Ding Wenzhi, Levine Ross, Lin Chen, Xie Wensi

Faculty of Business and Economics, The University of Hong Kong, K.K. Leung Building, Pok fu lam Road, Hong Kong.

Haas School of Business at the University of California, Berkeley, 545 Student Services Building, Berkeley, CA 94720, United States.

J financ econ. 2021 Aug;141(2):802-830. doi: 10.1016/j.jfineco.2021.03.005. Epub 2021 Mar 7.

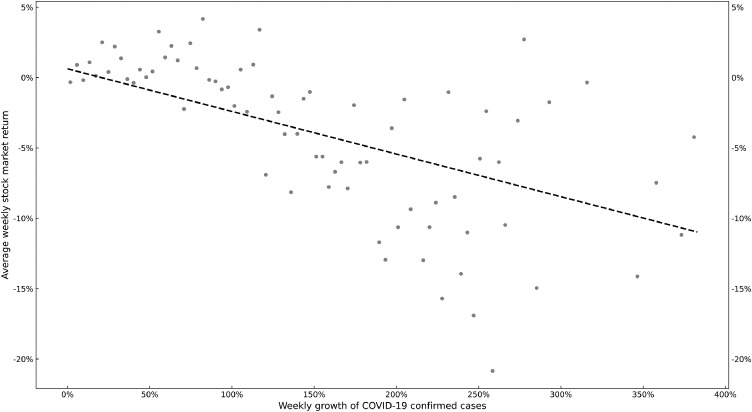

We evaluate the connection between corporate characteristics and the reaction of stock returns to COVID-19 cases using data on more than 6,700 firms across 61 economies. The pandemic-induced drop in stock returns was milder among firms with stronger pre-2020 finances (more cash and undrawn credit, less total and short-term debt, and larger profits), less exposure to COVID-19 through global supply chains and customer locations, more corporate social responsibility activities, and less entrenched executives. Furthermore, the stock returns of firms controlled by families (especially through direct holdings and with non-family managers), large corporations, and governments performed better, and those with greater ownership by hedge funds and other asset management companies performed worse. Stock markets positively price small amounts of managerial ownership but negatively price high levels of managerial ownership during the pandemic.

我们利用61个经济体中6700多家公司的数据,评估公司特征与股票回报对新冠疫情案例反应之间的联系。在2020年之前财务状况更强(现金和未动用信贷更多、总债务和短期债务更少、利润更大)、通过全球供应链和客户所在地受新冠疫情影响更小、企业社会责任活动更多以及高管权力受到更少限制的公司中,疫情引发的股票回报下降幅度较小。此外,由家族控制(特别是通过直接持股且有非家族经理)、大公司和政府控制的公司的股票回报表现更好,而由对冲基金和其他资产管理公司持股比例更高的公司表现更差。在疫情期间,股票市场对少量管理层持股给予正向定价,但对高水平管理层持股给予负向定价。