Division of Hospital Medicine, Department of Medicine, University of California San Francisco, San Francisco, CA, United States.

Tufts University School of Medicine, Boston, MA, United States.

JMIR Form Res. 2024 Aug 27;8:e56327. doi: 10.2196/56327.

The rise of telehealth and telemedicine during the pandemic allowed patients and providers to develop a sense of comfort with telehealth, which may have increased the demand for virtual-first care solutions with spillover effects into venture capital funding.

We aimed to understand the size and type of digital health investments occurring in the prepandemic and pandemic periods.

We examined health care companies founded from March 14, 2019, to March 14, 2020 (prepandemic) versus those founded from March 15, 2020, to March 14, 2022, after pandemic onset. Data were obtained from Crunchbase, a publicly available database that catalogs information about venture capital investments for companies. We also compared companies founded prepandemic to those founded after the first year of the pandemic (pandemic steady-state). We performed a Wilcoxon rank sum test to compare median funding amounts. We compared the 2 groups of companies according to the type of funding round raised, geography, health care subcategory, total amount of funding per year since founding, and number of founders.

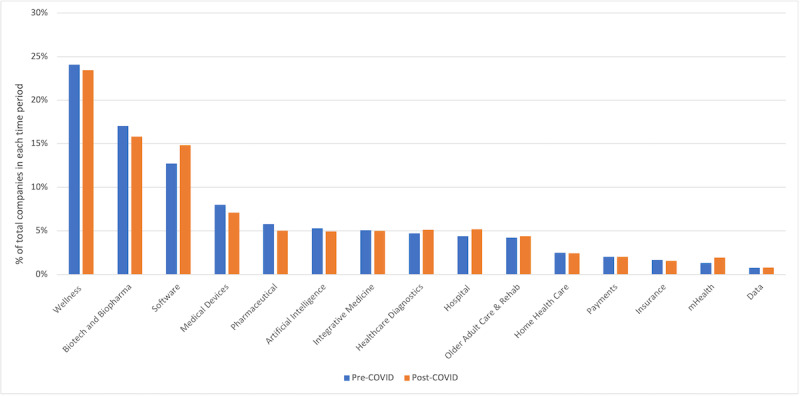

There were 2714 and 2218 companies founded prepandemic and during the pandemic, respectively. The companies were similarly distributed across geographies in the prepandemic and pandemic periods (P=.46) with no significant differences in the number of founders (P=.32). There was a significant difference in total funding per year since founding between prepandemic and pandemic companies (US $10.8 million vs US $20.9 million; P<.001). The distribution of funding rounds differed significantly for companies founded in prepandemic and pandemic periods (P<.001). On excluding data from the first year of the pandemic, there were 581 companies founded in the pandemic steady-state period from March 14, 2021, to March 14, 2022. Companies founded prepandemic had a significantly greater mean number of founders than those founded during the pandemic (P=.02). There was no significant difference in total funding per year since founding between prepandemic and steady-state pandemic companies (US $10.8 million vs US $14.4 million; P=.34). The most common types of health care companies included wellness, biotech/biopharma, and software companies. Distributions of companies across health care subcategories were not significantly different before and during the pandemic. However, significant differences were identified when data from the first year of the pandemic were excluded (P<.001). Companies founded during the steady-state pandemic period were significantly more likely to be classified as artificial intelligence (7.3% vs 4.7%; P=.005), software (17.3% vs 12.7%; P=.002), and insurance (3.3% vs 1.7%; P=.003), and were significantly less likely to be classified as health care diagnostics (2.4% vs 5.1%; P=.002).

We demonstrate no significant changes in the types of health care companies founded before versus during the pandemic, although significant differences emerge when comparing prepandemic companies to those founded after the first year of the pandemic.

在大流行期间,远程医疗和远程医疗的兴起使患者和提供者对远程医疗有了一定的舒适度,这可能增加了对虚拟优先护理解决方案的需求,并对风险投资资金产生溢出效应。

我们旨在了解大流行前后数字健康投资的规模和类型。

我们检查了 2019 年 3 月 14 日至 2020 年 3 月 14 日(大流行前)与 2020 年 3 月 15 日至 2022 年 3 月 14 日(大流行后)成立的医疗保健公司。数据来自 Crunchbase,这是一个公共可用的数据库,用于记录有关公司风险投资的信息。我们还将大流行前成立的公司与大流行后第一年(大流行稳定期)成立的公司进行了比较。我们使用 Wilcoxon 秩和检验来比较中位数的资金数额。我们根据筹集资金轮次的类型、地理位置、医疗保健子类别、自成立以来每年的总资金量以及创始人数量对这两组公司进行了比较。

大流行前和大流行期间分别有 2714 家和 2218 家公司成立。在大流行前和大流行期间,这些公司在地理位置上的分布相似(P=.46),创始人人数没有显著差异(P=.32)。大流行前和大流行期间公司的自成立以来每年的总资金量存在显著差异(US $10.8 百万 vs US $20.9 百万;P<.001)。大流行前和大流行期间成立的公司的资金轮次分布存在显著差异(P<.001)。排除大流行第一年的数据后,从 2021 年 3 月 14 日到 2022 年 3 月 14 日,大流行稳定期共有 581 家公司成立。大流行前成立的公司创始人人数明显多于大流行期间成立的公司(P=.02)。大流行前和稳定期大流行期间公司的自成立以来每年的总资金量没有显著差异(US $10.8 百万 vs US $14.4 百万;P=.34)。最常见的医疗保健公司类型包括健康、生物技术/生物制药和软件公司。在大流行前后,公司在医疗保健子类别中的分布没有显著差异。然而,当排除大流行第一年的数据时,发现了显著差异(P<.001)。在大流行稳定期成立的公司被归类为人工智能(7.3% vs 4.7%;P=.005)、软件(17.3% vs 12.7%;P=.002)和保险(3.3% vs 1.7%;P=.003)的可能性显著更高,而被归类为医疗保健诊断(2.4% vs 5.1%;P=.002)的可能性显著更低。

我们证明,在大流行前后成立的医疗保健公司类型没有显著变化,尽管将大流行前的公司与大流行后第一年成立的公司进行比较时,会出现显著差异。