Duan Yuejiao, Liu Lanbiao, Wang Zhuo

School of Finance, Nankai University, Tianjin, 300350, China.

Res Int Bus Finance. 2021 Dec;58:101432. doi: 10.1016/j.ribaf.2021.101432. Epub 2021 Jun 2.

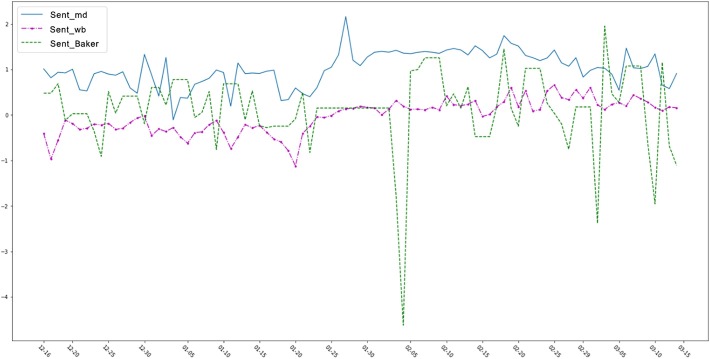

This study quantitatively measures the Chinese stock market's reaction to sentiments regarding the Novel Coronavirus 2019 (COVID-19). Using 6.3 million items of textual data extracted from the official news media and blogsite, we develop two COVID-19 sentiment indices that capture the moods related to COVID-19. Our sentiment indices are real-time and forward-looking indices in the stock market. We discover that stock returns and turnover rates were positively predicted by the COVID-19 sentiments during the period from December 17, 2019 to March 13, 2020. Consistent with this prediction, margin trading and short selling activities intensified proactively with growth sentiment. Overall, these results illustrate how the effects of the pandemic crisis were amplified by the sentiments.

本研究定量测度了中国股票市场对2019年新型冠状病毒(COVID-19)相关情绪的反应。利用从官方新闻媒体和博客网站提取的630万条文本数据,我们构建了两个捕捉与COVID-19相关情绪的COVID-19情绪指数。我们的情绪指数是股票市场的实时前瞻性指数。我们发现,在2019年12月17日至2020年3月13日期间,COVID-19情绪对股票回报率和换手率有正向预测作用。与这一预测一致,融资融券交易活动随着情绪的增长而积极加剧。总体而言,这些结果说明了大流行危机的影响是如何被情绪放大的。