Gharib Cheima, Mefteh-Wali Salma, Serret Vanessa, Ben Jabeur Sami

Laboratoire Interdisciplinaire des Environnements Continentaux (LIEC), UMR 7360 CNRS, Université de Lorraine, Bâtiment IBiSE - Campus Bridoux - 8 rue du Général Delestraint, F-57070, METZ, France.

ESSCA School of Management, 1 rue Lakanal, 49003, Angers, France.

Resour Policy. 2021 Dec;74:102392. doi: 10.1016/j.resourpol.2021.102392. Epub 2021 Oct 4.

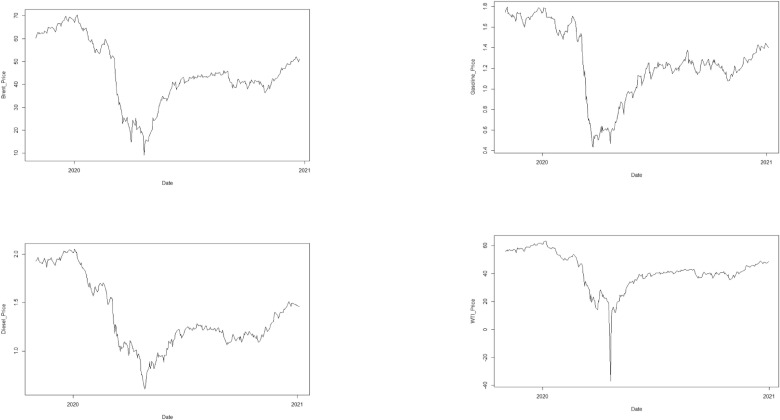

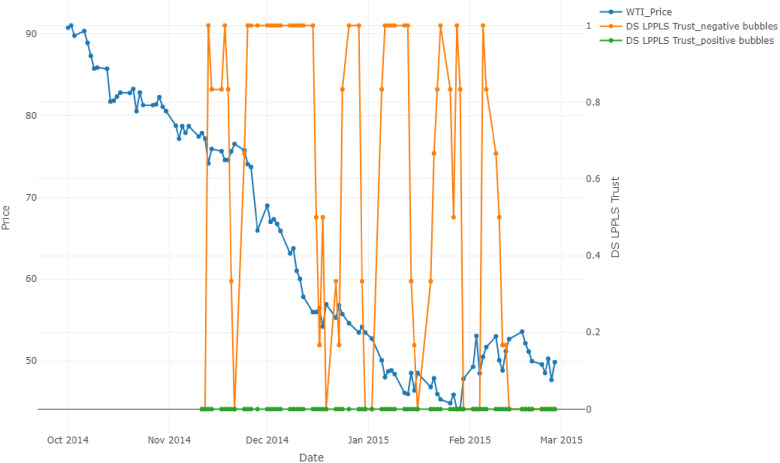

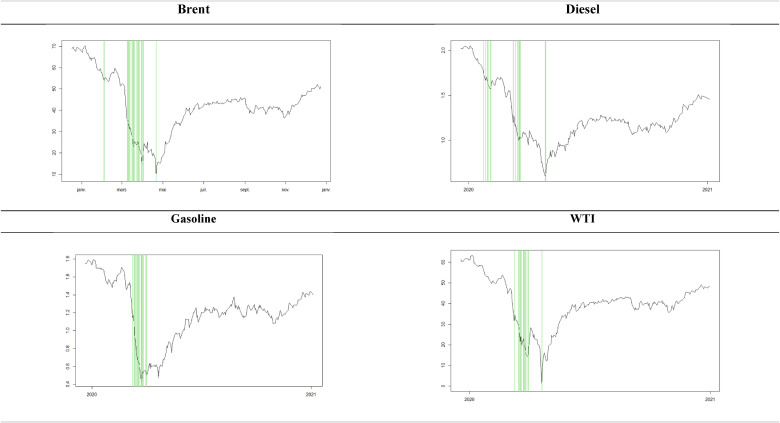

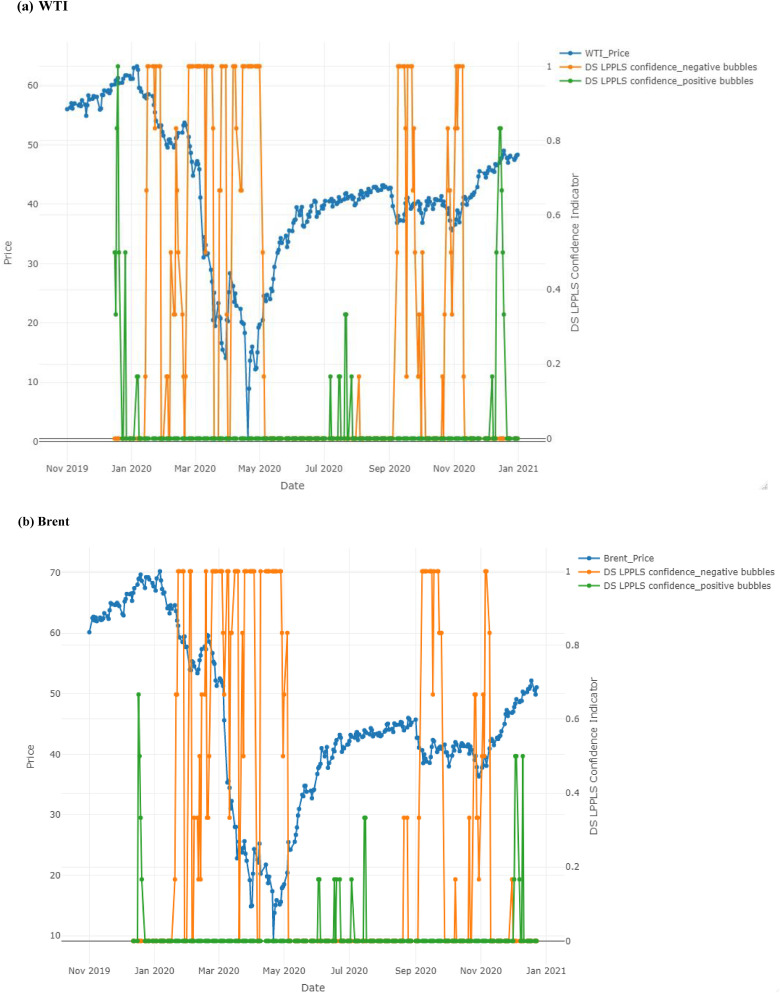

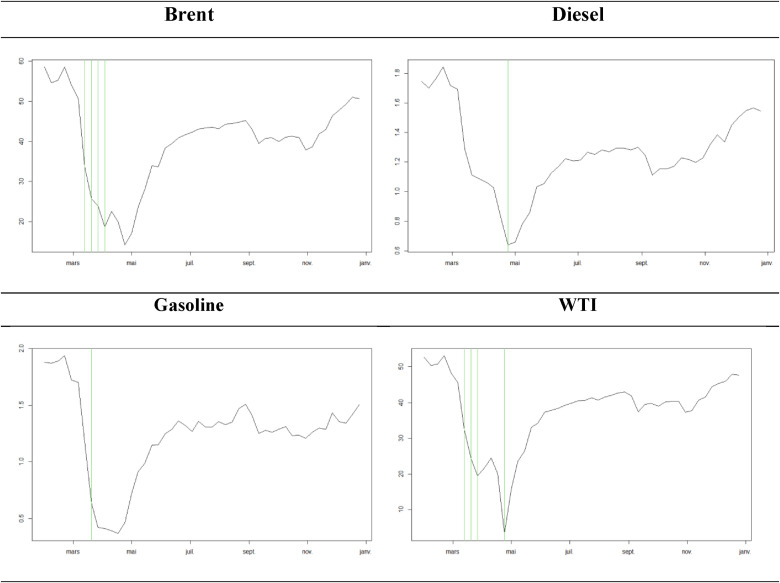

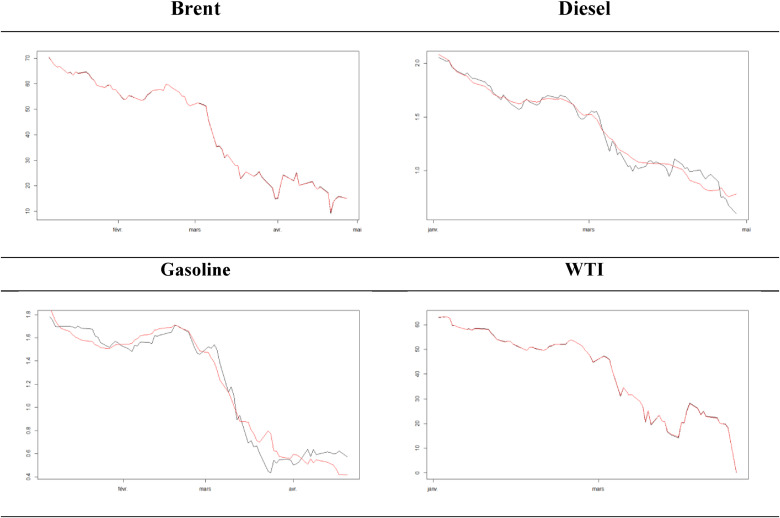

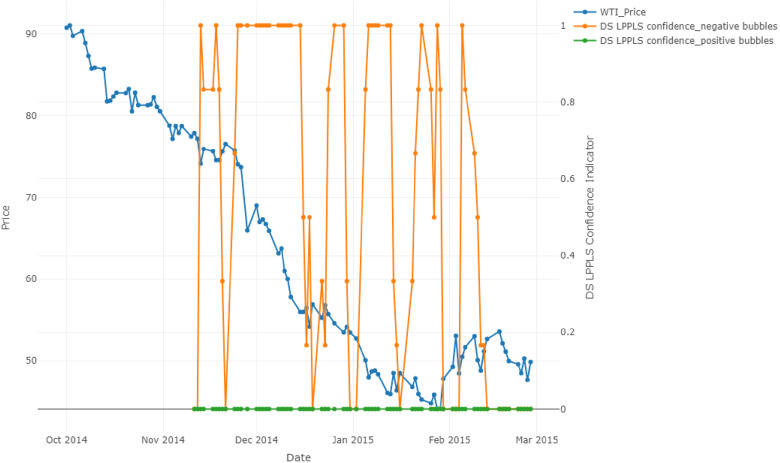

This paper provides an analysis of crude oil, diesel, and gasoline prices for the period from November 1, 2019 to December 31, 2020. We apply Log Periodic Power-Law Singularity (LPPLS) and Discrete Scale LPPLS bubble indicators to explore the dynamic bubbles of oil prices and predict their crash times. The results indicate that West Texas Light crude oil and North Sea Brent crude oil experienced a statistically significant negative financial bubble during the COVID-19 outbreak. In addition, gasoline and diesel prices are mainly driven by fundamentals. Our findings are expected to be useful to oil market investors, policymakers, and energy experts.

本文分析了2019年11月1日至2020年12月31日期间的原油、柴油和汽油价格。我们应用对数周期幂律奇点(LPPLS)和离散尺度LPPLS泡沫指标来探索油价的动态泡沫,并预测其崩溃时间。结果表明,在新冠疫情爆发期间,西德克萨斯轻质原油和北海布伦特原油经历了具有统计学意义的负金融泡沫。此外,汽油和柴油价格主要由基本面因素驱动。我们的研究结果有望对石油市场投资者、政策制定者和能源专家有所帮助。