Dey Asim K, Hoque G M Toufiqul, Das Kumer P, Panovska Irina

Department of Mathematical Sciences, University of Texas at El Paso, El Paso, TX 79968, USA.

Department of Electrical and & Computer Engineering, Princeton University, Princeton, NJ 08544, USA.

Physica A. 2022 Mar 1;589:126423. doi: 10.1016/j.physa.2021.126423. Epub 2021 Sep 30.

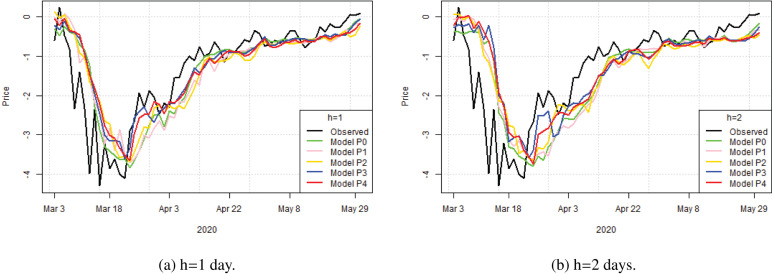

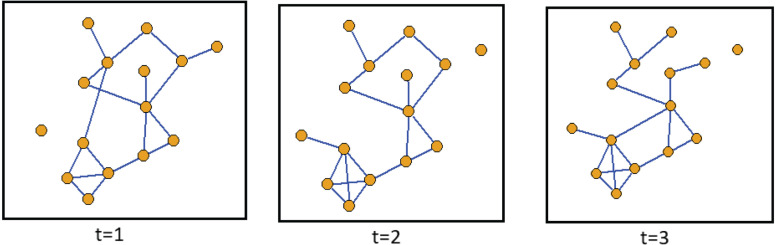

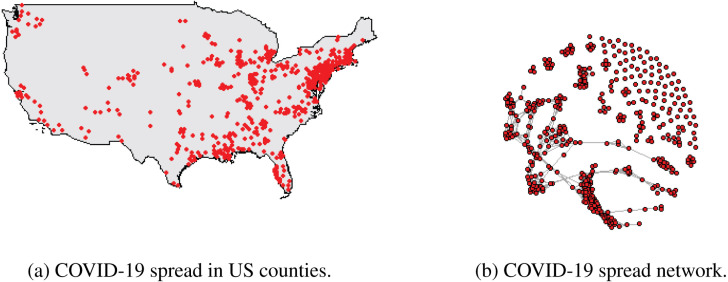

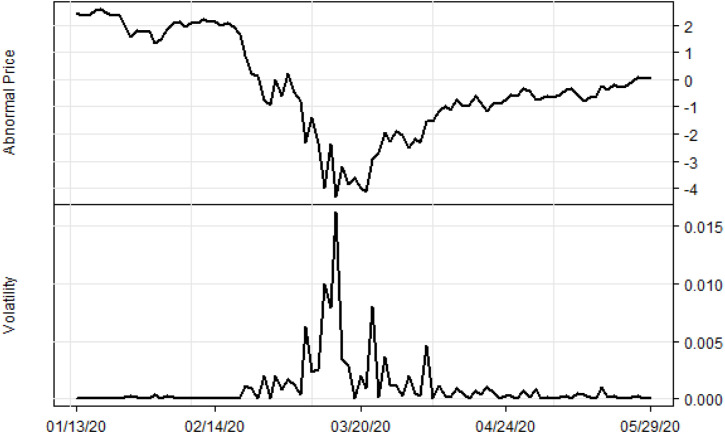

We develop a novel temporal complex network approach to quantify the US county level spread dynamics of COVID-19. We use both conventional econometric and Machine Learning (ML) models that incorporate the local spread dynamics, COVID-19 cases and death, and Google search activities to assess if incorporating information about local spreads improves the predictive accuracy of models for the US stock market. The results suggest that COVID-19 cases and deaths, its local spread, and Google searches have impacts on abnormal stock prices between January 2020 to May 2020. Furthermore, incorporating information about local spread significantly improves the performance of forecasting models of the abnormal stock prices at longer forecasting horizons.

我们开发了一种新颖的时间复杂网络方法来量化美国县级层面的新冠疫情传播动态。我们使用了传统计量经济学模型和机器学习(ML)模型,这些模型纳入了本地传播动态、新冠病例和死亡数据以及谷歌搜索活动,以评估纳入有关本地传播的信息是否能提高美国股票市场模型的预测准确性。结果表明,2020年1月至2020年5月期间,新冠病例和死亡、其本地传播以及谷歌搜索对异常股价有影响。此外,纳入有关本地传播的信息显著提高了较长预测期内异常股价预测模型的性能。