Ozaki Jun'ichi, Viegas Eduardo, Takayasu Hideki, Takayasu Misako

Department of Computer Science, School of Computing, Tokyo Institute of Technology, 4259, Nagatsuta-cho, Midori-ku, Yokohama, 226-8503, Japan.

Centre for Complexity Science and Department of Mathematics, Imperial College, London, SW7 2AZ, UK.

Sci Rep. 2024 Feb 26;14(1):4628. doi: 10.1038/s41598-024-54719-0.

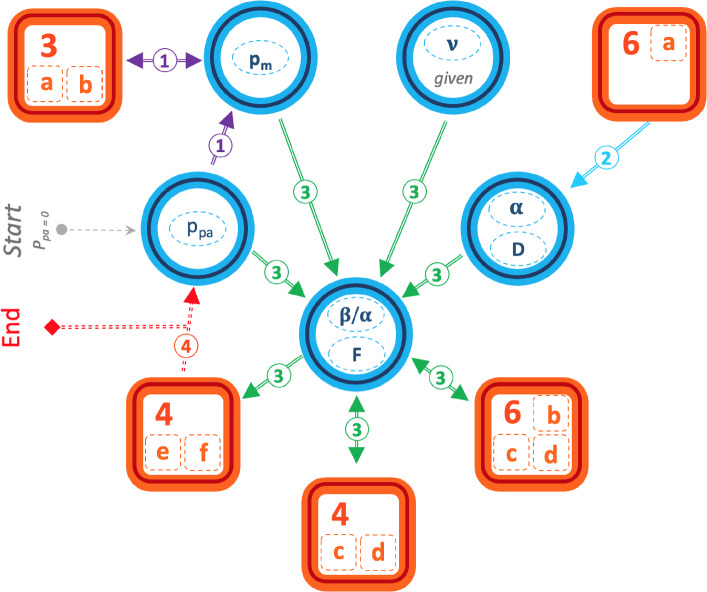

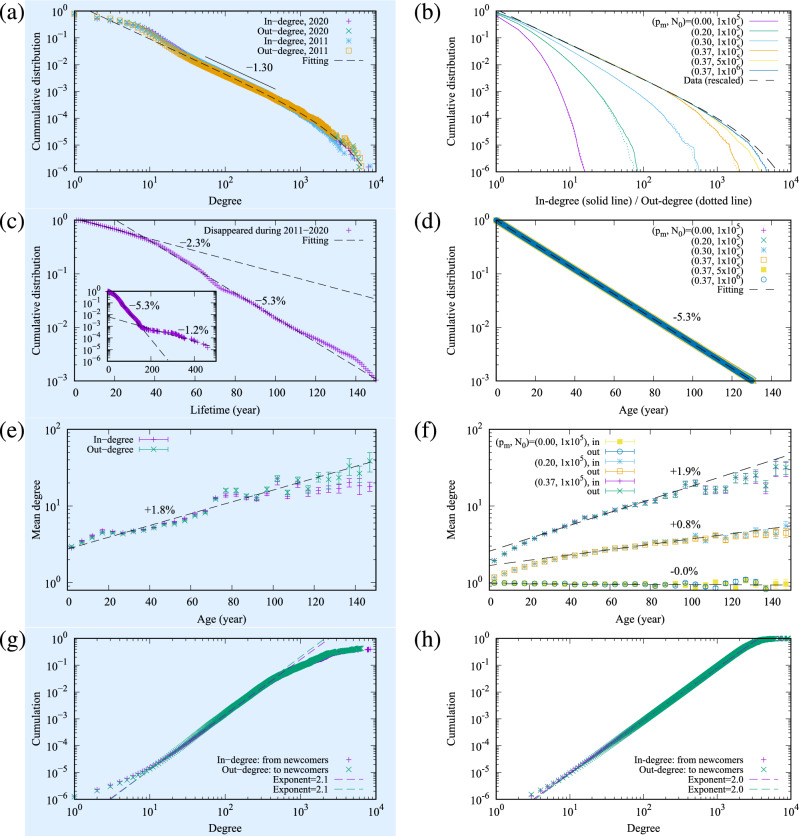

We develop a single two-layered model framework that captures and replicates both the statistical properties of the network as well as those of the intrinsic quantities of the agents. Our model framework consists of two distinct yet connected elements that were previously only studied in isolation, namely methods related to temporal network structures and those associated with money transport flows. Within this context, the network structure emerges from the first layer and its topological structure is transferred to the second layer associated with the money transactions. In this manner, we can explain how the micro-level dynamics of the agents within the network lead to the exogenous manifestation of the aggregated system statistical data en-wrapping the very same agents within the system. This is done by capturing the essential dynamics of collective motion in complex networks that enable the simultaneous emergence of tent-shaped distributions in growth rates within the agents, together with the emergence of scaling properties within the network in the study. We can validate the model framework and dynamics by applying these to the context of the real-world inter-firm trading network of firms in Japan and comparing the results of the statistical distributions at both network and agent levels in a temporal manner. In particular, we compare our results to the fundamental quantities supporting the seven empirical laws observed in data: the degree distribution, the mean degree growth rate over time, the age distribution of the firms, the preferential attachment, the sales distribution in steady states, their growth rates, their scaling relations generated by the model. We find these results to be nearly identical to the real-world data. The framework has the potential to be transformed into a forecasting tool to support decision-makers on financial and prudential policies.

我们开发了一个单一的双层模型框架,该框架能够捕捉并复制网络的统计特性以及主体内在量的统计特性。我们的模型框架由两个不同但相互关联的元素组成,这两个元素以前只是单独进行研究,即与时间网络结构相关的方法和与货币流动相关的方法。在此背景下,网络结构从第一层出现,其拓扑结构被转移到与货币交易相关的第二层。通过这种方式,我们可以解释网络中主体的微观层面动态如何导致系统统计数据的外在表现,而这些统计数据又将系统中的同一批主体包裹在内。这是通过捕捉复杂网络中集体运动的基本动态来实现的,这些动态使得主体内部增长率出现帐篷状分布,同时研究中的网络也出现标度特性。我们可以将该模型框架和动态应用于日本企业间实际交易网络的背景中,并以时间序列的方式比较网络和主体层面的统计分布结果,从而验证该模型框架和动态。特别是,我们将我们的结果与支持数据中观察到的七条经验定律的基本量进行比较:度分布、随时间的平均度增长率、企业的年龄分布、优先连接、稳态下的销售分布、它们的增长率以及模型产生的标度关系。我们发现这些结果与实际数据几乎相同。该框架有潜力转化为一种预测工具,以支持决策者制定金融和审慎政策。