Department of Nutrition, Gillings School of Global Public Health, University of North Carolina at Chapel Hill, Chapel Hill, North Carolina, United States of America.

Carolina Population Center, University of North Carolina at Chapel Hill, Chapel Hill, North Carolina, United States of America.

PLoS Med. 2021 May 25;18(5):e1003574. doi: 10.1371/journal.pmed.1003574. eCollection 2021 May.

In an effort to prevent and reduce the prevalence rate of people with obesity and diabetes, South Africa implemented a sugar-content-based tax called the Health Promotion Levy in April 2018, one of the first sugar-sweetened beverage (SSB) taxes to be based on each gram of sugar (beyond 4 g/100 ml). This before-and-after study estimated changes in taxed and untaxed beverage intake 1 year after the tax, examining separately, to our knowledge for the first time, the role of reformulation distinct from behavioral changes in SSB intake.

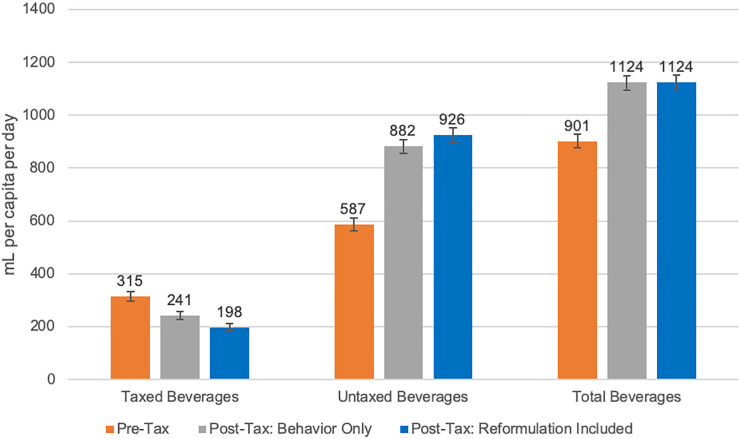

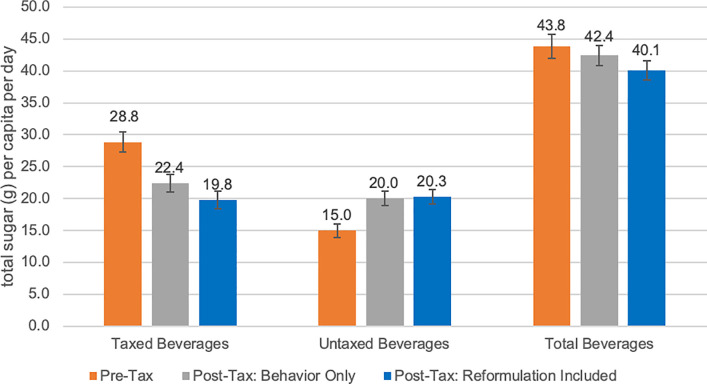

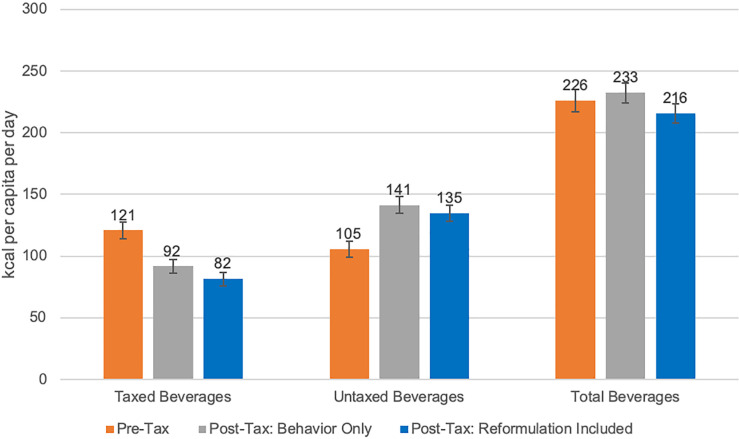

We collected single-day 24-hour dietary recalls from repeat cross-sectional surveys of adults aged 18-39 years in Langa, South Africa. Participants were recruited in February-March 2018 (pre-tax, n = 2,459) and February-March 2019 (post-tax, n = 2,489) using door-to-door sampling. We developed time-specific food composition tables (FCTs) for South African beverages before and after the tax, linked with the diet recalls. By linking pre-tax FCTs only to dietary intake data collected in the pre-tax and post-tax periods, we calculated changes in beverage intake due to behavioral change, assuming no reformulation. Next, we repeated the analysis using an updated FCT in the post-tax period to capture the marginal effect of reformulation. We estimated beverage intake using a 2-part model that takes into consideration the biases in using ordinary least squares or other continuous variable approaches with many individuals with zero intake. First, a probit model was used to estimate the probability of consuming the specific beverage category. Then, conditional on a positive outcome, a generalized linear model with a log-link was used to estimate the continuous amount of beverage consumed. Among taxed beverages, sugar intake decreased significantly (p < 0.0001) from 28.8 g/capita/day (95% CI 27.3-30.4) pre-tax to 19.8 (95% CI 18.5-21.1) post-tax. Energy intake decreased (p < 0.0001) from 121 kcal/capita/day (95% CI 114-127) pre-tax to 82 (95% CI 76-87) post-tax. Volume intake decreased (p < 0.0001) from 315 ml/capita/day (95% CI 297-332) pre-tax to 198 (95% CI 185-211) post-tax. Among untaxed beverages, sugar intake increased (p < 0.0001) by 5.3 g/capita/day (95% CI 3.7 to 6.9), and energy intake increased (p < 0.0001) by 29 kcal/capita/day (95% CI 19 to 39). Among total beverages, sugar intake decreased significantly (p = 0.004) by 3.7 (95% CI -6.2 to -1.2) g/capita/day. Behavioral change accounted for reductions of 24% in energy, 22% in sugar, and 23% in volume, while reformulation accounted for additional reductions of 8% in energy, 9% in sugar, and 14% in volume from taxed beverages. The key limitations of this study are an inability to make causal claims due to repeat cross-sectional data collection, and that the magnitude of reduction in taxed beverage intake may not be generalizable to higher income populations.

Using a large sample of a high-consuming, low-income population, we found large reductions in taxed beverage intake, separating the components of behavioral change from reformulation. This reduction was partially compensated by an increase in sugar and energy from untaxed beverages. Because policies such as taxes can incentivize reformulation, our use of an up-to-date FCT that reflects a rapidly changing food supply is novel and important for evaluating policy effects on intake.

为了预防和减少肥胖和糖尿病患者的流行率,南非于 2018 年 4 月实施了一项基于含糖量的税收,称为健康促进税,这是第一个基于每克糖(超过 4 克/100 毫升)的含糖饮料(SSB)税之一。这项前后对比研究估计了税收和非税收饮料摄入在税收实施后 1 年的变化,我们首次分别单独研究了配方改革与 SSB 摄入行为变化在其中的作用。

我们从南非兰加的成年人中收集了 18-39 岁的 24 小时饮食回忆的单一日期重复横断面调查。参与者于 2018 年 2 月至 3 月(税收前,n=2459)和 2019 年 2 月至 3 月(税收后,n=2489)通过挨家挨户的方式招募。我们为税收前后的南非饮料制定了特定的食物成分表(FCT),并与饮食回忆相关联。通过仅将税收前的 FCT 与税收前后时期收集的饮食摄入数据相关联,我们假设没有配方改革,计算了由于行为变化导致的饮料摄入量的变化。接下来,我们使用税收后更新的 FCT 重复分析,以捕捉配方改革的边际效应。我们使用两部分模型估计饮料摄入量,该模型考虑了使用普通最小二乘法或其他带有许多零摄入量个体的连续变量方法的偏差。首先,使用概率模型估计特定饮料类别的消费概率。然后,在出现阳性结果的情况下,使用对数链接的广义线性模型估计消耗的连续饮料量。在征税饮料中,糖摄入量显著下降(p<0.0001),从税收前的 28.8 克/人/天(95%CI 27.3-30.4)降至税收后的 19.8 克/人/天(95%CI 18.5-21.1)。能量摄入量减少(p<0.0001),从税收前的 121 千卡/人/天(95%CI 114-127)降至税收后的 82 千卡/人/天(95%CI 76-87)。体积摄入量减少(p<0.0001),从税收前的 315 毫升/人/天(95%CI 297-332)降至税收后的 198 毫升/人/天(95%CI 185-211)。在非征税饮料中,糖摄入量增加(p<0.0001)5.3 克/人/天(95%CI 3.7 至 6.9),能量摄入量增加(p<0.0001)29 千卡/人/天(95%CI 19 至 39)。在总饮料中,糖摄入量显著减少(p=0.004)3.7 克/人/天(95%CI-6.2 至-1.2)。行为变化导致能量减少 24%,糖减少 22%,体积减少 23%,而配方改革导致征税饮料的能量减少 8%,糖减少 9%,体积减少 14%。这项研究的主要限制是由于重复的横断面数据收集,因此无法做出因果关系的结论,并且税收饮料摄入量的减少幅度可能不适用于高收入人群。

我们使用大量高消费、低收入人群的样本发现,征税饮料的摄入量大幅减少,将行为变化和配方改革的成分分开。这种减少部分被非征税饮料中糖和能量的增加所补偿。由于税收等政策可以激励配方改革,因此我们使用最新的反映快速变化的食品供应的 FCT 是新颖且重要的,有助于评估政策对摄入的影响。