Liu Zhifeng, Huynh Toan Luu Duc, Dai Peng-Fei

Management School, Hainan University, Haikou, China.

Supply Chain and Logistics Optimization Research Center, University of Windsor, Windsor, Canada.

Res Int Bus Finance. 2021 Oct;57:101419. doi: 10.1016/j.ribaf.2021.101419. Epub 2021 Apr 9.

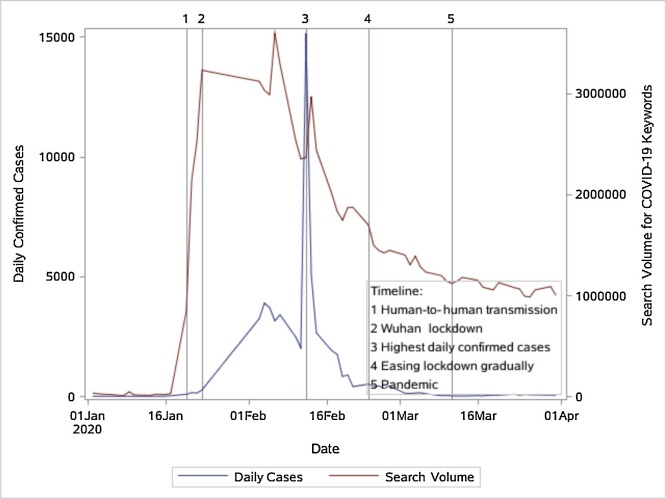

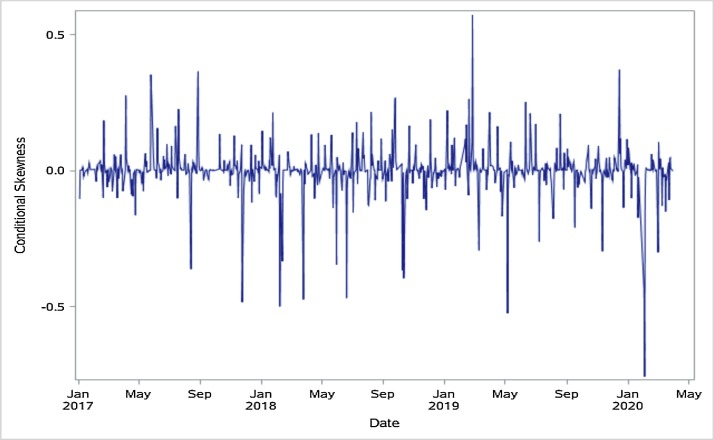

This study investigates the impact of the COVID-19 pandemic on the stock market crash risk in China. For this purpose, we first estimated the conditional skewness of the return distribution from a GARCH with skewness (GARCH-S) model as the proxy for the equity market crash risk of the Shanghai Stock Exchange. We then constructed a fear index for COVID-19 using data from the Baidu Index. Based on the findings, conditional skewness reacts negatively to daily growth in total confirmed cases, indicating that the pandemic increases stock market crash risk. Moreover, the fear sentiment exacerbates such risk, especially with regard to the impact of COVID-19. In other words, when the fear sentiment is high, the stock market crash risk is more strongly affected by the pandemic. Our evidence is robust for the number of daily deaths and global cases.

本研究考察了新冠疫情对中国股市崩盘风险的影响。为此,我们首先从一个带偏度的广义自回归条件异方差模型(GARCH-S)估计收益分布的条件偏度,以此作为上海证券交易所股票市场崩盘风险的代理变量。然后,我们利用百度指数的数据构建了一个新冠疫情恐惧指数。基于研究结果,条件偏度对每日确诊病例总数的增长呈负向反应,这表明疫情会增加股市崩盘风险。此外,恐惧情绪会加剧这种风险,尤其是在新冠疫情的影响方面。换句话说,当恐惧情绪高涨时,股市崩盘风险受疫情的影响更强。我们的证据对于每日死亡人数和全球病例数而言是稳健的。