Clemente Gian Paolo, Grassi Rosanna, Hitaj Asmerilda

Dipartimento di Discipline Matematiche, Finanza Matematica ed Econometria, Università Cattolica del Sacro Cuore, Milan, Italy.

Dipartimento di Statistica e Metodi Quantitativi, Università degli Studi di Milano-Bicocca, Milan, Italy.

Ann Oper Res. 2022;316(2):1519-1541. doi: 10.1007/s10479-022-04675-7. Epub 2022 Apr 11.

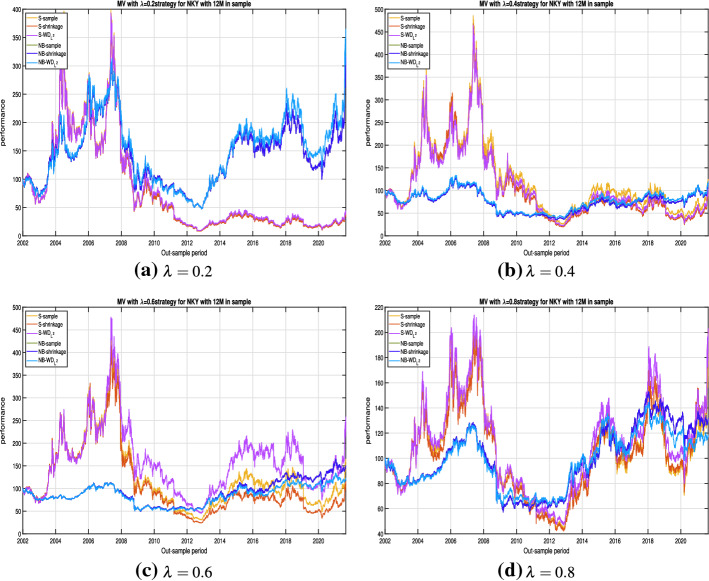

In this article we deal with the problem of portfolio allocation by enhancing network theory tools. We propose the use of the correlation network dependence structure in constructing some well-known risk-based models in which the estimation of the correlation matrix is a building block in the portfolio optimization. We formulate and solve all these portfolio allocation problems using both the standard approach and the network-based approach. Moreover, in constructing the network-based portfolios we propose the use of three different estimators for the covariance matrix: the sample, the shrinkage toward constant correlation and the depth-based estimators . All the strategies under analysis are implemented on three high-dimensional portfolios having different characteristics. We find that the network-based portfolio consistently performs better and has lower risk compared to the corresponding standard portfolio in an out-of-sample perspective.

The online version contains supplementary material available at 10.1007/s10479-022-04675-7.

在本文中,我们通过增强网络理论工具来处理投资组合分配问题。我们建议在构建一些著名的基于风险的模型时使用相关网络依赖结构,其中相关矩阵的估计是投资组合优化的一个组成部分。我们使用标准方法和基于网络的方法来制定和解决所有这些投资组合分配问题。此外,在构建基于网络的投资组合时,我们建议使用三种不同的协方差矩阵估计器:样本估计器、向常数相关收缩的估计器和基于深度的估计器。所有分析的策略都在具有不同特征的三个高维投资组合上实施。我们发现,从样本外的角度来看,基于网络的投资组合始终表现更好,风险更低。

在线版本包含可在10.1007/s10479-022-04675-7获取的补充材料。