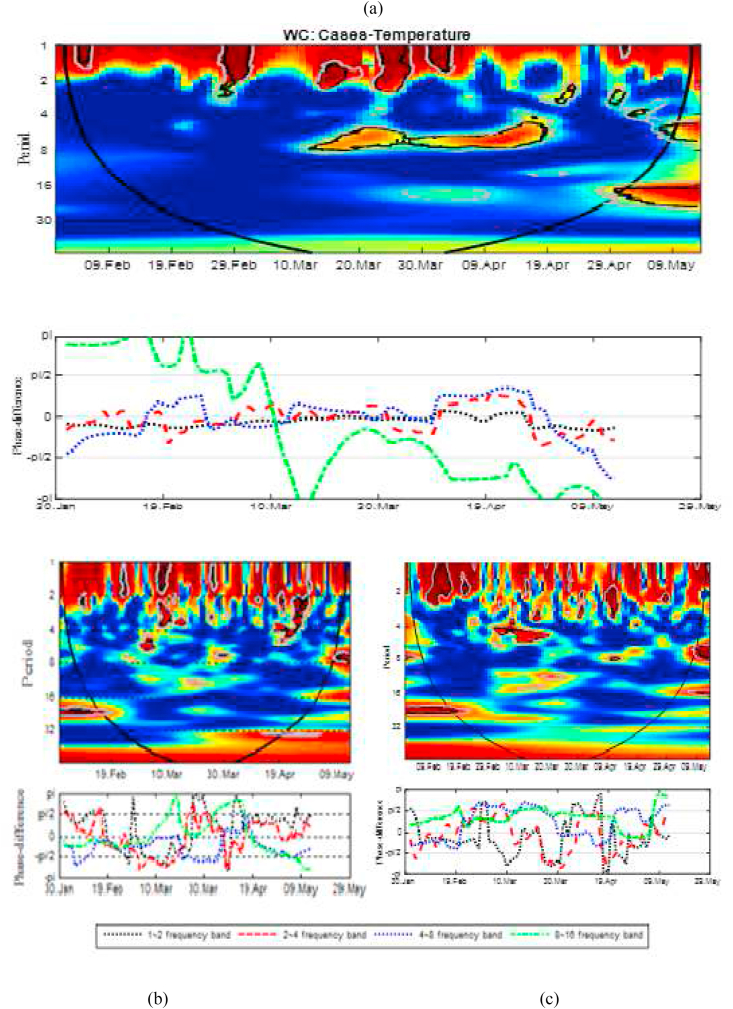

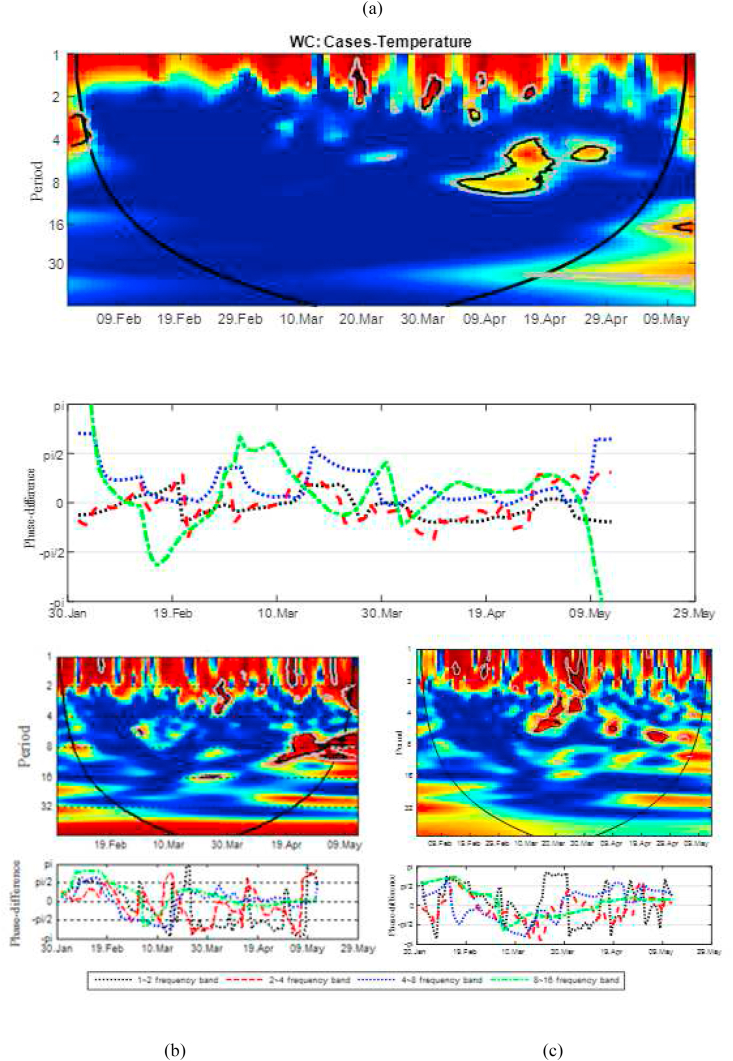

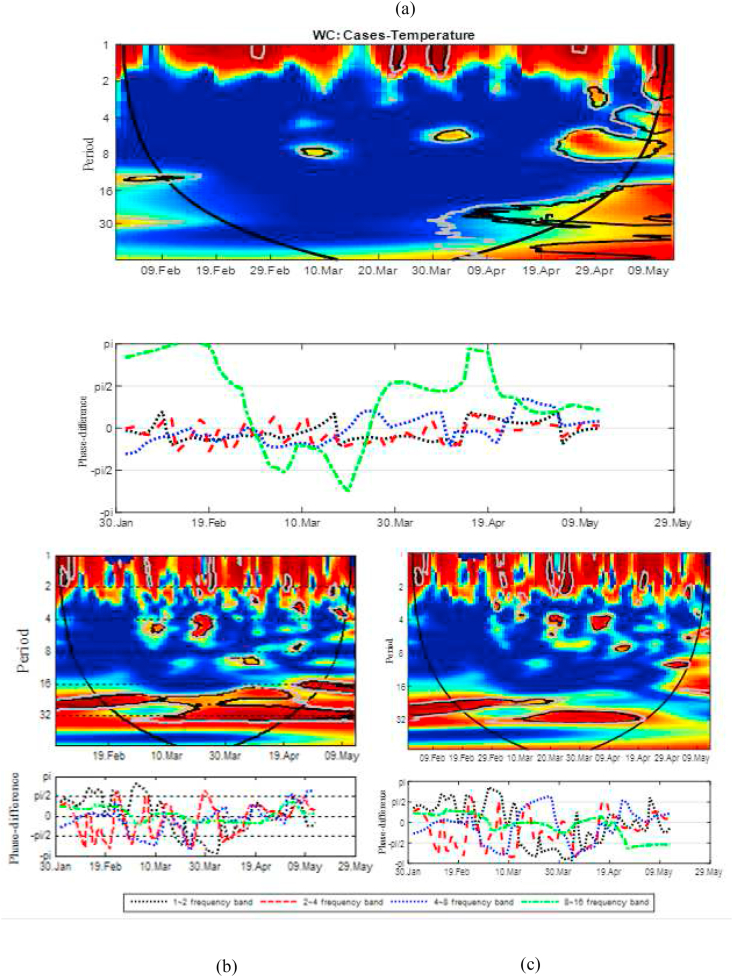

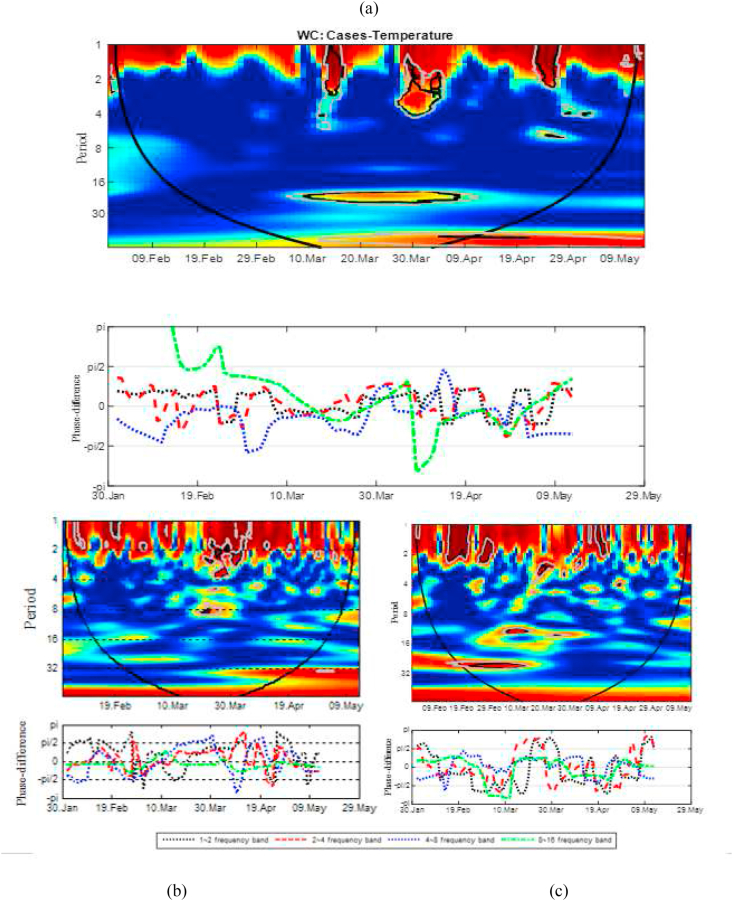

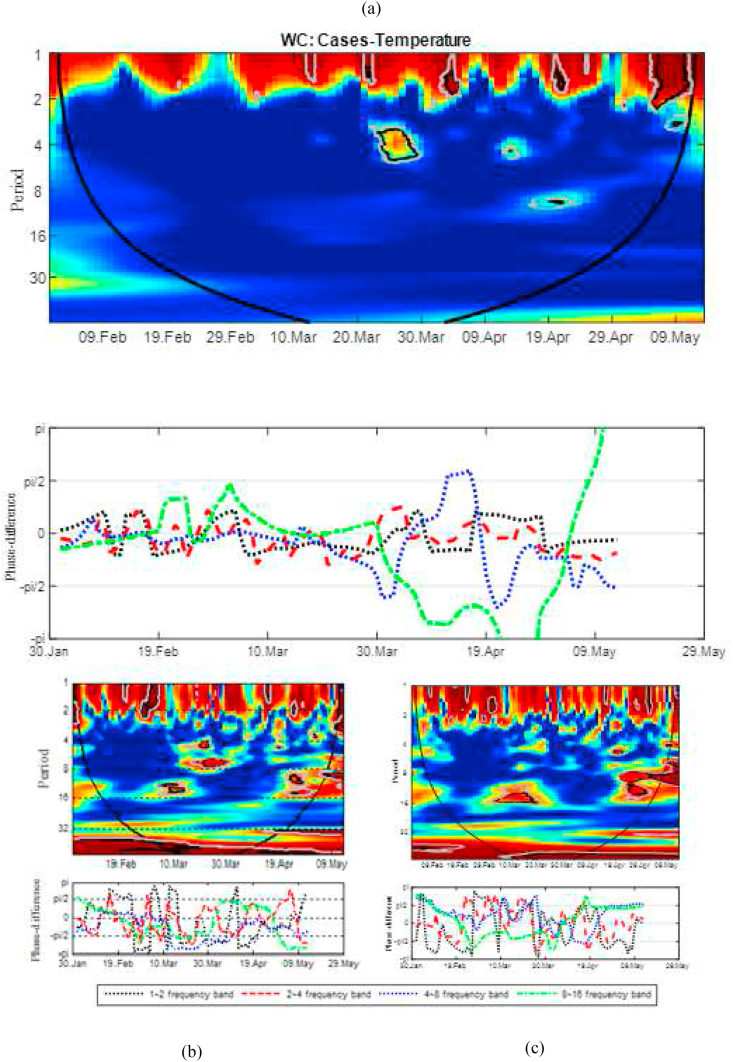

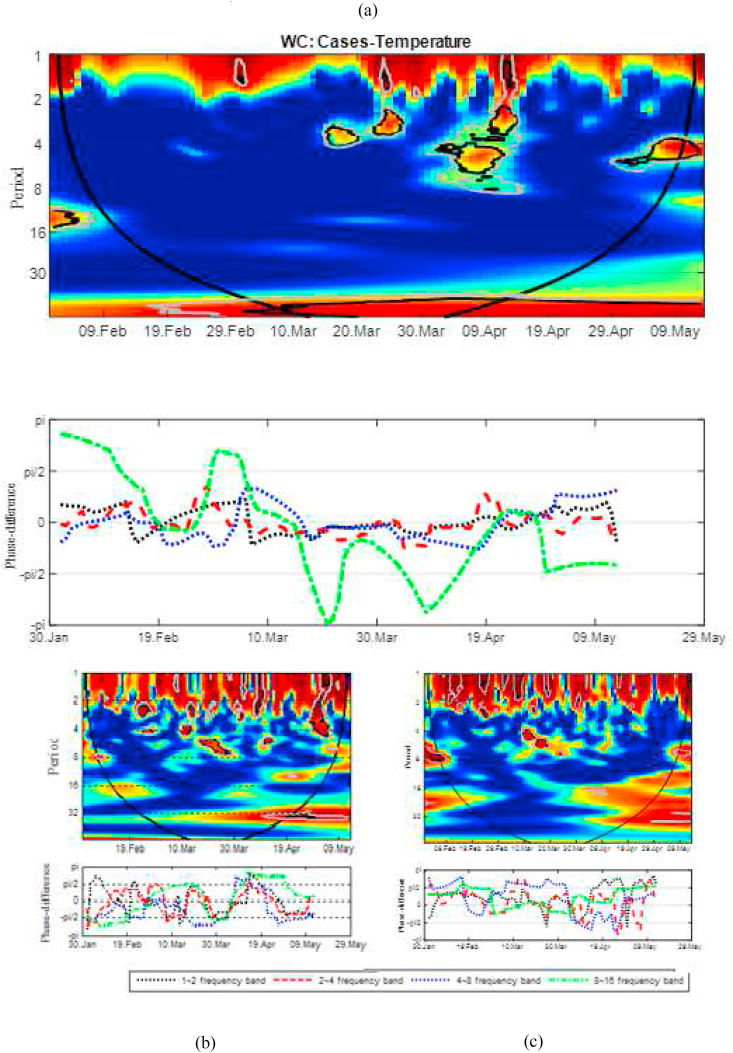

This paper examines the time-frequency relationship between the number of confirmed COVID-19 cases, temperature, exchange rates and stock market return in the top-15 most affected countries by the COVID-19 pandemic. We employ Wavelet Coherence and Partial Wavelet Coherence on the daily data from 1st February, 2020 to 13th May, 2020. This study adds to the literature by implementing the Wavelet Coherence technique to explore the unexpected outbreak effects of the global pandemic on temperature, exchange rates and stock market returns. Our results reveal (i) there is evidence of cyclicality between temperature and COVID-19 cases, implying that average daily temperature has a significant impact on the spread of the COVID-19 disease in most of the countries; (ii) strong connectedness at low frequencies display that COVID-19 cases have a significant long-term impact on the exchange rate returns and stock markets returns of the most affected countries under study; (iii) after controlling for the effect of stock market returns and temperature, the co-movements between the confirmed COVID-19 cases and exchange rate returns becomes stronger; (iv) after controlling for the effect of exchange rate returns and temperature, the co-movements between the confirmed COVID-19 cases and stock market returns become stronger. Apart from theoretical contribution, this paper offers value to investors and policymakers as they attempt to combat the coronavirus risk and shape the economy and stock market behavior.

本文研究了在受新冠疫情影响最严重的15个国家中,新冠确诊病例数、温度、汇率与股票市场回报之间的时频关系。我们对2020年2月1日至2020年5月13日的日数据运用了小波相干分析和偏小波相干分析。本研究通过运用小波相干技术来探究全球疫情对温度、汇率和股票市场回报的意外爆发影响,为该领域文献增添了内容。我们的研究结果表明:(i)温度与新冠病例之间存在周期性证据,这意味着在大多数国家,日均温度对新冠疾病的传播有重大影响;(ii)低频段的强关联性表明,新冠病例对所研究的受影响最严重国家的汇率回报和股票市场回报有重大长期影响;(iii)在控制了股票市场回报和温度的影响后,新冠确诊病例与汇率回报之间的共同变动变得更强;(iv)在控制了汇率回报和温度的影响后,新冠确诊病例与股票市场回报之间的共同变动变得更强。除了理论贡献外,本文还为投资者和政策制定者提供了价值,因为他们试图应对新冠病毒风险并塑造经济和股票市场行为。