Krieger James, Magee Kiran, Hennings Tayler, Schoof John, Madsen Kristine A

University of Washington, Department of Health Services, USA.

Community Health Sciences, School of Public Health, University of California, Berkeley, USA.

Prev Med Rep. 2021 Apr 30;23:101388. doi: 10.1016/j.pmedr.2021.101388. eCollection 2021 Sep.

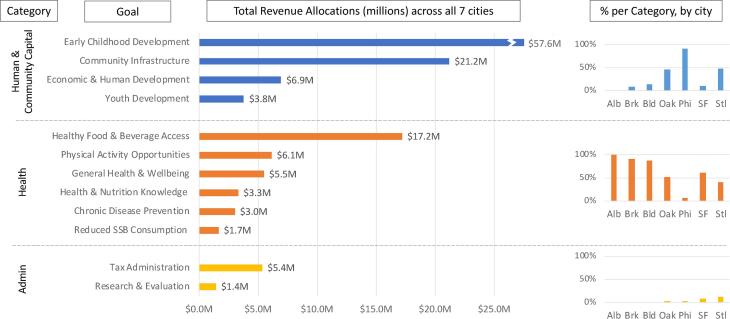

We sought to describe how revenues from sugar-sweetened beverage (SSB) excise taxes in 7 U.S. cities are being allocated, who is benefiting from these investments, and whether allocations are consistent with the original intent of tax legislation. We collected information from public documents and key informants about allocations in the most recent fiscal year available (ranging from 2018 to 2021). Across the 7 U.S. cities with taxes, the average annual revenue from SSB taxes totaled $133.9 M. In the fiscal year studied, cities allocated a total of $133.2 M in SSB tax revenues. Human and community capital investments totaled $89.6 M (67% of all allocations) funding early childhood development, community infrastructure improvements, and youth and workforce development. Health-related investments totaled $36.9 M (28% of total allocations), funding access to healthy foods and beverages; support for physical activity opportunities; promotion of overall physical, mental or social health and wellbeing; health and nutrition education; chronic-disease prevention and management; and reducing SSB consumption. In the 3 cities that specified how tax revenues would be spent, allocations were consistent with promised uses of revenues. In addition, 85% of aggregated revenues ($112.9 M) were targeted to support work and programs in impacted communities (communities that experience health inequities, discrimination and exclusion). SSB tax revenues are supporting initiatives to improve community health, develop human and community capital, and advance equity. These investments may yield additional health benefits beyond those resulting from lower SSB consumption. Consistent tracking and public reporting on revenue allocations would increase transparency and accountability.

我们试图描述美国7个城市的含糖饮料消费税收入是如何分配的,谁从这些投资中受益,以及分配是否符合税收立法的初衷。我们从公开文件和关键信息提供者那里收集了有关最近一个财政年度(2018年至2021年)分配情况的信息。在7个征收该税的美国城市中,含糖饮料税的年均收入总计1.339亿美元。在研究的财政年度,各城市共分配了1.332亿美元的含糖饮料税收入。人力和社区资本投资总计8960万美元(占所有分配资金的67%),用于资助幼儿发展、社区基础设施改善以及青年和劳动力发展。与健康相关的投资总计3690万美元(占总分配资金的28%),用于资助获取健康食品和饮料;支持体育活动机会;促进整体身体、心理或社会健康与福祉;健康和营养教育;慢性病预防与管理;以及减少含糖饮料消费。在3个明确规定了税收收入使用方式的城市中,分配符合承诺的收入用途。此外,85%的总收入(1.129亿美元)旨在支持受影响社区(经历健康不平等、歧视和排斥的社区)的工作和项目。含糖饮料税收入正在支持改善社区健康、发展人力和社区资本以及促进公平的举措。这些投资可能会产生除降低含糖饮料消费所带来的健康益处之外的其他健康效益。对收入分配进行持续跟踪和公开报告将提高透明度和问责制。