Postma Doerine J, De Smet Peter A G M, Mantel-Teeuwisse Aukje K, Leufkens Hubert G M, Notenboom Kim

Utrecht Institute for Pharmaceutical Sciences (UIPS), Division of Pharmacoepidemiology & Clinical Pharmacology, Utrecht University, Utrecht, The Netherlands.

Royal Dutch Association for the Advancement of Pharmacy, Den Haag, The Netherlands.

BMJ Open. 2025 Apr 10;15(4):e099697. doi: 10.1136/bmjopen-2025-099697.

To assess the upstream pharmaceutical supply chains of 10 high-use pharmaceuticals to detect vulnerabilities that may increase the risk of medicine shortages.

Cohort study.

Dutch outpatient setting in 2022.

A total of 407 authorised medicinal products for 10 pharmaceutical substances with the largest number of outpatients.

The diversity of active pharmaceutical ingredient (API) and finished pharmaceutical product (FPP) manufacturers, their geographic locations and the interdependencies between these manufacturers and marketing authorisation holders (MAHs).

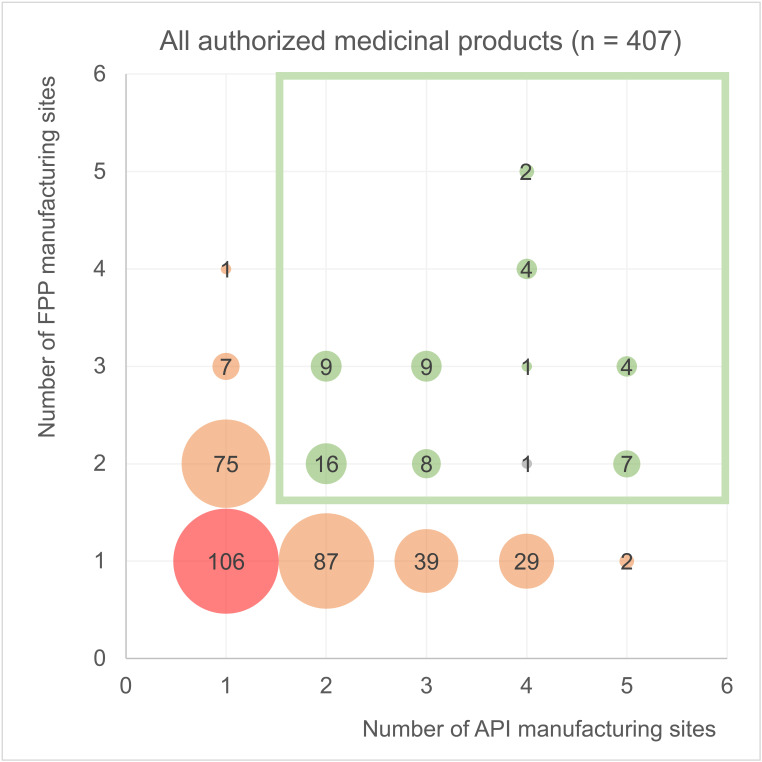

For the 407 authorised medicinal products, 50 of the 90 API manufacturing sites were in Asia, and 38 were in Europe. For five pharmaceutical substances, most of the API sites were located outside Europe. Of the 128 FPP manufacturing sites, 94 were in Europe and 31 in Asia. For all 10 substances, at least 47% of FPP sites were located in Europe. API manufacturing for 122 of the 407 products (30%) was entirely performed outside Europe, and FPP manufacturing for 66 of the 407 products (16%). For four substances, more than half of the products depended on API manufacturing outside Europe. The number of distinct API and FPP manufacturing sites per substance was at least four. For amoxicillin, 16 of the 32 products (50%) entirely depended on one and the same API site. For omeprazole, 39 of the 85 products (46%) entirely depended on one and the same FPP site. MAHs applied dual sourcing for API and FPP manufacturing for 61 (15%) of the authorised medicinal products. For three pharmaceutical substances, none of the authorised medicinal products listed at least two API and FPP manufacturing sites.

Our study of the supply chains of high-use pharmaceutical substances indicates the need for a granular assessment of the interdependencies between MAHs, API and FPP manufacturers to identify upstream supply chain vulnerabilities.

评估10种高使用量药品的上游药品供应链,以发现可能增加药品短缺风险的脆弱性。

队列研究。

2022年荷兰门诊环境。

共有407种针对10种门诊量最大的药物物质的获批药品。

活性药物成分(API)和成品药(FPP)制造商的多样性、其地理位置以及这些制造商与上市许可持有人(MAH)之间的相互依存关系。

对于407种获批药品,90个API生产基地中有50个在亚洲,38个在欧洲。对于5种药物物质,大多数API生产基地位于欧洲以外。在128个FPP生产基地中,94个在欧洲,31个在亚洲。对于所有10种药物物质,至少47%的FPP生产基地位于欧洲。407种产品中有122种(30%)的API生产完全在欧洲以外进行,407种产品中有66种(16%)的FPP生产在欧洲以外进行。对于4种药物物质,超过一半的产品依赖欧洲以外的API生产。每种药物物质的不同API和FPP生产基地数量至少为4个。对于阿莫西林,32种产品中有16种(50%)完全依赖同一个API生产基地。对于奥美拉唑,85种产品中有39种(46%)完全依赖同一个FPP生产基地。MAH对61种(15%)获批药品的API和FPP生产采用双重采购。对于3种药物物质,没有一种获批药品列出至少两个API和FPP生产基地。

我们对高使用量药物物质供应链的研究表明,需要对MAH、API和FPP制造商之间的相互依存关系进行细致评估,以识别上游供应链的脆弱性。