Zenger Brian, Li Haojia, Bunch T Jared, Crawford Candice, Fang James C, Groh Christopher A, Hess Rachel, Navaravong Leenhapong, Ranjan Ravi, Young Jeff, Zhang Yue, Steinberg Benjamin A

University of Utah School of Medicine, Salt Lake City, Utah.

Department of Internal Medicine, Division of Epidemiology, University of Utah, Salt Lake City, Utah.

Heart Rhythm O2. 2022 Dec 27;4(4):251-257. doi: 10.1016/j.hroo.2022.12.014. eCollection 2023 Apr.

Catheter ablation is an effective treatment for atrial fibrillation (AF) but incurs significant financial costs to payers. Reducing variability may improve cost effectiveness.

We aimed to measure (1) the components of direct and indirect costs for routine AF ablation procedures, (2) the variability of those costs, and (3) the main factors driving ablation cost variability.

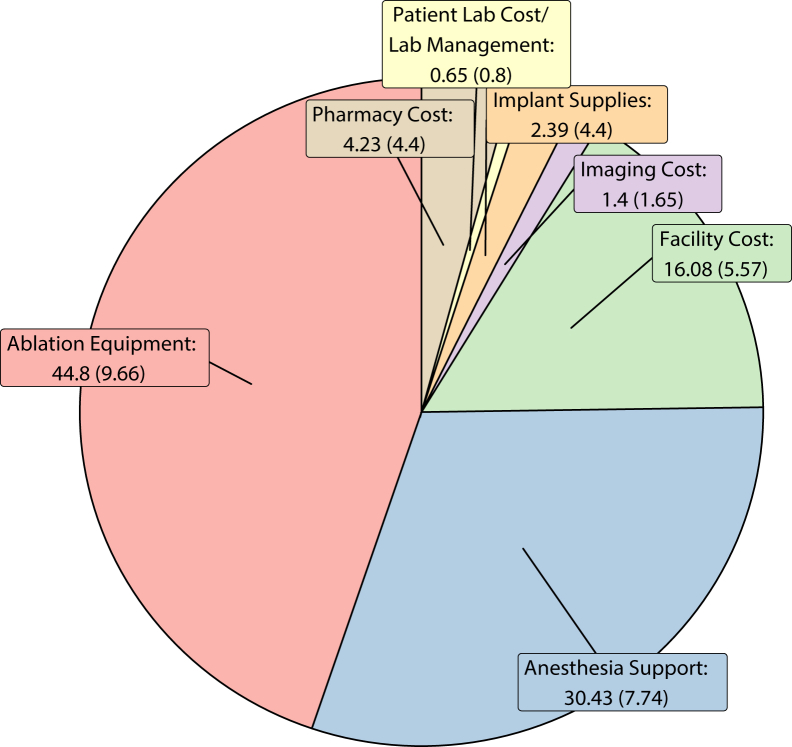

Using data from the University of Utah Health Value Driven Outcomes system, we were able to measure direct, inflation-adjusted costs of uncomplicated, routine AF ablation to the healthcare system. Direct costs were considered costs incurred by pharmacy, disposable supplies, patient labs, implants, and other services categories (primarily anesthesia support) and indirect costs were considered within imaging, facility, and electrophysiology lab management categories.

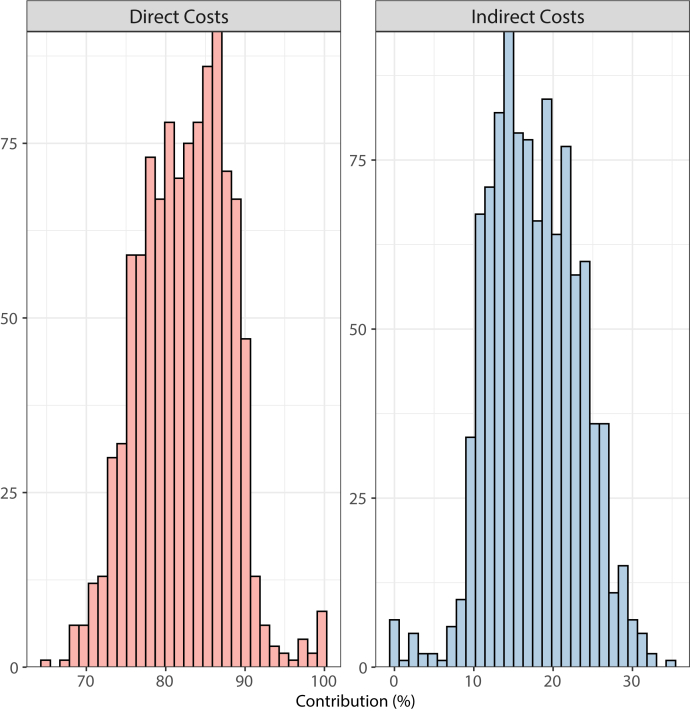

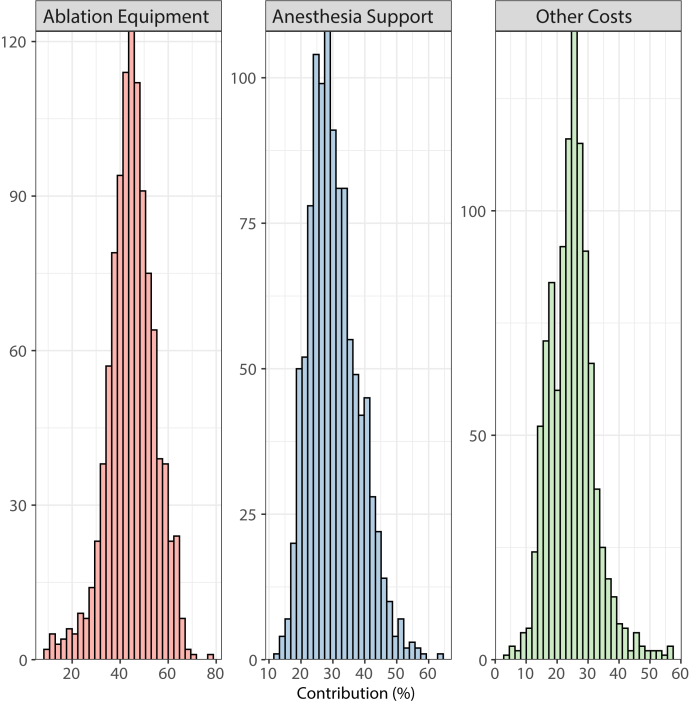

A total of 910 patients with 1060 outpatient ablation encounters were included from January 1, 2013, to December 31, 2020. Disposable supplies accounted for the largest component of cost with 44.8 ± 9.7%, followed by other services (primarily anesthesia support) with 30.4 ± 7.7% and facility costs with 16.1 ± 5.6%; pharmacy, imaging, and implant costs each contributed <5%. Direct costs were larger than indirect costs (82.4 ± 5.6% vs 17.6 ± 5.6%). Multivariable regression showed that procedure operator was the primary factor associated with AF ablation overall cost (up to 12% differences depending on operator).

Direct costs and other services (primarily anesthesia) drive the majority costs associated with AF ablations. There is significant variability in costs for these routine, uncomplicated AF ablation procedures. The procedure operator, and not patient characteristic, is the main driver for cost variability.

导管消融术是治疗心房颤动(AF)的有效方法,但会给支付方带来巨大的经济成本。降低成本差异可能会提高成本效益。

我们旨在衡量(1)常规房颤消融手术的直接和间接成本组成部分,(2)这些成本的差异,以及(3)导致消融成本差异的主要因素。

利用犹他大学健康价值驱动结果系统的数据,我们能够衡量简单常规房颤消融手术对医疗系统的直接、经通胀调整的成本。直接成本被认为是药房、一次性用品、患者实验室、植入物和其他服务类别(主要是麻醉支持)产生的成本,间接成本则在影像、设施和电生理实验室管理类别中考虑。

从2013年1月1日至2020年12月31日,共纳入910例患者的1060次门诊消融病例。一次性用品占成本的最大组成部分,为44.8±9.7%,其次是其他服务(主要是麻醉支持),占30.4±7.7%,设施成本占16.1±5.6%;药房、影像和植入物成本各自占比均小于5%。直接成本大于间接成本(82.4±5.6%对17.6±5.6%)。多变量回归显示,手术操作者是与房颤消融总成本相关联的主要因素(根据操作者不同,差异高达12%)。

直接成本和其他服务(主要是麻醉)构成了与房颤消融相关的大部分成本。这些常规、简单的房颤消融手术成本存在显著差异。手术操作者而非患者特征是成本差异的主要驱动因素。