Department of Psychology, University of Denver, Denver, CO, USA.

Sci Rep. 2020 Jun 18;10(1):9878. doi: 10.1038/s41598-020-66502-y.

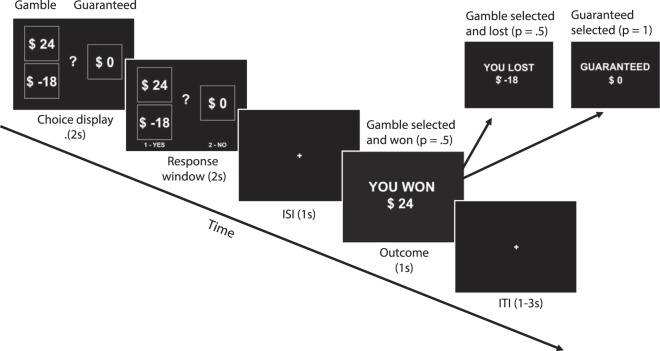

Forty years ago, prospect theory introduced the notion that risky options are evaluated relative to their recent context, causing a significant shift in the study of risky monetary decision-making in psychology, economics, and neuroscience. Despite the central role of past experiences, it remains unclear whether, how, and how much past experiences quantitatively influence risky monetary choices moment-to-moment in a nominally learning-free setting. We analyzed a large dataset of risky monetary choices with trial-by-trial feedback to quantify how past experiences, or recent events, influence risky choice behavior and the underlying processes. We found larger recent outcomes both negatively influence subsequent risk-taking and positively influence the weight put on potential losses. Using a hierarchical Bayesian framework to fit a modified version of prospect theory, we demonstrated that the same risks will be evaluated differently given different past experiences. The computations underlying risky decision-making are fundamentally dynamic, even if the environment is not.

四十年前,前景理论引入了这样一种观点,即风险选项是相对于其最近的上下文进行评估的,这导致了心理学、经济学和神经科学中对风险货币决策研究的重大转变。尽管过去的经验起着核心作用,但目前尚不清楚过去的经验是否以及在多大程度上会在名义上无学习的环境中对风险货币选择进行实时、定量地影响。我们分析了一个带有逐次反馈的风险货币选择的大型数据集,以量化过去的经验或最近的事件如何影响风险选择行为和潜在的过程。我们发现,更大的近期结果既会对后续冒险行为产生负面影响,也会对潜在损失的权重产生正面影响。我们使用分层贝叶斯框架来拟合前景理论的一个修改版本,证明了在不同的过去经验下,相同的风险将被不同地评估。即使环境没有变化,风险决策的计算基础也是动态的。