Boston Strategic Partners, Boston, MA, United States.

J Med Internet Res. 2023 Jul 31;25:e35857. doi: 10.2196/35857.

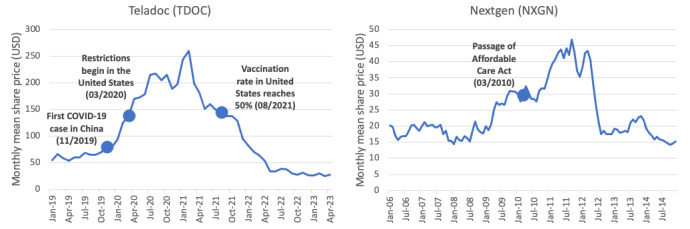

The telehealth sector of health care delivery experienced significant growth at the start of the pandemic as web-based care quickly became essential for the ongoing safety of patients and health care providers, such as clinicians and other health care professionals. After vaccines were introduced, however, telehealth companies lost value as the need for web-based care appeared to lessen. Presently, both existing telehealth companies and new entrants to the space are seeking ways to innovate, gain investor and customer buy-in, and overcome competitors. New companies are hoping to be seen not as pandemic-era substitutes, but instead as reinforcements to in-person care, valuable in their own right thanks to the convenience and technological advancements they bring. This struggle to reframe the value proposition, or perceived benefit, of telehealth is reflected in fluctuating stock prices and dropping valuations. This viewpoint summarizes the market volatility seen in the telehealth sector since the start of the COVID-19 pandemic and suggests potential opportunities for growth in the space. This is accomplished through a qualitative secondary research approach, leveraging contemporary sources, financial references such as Yahoo! Finance, and peer-reviewed literature to support predictions for the future market. We found that, in 2020, the size of the US telehealth market rose to US $17.9 billion and is estimated to reach US $140.7 billion by 2030. Additionally, digital health venture funding nearly doubled in 2020 over the prior 2 years with total funding rising to US $14.1 billion. However, these factors produced an oversaturated market in which the volume of supply was higher than demand, resulting in a sharp drop in valuations for some as vaccination rates climbed in 2021. In the face of this rebalancing, or return to normal following excessively high or unsustainable valuations, we suggest a possible path forward for telehealth companies in the postpandemic era. Suppliers' current role in the telehealth space-whether health care industry incumbents, that is, traditional health care delivery systems and companies, or "telehealth-first" challengers-are especially relevant to the specific growth strategies they should pursue. Furthermore, consideration of the areas of medicine and characteristics that best lend themselves to web-based care may lead to a greater chance for long-term success in a postpandemic health care delivery system. In the future, we believe investors should expect a bullish market, that is, one characterized by growing share prices. Success is likely to occur in part through changing the actual models of care, as opposed to moving traditional care to a web-based format. The oversaturated market will likely condense into select established telehealth giants who were able to adapt to the changing landscape. While investors may be reasonably hesitant regarding individual telehealth companies, the industry can expect slowed but continued growth.

在大流行开始时,医疗保健提供领域的远程医疗经历了显著的增长,因为基于网络的护理迅速成为患者和医疗保健提供者(如临床医生和其他医疗保健专业人员)持续安全的必要条件。然而,在引入疫苗后,随着对基于网络的护理的需求似乎减少,远程医疗公司的价值下降。目前,现有的远程医疗公司和该领域的新进入者都在寻找创新的方法,获得投资者和客户的认可,并克服竞争对手。新公司希望被视为不仅仅是大流行时期的替代品,而是作为面对面护理的补充,由于它们带来的便利性和技术进步,它们本身就具有价值。这种重新构建远程医疗的价值主张或感知收益的努力反映在波动的股价和不断下降的估值中。这一观点总结了自 COVID-19 大流行开始以来远程医疗领域的市场波动,并为该领域的未来增长提供了潜在机会。这是通过定性的二次研究方法实现的,利用当代资源、雅虎金融等金融参考资料以及同行评议文献来支持对未来市场的预测。我们发现,2020 年,美国远程医疗市场规模增长到 179 亿美元,预计到 2030 年将达到 1407 亿美元。此外,2020 年数字医疗风险投资几乎是前两年的两倍,总投资上升至 141 亿美元。然而,这些因素导致了一个供过于求的市场,供应数量高于需求,导致一些公司的估值在 2021 年疫苗接种率上升时大幅下降。面对这种再平衡,或者说在过高或不可持续的估值之后回归正常,我们为大流行后时代的远程医疗公司提出了一个可能的前进道路。供应商在远程医疗领域的当前角色——无论是医疗保健行业的现有企业,即传统的医疗保健提供系统和公司,还是“远程医疗优先”的挑战者——对于他们应该追求的具体增长战略特别重要。此外,考虑到最适合基于网络的护理的医学领域和特征,可能会增加在大流行后医疗保健提供系统中取得长期成功的机会。未来,我们相信投资者将预期市场看涨,也就是说,股价不断上涨。成功可能部分是通过改变实际的护理模式,而不是将传统护理转移到基于网络的模式。供过于求的市场可能会集中到少数能够适应不断变化的格局的成熟远程医疗巨头。虽然投资者对个别远程医疗公司可能会有合理的犹豫,但该行业预计将继续保持缓慢但持续的增长。