Etter-Phoya Rachel, Murray Stuart, Hall Stephen, Masiya Michael, O'Hare Bernadette

School of Medicine, The University of St Andrews, St Andrews, United Kingdom.

Tax Justice Network, Lilongwe, Malawi.

PLOS Glob Public Health. 2025 Mar 19;5(3):e0004218. doi: 10.1371/journal.pgph.0004218. eCollection 2025.

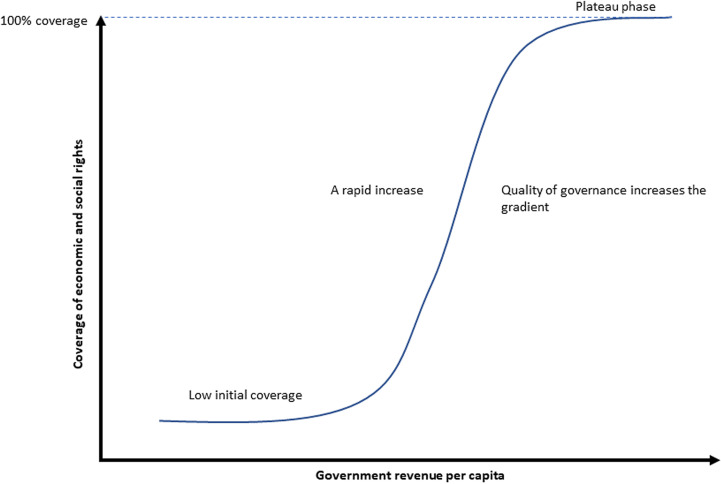

The United Nations Universal Declaration of Human Rights states that everyone is entitled to economic and social rights essential to survive and thrive (Articles 25 and 26) and everyone is entitled to a social and international order in which their rights and freedom can be realised (Article 28). These rights must be ensured through national efforts and international cooperation (Article 22), but many millions of people worldwide do not access their rights, including the right to clean drinking water, safe sanitation, healthcare, and education. Government revenue from taxes plays a crucial role in ensuring these rights. However, globally, 10% of corporate tax revenue is lost because multinational corporations shift their profits from where they operate. This study examines the impact of profit shifting on tax revenue in Nigeria, focussing on access to economic and social rights and governance. It estimates the impact of revenue gains made on profits shifted from Nigeria to European tax havens, using data on profits shifted published by Wier and Zucman in 2022 and the Government Revenue and Development Estimations (GRADE) model for the estimations. The findings reveal that if the Nigerian government had additional revenue equivalent to tax losses, an additional 500,000 Nigerians would have their right to drink clean water and nearly 800,000 their right to use basic sanitation each day, 150,000 children would have their right to education, and 11 children would have their right to survive each day (amounting to 4,063 children each year). Increased revenue would also improve governance. In contrast, the gains European tax havens make as destinations for shifted profits in terms of rights are almost negligible, given that almost all Europeans have those economic and social rights discussed in this paper fulfilled. The tax reforms championed by the Organisation for Economic Co-operation and Development (OECD), including 27 European member nations, to tackle aggressive corporate tax avoidance and tax evasion-in short, tax abuse-fall short of ensuring a suitable international order for rights to be achieved. To remedy this, all European countries must support negotiations on international tax cooperation at the United Nations. This should include reforms on regulating multinational corporations, particularly through unitary taxation with formulary apportionment. In the short- and medium-term, interim measures to mitigate the harmful impacts of profit shifting are necessary. Countries must take steps to raise the global minimum corporate tax rate, introduce unilateral measures to tax multinational corporations, improve tax transparency and information sharing with lower-income countries, and strengthen anti-avoidance rules.

《联合国世界人权宣言》指出,人人有权享有为维持生存和蓬勃发展所必需的经济和社会权利(第二十五条和第二十六条),人人有权享有能使这些权利和自由得到实现的社会和国际秩序(第二十八条)。这些权利必须通过国家努力和国际合作来保障(第二十二条),但全球仍有数百万人无法享有其权利,包括获得清洁饮用水、安全卫生设施、医疗保健和教育的权利。政府税收在保障这些权利方面发挥着关键作用。然而,在全球范围内,10%的公司税收流失,原因是跨国公司将利润从其运营地转移。本研究考察了利润转移对尼日利亚税收的影响,重点关注经济和社会权利的获取以及治理情况。研究利用维尔和祖克曼于2022年公布的利润转移数据以及政府收入与发展估算(GRADE)模型,估算了从尼日利亚转移至欧洲避税天堂的利润所带来的税收增加的影响。研究结果表明,如果尼日利亚政府获得相当于税收损失的额外收入,每天将有额外50万尼日利亚人能够享有清洁饮用水的权利,近80万人能够享有使用基本卫生设施的权利,15万名儿童能够享有受教育的权利,每天将有11名儿童能够享有生存的权利(每年共计4063名儿童)。增加的收入还将改善治理。相比之下,鉴于几乎所有欧洲人都已实现本文所讨论的那些经济和社会权利,欧洲避税天堂作为转移利润目的地在权利方面所获得的收益几乎可以忽略不计。经济合作与发展组织(经合组织)倡导的税收改革,包括27个欧洲成员国,旨在应对激进的公司避税和逃税行为——简而言之,即税收滥用——但在确保实现权利的适当国际秩序方面仍有不足。为弥补这一不足,所有欧洲国家必须支持在联合国进行国际税收合作谈判。这应包括对跨国公司监管的改革,特别是通过统一征税和公式分摊法。在短期和中期,采取临时措施减轻利润转移的有害影响是必要的。各国必须采取措施提高全球公司最低税率,出台对跨国公司征税的单边措施,提高税收透明度并与低收入国家共享信息,以及加强反避税规则。