Finance, Economics, and Management Research Group, Ho Chi Minh City Open University, Ho Chi Minh City, Vietnam.

FPT University, Hanoi, Vietnam.

Comput Intell Neurosci. 2021 Dec 8;2021:2917577. doi: 10.1155/2021/2917577. eCollection 2021.

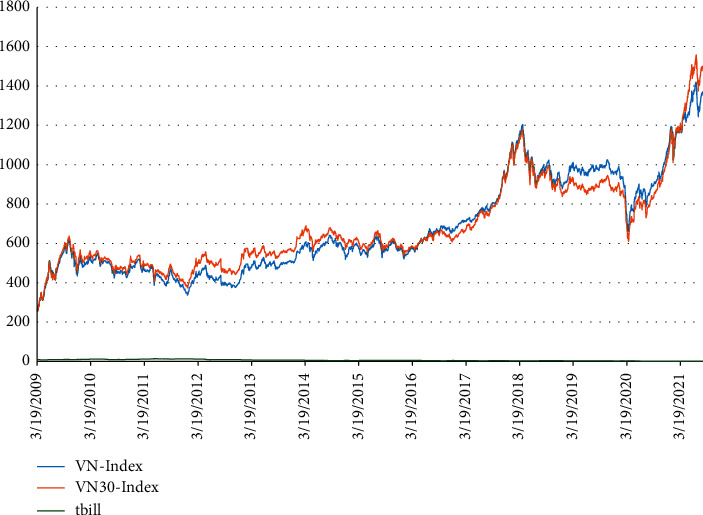

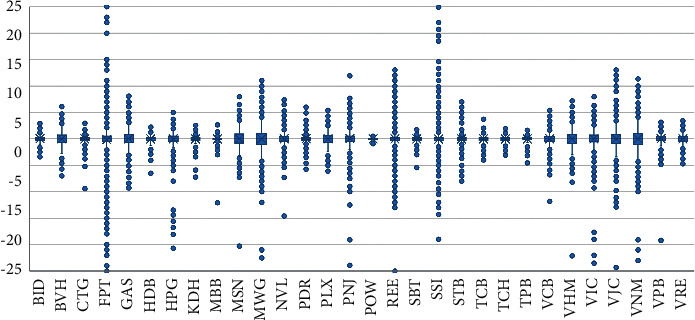

Risk management and stock investment decision-making is an essential topic for investors and fund managers, especially in the context of the COVID-19 pandemic. The problem becomes easier if the market is efficient, where stock prices fully reflect potential risk. Nevertheless, if the market is not efficient, investors may have an opportunity to find an effective investment method. Vietnam is one of the emerging markets; the efficiency is still weak. Thus, there will be an opportunity for astute investors. This study aims to test the weak-form efficient market and provide a modern approach to investors' decision-making. To achieve that aim, this study uses historical data of stocks in the VN-Index and VN30 portfolio to buy and sell within a one-day period under the rolling window approach to test the Ho Chi Minh City Stock Exchange (HoSE) through a runs test and to perform stock trading using the support vector machine (SVM) and logistic regression. The buying/selling of stocks is guided by the forecasted outcomes (increase/decrease) of logistic regression and SVM. This study adjusted the return rate in proportion to the risks and compared it with index investments of VN-Index and VN30 to evaluate investment efficiency. The test results dismissed the weak-form efficient-market hypothesis, which opens up many opportunities for short-term traders. This study's primary contribution is to provide a stock trading strategy for short-term investors to maximize trading profits. Because logistic regression and SVM have proven effective trading methods, investors can use them to achieve abnormal returns.

风险管理和股票投资决策是投资者和基金经理的重要课题,尤其是在 COVID-19 大流行背景下。如果市场是有效的,即股票价格充分反映了潜在风险,那么问题就会变得简单。然而,如果市场是无效的,投资者可能有机会找到有效的投资方法。越南是新兴市场之一,效率仍然较弱。因此,对于精明的投资者来说,将会有机会。本研究旨在检验弱形式有效市场,并为投资者的决策提供现代方法。为了实现这一目标,本研究使用 VN-Index 和 VN30 投资组合中股票的历史数据,采用滚动窗口方法在一天内买卖股票,通过游程检验对胡志明市证券交易所(HoSE)进行检验,并使用支持向量机(SVM)和逻辑回归进行股票交易。股票的买卖是由逻辑回归和 SVM 的预测结果(增加/减少)指导的。本研究根据风险按比例调整回报率,并与 VN-Index 和 VN30 的指数投资进行比较,以评估投资效率。测试结果否定了弱形式有效市场假说,为短期交易者提供了许多机会。本研究的主要贡献是为短期投资者提供股票交易策略,以最大化交易利润。由于逻辑回归和 SVM 已被证明是有效的交易方法,投资者可以使用它们来获得异常回报。