Zada Hassan, Maqsood Huma, Ahmed Shakeel, Khan Muhammad Zeb

Department of Management Sciences, SZABIST, Islamabad, Pakistan.

Department of Social Sciences, SZABIST, Islamabad, Pakistan.

SN Bus Econ. 2023;3(1):37. doi: 10.1007/s43546-022-00417-w. Epub 2023 Jan 9.

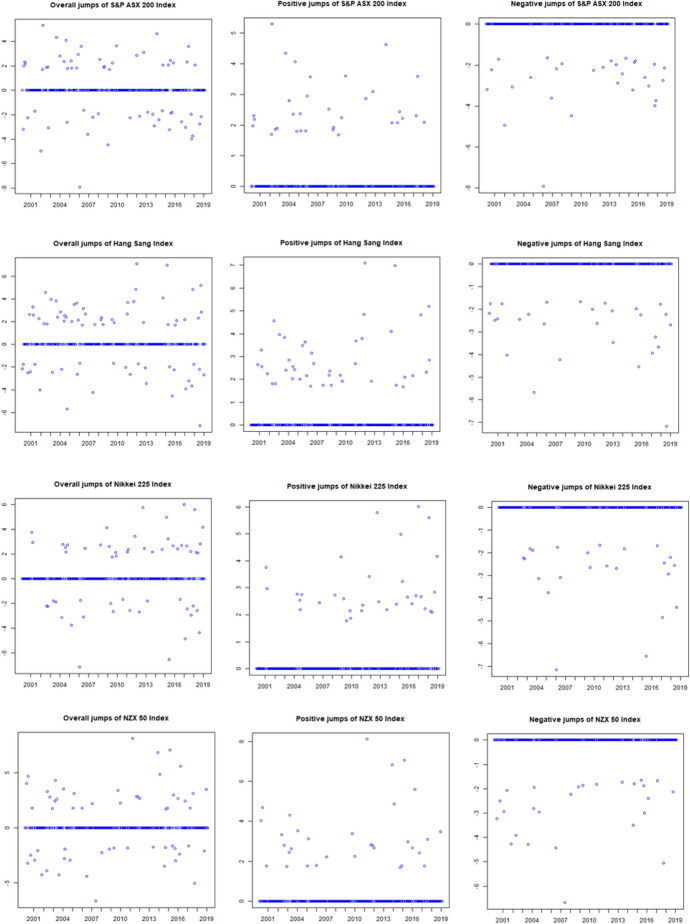

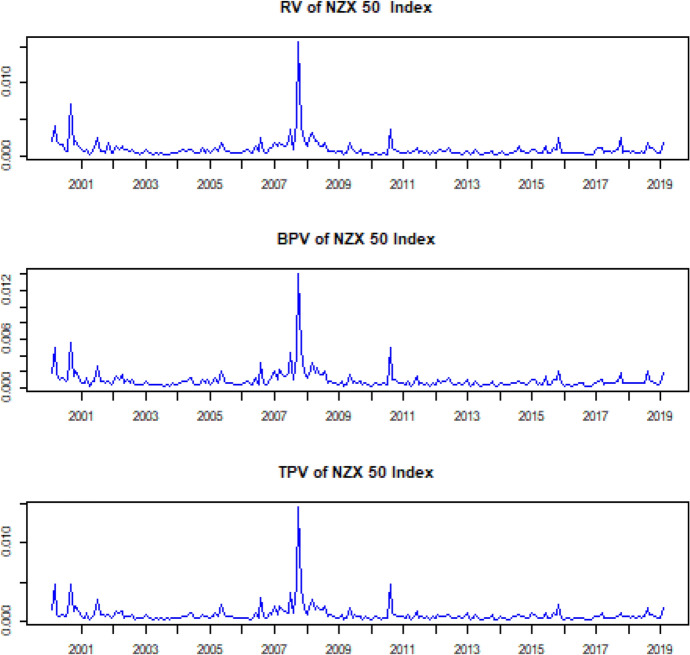

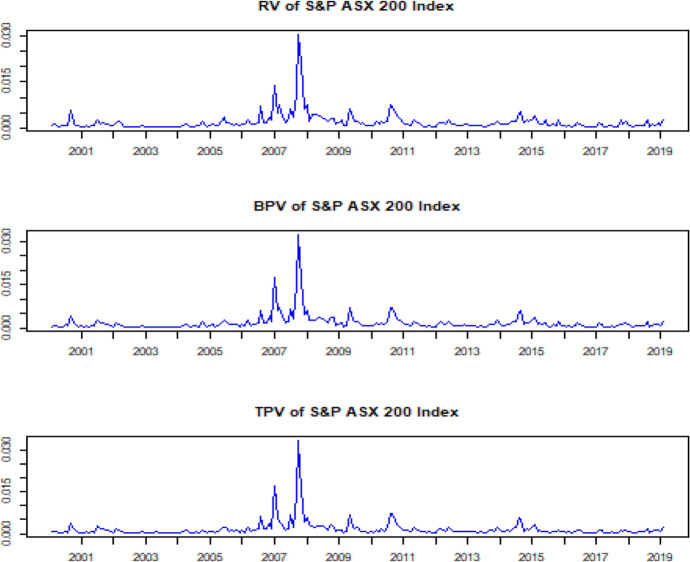

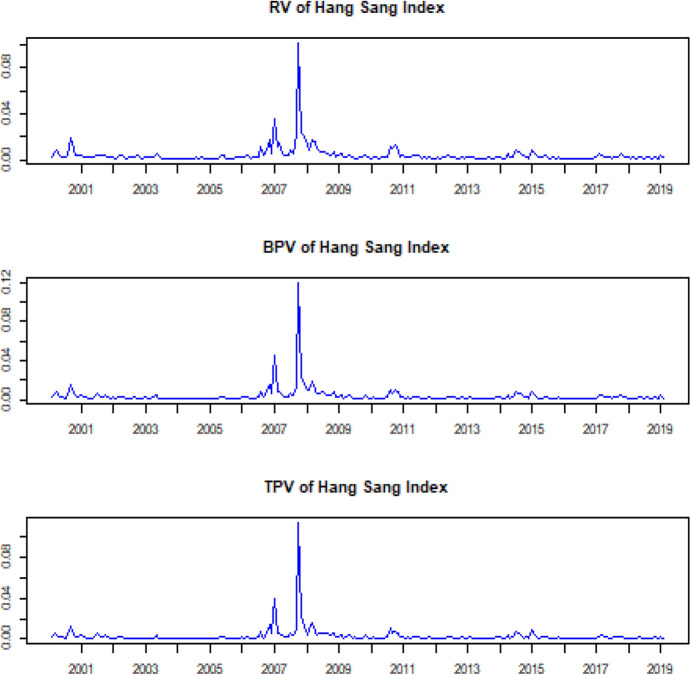

This research explores the function of information shocks in equity returns and integrated volatility of emerging Asian markets using Swap Variance (SwV) approach on the period of 20 years (Feb 2001-Feb 2020). It compares average monthly returns and volatility of shock periods with non-shock periods after separating negative and positive shocks. Findings reveal frequent occurrence of information shocks in all Asian developed equity markets with positive shocks than that of negative shocks. Moreover, highly volatile Asian developed markets earn higher returns during shocks periods, while markets with higher volatility and lower continuous returns are adversely affected during shocks periods. The ratio of total realized volatility and the average ratio of shocks volatility establish that shocks account for a considerable amount of volatility, and integrated volatility is higher during negative shocks phases. The study has implications for all stakeholders of financial markets for rational investment decisions.

本研究采用互换方差(SwV)方法,对20年期间(2001年2月至2020年2月)新兴亚洲市场的股票回报和综合波动率中的信息冲击功能进行了探索。在区分正负冲击后,将冲击期与非冲击期的平均月回报率和波动率进行了比较。研究结果显示,在所有亚洲发达股票市场中,信息冲击频繁发生,且正冲击比负冲击更为常见。此外,高波动率的亚洲发达市场在冲击期获得更高的回报,而波动率较高且连续回报率较低的市场在冲击期受到不利影响。总实现波动率与冲击波动率平均比率表明,冲击占相当大比例的波动率,且在负冲击阶段综合波动率更高。该研究对金融市场的所有利益相关者做出理性投资决策具有启示意义。