Pham Binh Thai, Sala Hector

School of Public Finance, University of Economics Ho Chi Minh City, Ho Chi Minh City, Vietnam.

Departament D'Economia Aplicada, Universitat Autònoma de Barcelona, Barcelona, Spain.

Empir Econ. 2022;62(3):1123-1146. doi: 10.1007/s00181-021-02052-0. Epub 2021 Apr 20.

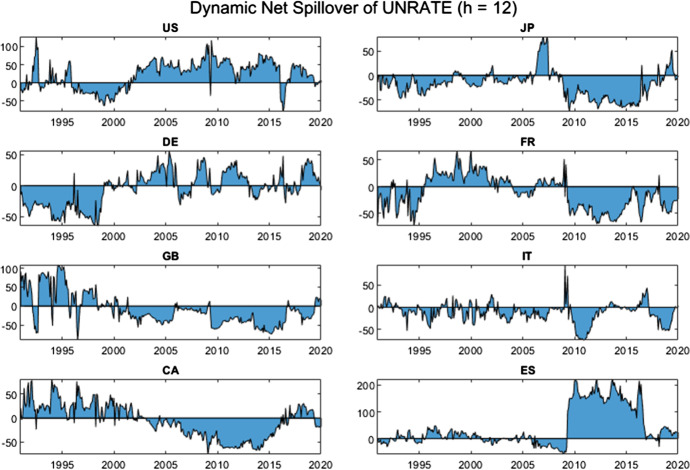

We bring the notion of connectedness (Diebold and Yilmaz, Int J Forecast 28(1):57-66 2012) to a set of two critical macroeconomic variables as inflation and unemployment. We focus on the G7 economies plus Spain, and use monthly data-high-frequency data in a macro setting-to explore the extent and consequences of total and directional volatility spillovers across variables and countries. We find that total connectedness is larger for prices (58.28%) than for unemployment (41.81%). We also identify asymmetries per country that result in higher short-run Phillips curve trade-offs in recessions and lower trade-offs in expansions. Besides, by exploring time-varying connectedness (resulting from country-specific shocks), we find that volatility spillovers magnify in periods of common economic turmoil such as the Global Financial Crisis. Our results call for an enhancement of international macroeconomic policy coordination.

The online version contains supplementary material available at 10.1007/s00181-021-02052-0.

我们将关联性概念(迪博尔德和伊尔马兹,《国际预测杂志》28(1):57 - 66,2012年)应用于通货膨胀和失业这两个关键宏观经济变量。我们聚焦于七国集团经济体加上西班牙,并使用月度数据——宏观背景下的高频数据——来探究变量间和国家间总体及定向波动溢出的程度和后果。我们发现,价格的总体关联性(58.28%)高于失业的总体关联性(41.81%)。我们还识别出各国存在的不对称性,这导致衰退期短期菲利普斯曲线权衡更高,而扩张期权衡更低。此外,通过探究时变关联性(由特定国家冲击导致),我们发现波动溢出在全球金融危机等共同经济动荡时期会放大。我们的结果呼吁加强国际宏观经济政策协调。

网络版包含可在10.1007/s00181 - 021 - 02052 - 0获取的补充材料。