O'Donnell Niall, Shannon Darren, Sheehan Barry

University of Limerick, Ireland.

J Behav Exp Finance. 2021 Jun;30:100477. doi: 10.1016/j.jbef.2021.100477. Epub 2021 Feb 18.

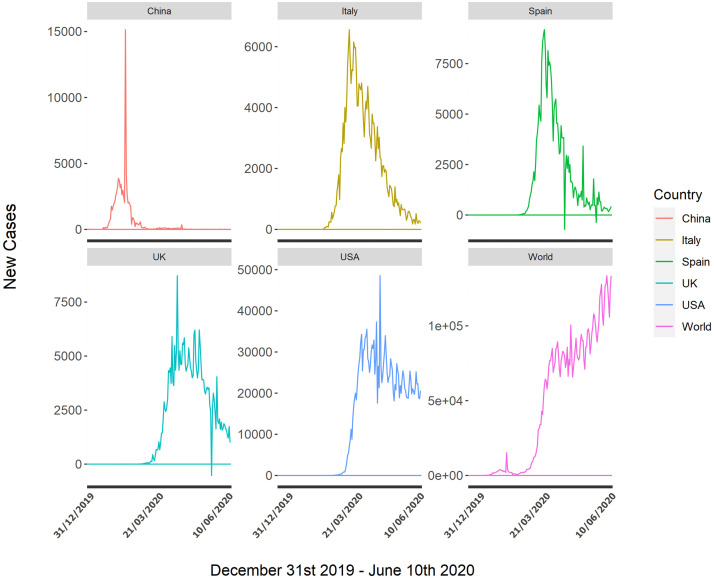

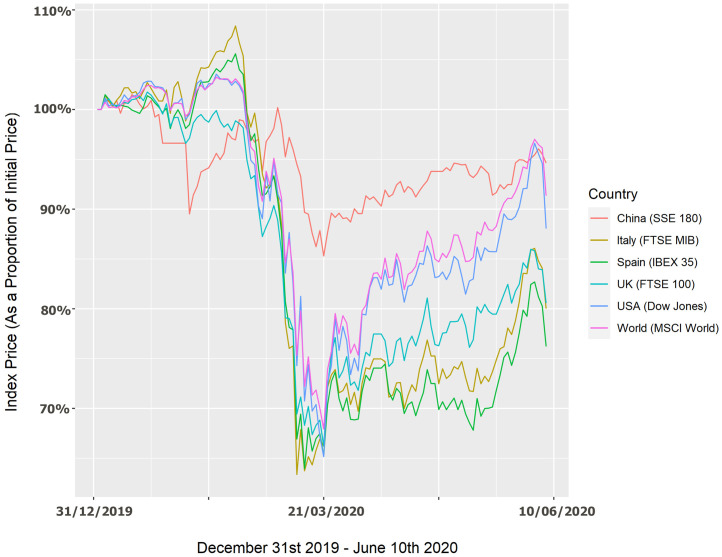

The closure of borders and traditional commerce due to the COVID-19 pandemic is expected to have a lasting financial impact. We determine whether the growth in COVID-19 affected index prices by examining equity markets in five regional epicentres, along with a 'global' index. We also investigate the impact of COVID-19 after controlling for investor sentiment, credit risk, liquidity risk, safe-haven asset demand and the price of oil. Despite controlling for these traditional market drivers, the daily totals of COVID-19 cases nevertheless explained index price changes in Spain, Italy, the United Kingdom and the United States. Similar results were not observed in China, the origin of the virus, nor in the 'global' index (MSCI World). Our results suggest that early interventions (China) and the spatiotemporal nature of pandemic epicentres (World) should be considered by governments, regulators and relevant stakeholders in the event of future COVID-19 'waves' or further extreme societal disruptions.

由于新冠疫情导致边境和传统商业关闭,预计将产生持久的财务影响。我们通过研究五个地区疫情中心的股票市场以及一个“全球”指数,来确定新冠疫情的增长是否影响了指数价格。我们还在控制了投资者情绪、信用风险、流动性风险、避险资产需求和油价之后,研究了新冠疫情的影响。尽管控制了这些传统市场驱动因素,但新冠疫情病例的每日总数仍解释了西班牙、意大利、英国和美国的指数价格变化。在病毒起源地中国以及“全球”指数(MSCI世界指数)中未观察到类似结果。我们的结果表明,在未来出现新冠疫情“浪潮”或进一步的极端社会破坏事件时,政府、监管机构和相关利益攸关方应考虑早期干预措施(中国)以及疫情中心的时空特性(全球)。