Health Economics Research Unit, KEMRI Wellcome Trust Research Programme, P.O.BOX 43640-00100, Nairobi, Kenya.

AMPATH, Eldoret, Kenya.

Int J Equity Health. 2023 Jun 1;22(1):107. doi: 10.1186/s12939-023-01923-5.

Non-communicable diseases (NCDs) can impose a substantial financial burden to households in the absence of an effective financial risk protection mechanism. The national health insurance fund (NHIF) has included NCD services in its national scheme. We evaluated the effectiveness of NHIF in providing financial risk protection to households with persons living with hypertension and/or diabetes in Kenya.

We carried out a prospective cohort study, following 888 households with at least one individual living with hypertension and/or diabetes for 12 months. The exposure arm comprised households that are enrolled in the NHIF national scheme, while the control arm comprised households that were not enrolled in the NHIF. Study participants were drawn from two counties in Kenya. We used the incidence of catastrophic health expenditure (CHE) as the outcome of interest. We used coarsened exact matching and a conditional logistic regression model to analyse the odds of CHE among households enrolled in the NHIF compared with unenrolled households. Socioeconomic inequality in CHE was examined using concentration curves and indices.

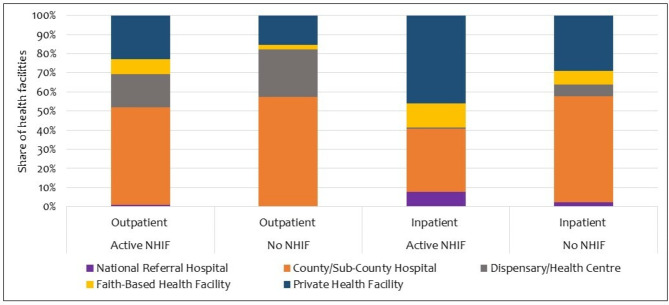

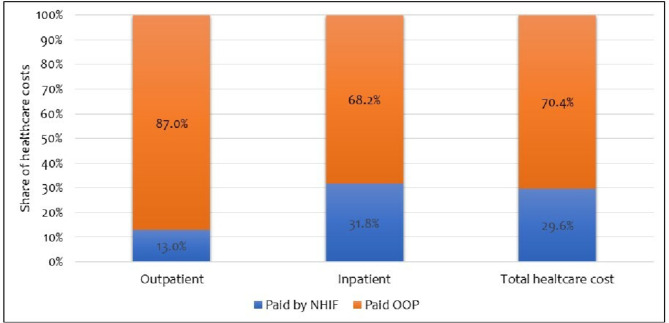

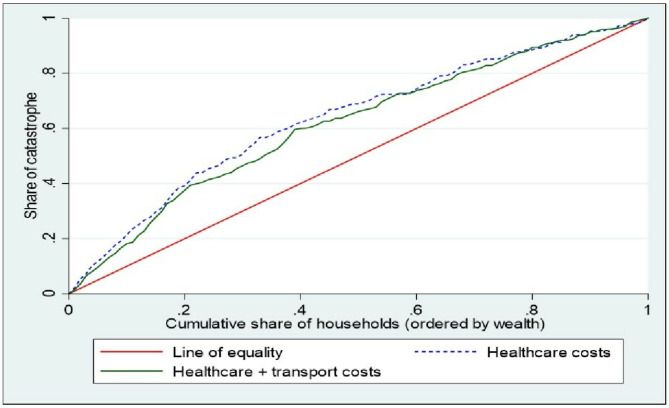

We found strong evidence that NHIF-enrolled households spent a lower share (12.4%) of their household budget on healthcare compared with unenrolled households (23.2%) (p = 0.004). While households that were enrolled in NHIF were less likely to incur CHE, we did not find strong evidence that they are better protected from CHE compared with households without NHIF (OR = 0.67; p = 0.47). The concentration index (CI) for CHE showed a pro-poor distribution (CI: -0.190, p < 0.001). Almost half (46.9%) of households reported active NHIF enrolment at baseline but this reduced to 10.9% after one year, indicating an NHIF attrition rate of 76.7%. The depth of NHIF cover (i.e., the share of out-of-pocket healthcare costs paid by NHIF) among households with active NHIF was 29.6%.

We did not find strong evidence that the NHIF national scheme is effective in providing financial risk protection to households with individuals living with hypertension and/diabetes in Kenya. This could partly be explained by the low depth of cover of the NHIF national scheme, and the high attrition rate. To enhance NHIF effectiveness, there is a need to revise the NHIF benefit package to include essential hypertension and/diabetes services, review existing provider payment mechanisms to explicitly reimburse these services, and extend the existing insurance subsidy programme to include individuals in the informal labour market.

在缺乏有效的财务风险保护机制的情况下,非传染性疾病(NCD)会给家庭带来沉重的经济负担。国家健康保险基金(NHIF)已将 NCD 服务纳入国家计划。我们评估了 NHIF 为肯尼亚患有高血压和/或糖尿病的人提供家庭财务风险保护的效果。

我们进行了一项前瞻性队列研究,对 888 户至少有一名患有高血压和/或糖尿病的个人进行了 12 个月的随访。暴露组包括参加 NHIF 国家计划的家庭,而对照组包括未参加 NHIF 的家庭。研究参与者来自肯尼亚的两个县。我们以灾难性医疗支出(CHE)的发生率为研究结果。我们使用粗化精确匹配和条件逻辑回归模型来分析与未参保家庭相比,参保 NHIF 的家庭发生 CHE 的可能性。我们使用集中曲线和指数来检查 CHE 的社会经济不平等。

我们有充分的证据表明,与未参保家庭(23.2%)相比,参保 NHIF 的家庭在医疗保健方面的支出占家庭预算的比例较低(12.4%)(p=0.004)。虽然参加 NHIF 的家庭发生 CHE 的可能性较小,但我们没有发现强有力的证据表明他们比没有 NHIF 的家庭受到更好的 CHE 保护(OR=0.67;p=0.47)。CHE 的集中指数(CI)显示出有利于穷人的分布(CI:-0.190,p<0.001)。几乎一半(46.9%)的家庭在基线时报告了积极的 NHIF 参保,但一年后这一比例降至 10.9%,表明 NHIF 的退保率为 76.7%。参保 NHIF 的家庭中 NHIF 覆盖的深度(即 NHIF 支付的自付医疗费用份额)为 29.6%。

我们没有发现强有力的证据表明 NHIF 国家计划能够有效地为肯尼亚患有高血压和/或糖尿病的家庭提供财务风险保护。这可能部分归因于 NHIF 国家计划的覆盖深度较低,以及较高的退保率。为了提高 NHIF 的效果,需要修订 NHIF 的福利套餐,将基本高血压和/或糖尿病服务纳入其中,审查现有的提供者支付机制,以明确报销这些服务,并将现有的保险补贴计划扩大到非正规劳动力市场的个人。