Fifth Department of Medicine, University Hospital Mannheim, Heidelberg University, Mannheim, Germany.

TUM School of Management, Technical University of Munich, Munich, Germany.

Ther Innov Regul Sci. 2022 Mar;56(2):313-322. doi: 10.1007/s43441-021-00364-y. Epub 2022 Jan 11.

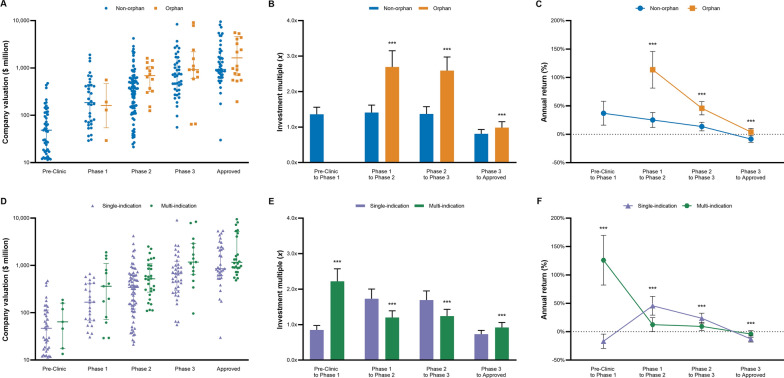

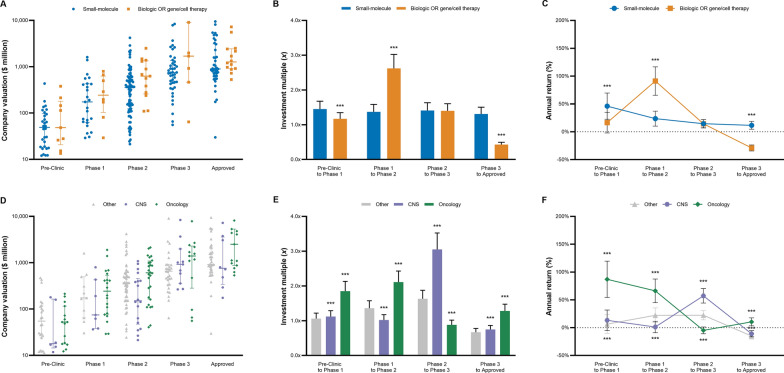

This study evaluates the association of Biopharma company valuation with the lead drug's development stage, orphan status, number of indications, and disease area. We also estimated annual returns Bioentrepreneurs and investors can expect from founding and investing in drug development ventures.

SDC Thomson Reuter and S&P Capital IQ were screened for majority acquisitions of US and EU Biopharma companies developing new molecular entities for prescription use (SIC code: 2834). Acquisition data were complemented with drug characteristics extracted from clinicaltrials.gov, the US Food and Drug Administration (FDA), and deal announcements. Thereafter, company valuations were combined with previously published clinical development periods alongside orphan-, indication-, and disease-specific success rates to estimate annual returns for investments in drug developing companies.

Based on a sample of 311 Biopharma acquisitions from 2005 to 2020, companies developing orphan, multi-indication, and oncology drugs were valued significantly higher than their peers during later development stages (p < 0.05). We also estimated significantly higher returns for shareholders of companies with orphan relative to non-orphan-designated lead drugs from Phase 1 to FDA approval (46% vs. 12%, p < 0.001). Drugs developed across multiple indications also provided higher returns than single-indication agents from Pre-Clinic to FDA approval (21% vs. 11%, p < 0.001). Returns for oncology drugs exceeded other disease areas (26% vs. 8%, p < 0.001).

Clinical and economic conditions surrounding orphan-designated drugs translate to a favorable financial risk-return profile for Bioentrepreneurs and investors. Bioentrepreneurs must be aware of the upside real option value their multi-indication drug could offer when negotiating acquisition or licensing agreements.

本研究评估了 Biopharma 公司估值与先导药物的开发阶段、孤儿状态、适应证数量和疾病领域之间的关系。我们还估算了生物企业家和投资者从成立和投资药物开发企业中可以获得的年度回报。

SDC Thomson Reuter 和 S&P Capital IQ 筛选了用于处方用途的新型分子实体的美国和欧盟 Biopharma 公司(SIC 代码:2834)的多数收购。通过临床试验、美国食品和药物管理局(FDA)和交易公告,从临床trials.gov 中提取药物特征来补充收购数据。此后,将公司估值与之前公布的临床开发阶段以及孤儿、适应证和疾病特定成功率结合起来,估算投资药物开发公司的年度回报。

基于 2005 年至 2020 年的 311 项 Biopharma 收购的样本,在后期开发阶段,开发孤儿药、多适应证药和肿瘤药物的公司的估值明显高于同行(p<0.05)。我们还估计,从第 1 阶段到 FDA 批准,孤儿药与非孤儿指定主导药物相比,股东的回报率明显更高(46%比 12%,p<0.001)。多适应证药物从临床前到 FDA 批准的回报率也高于单适应证药物(21%比 11%,p<0.001)。肿瘤药物的回报率超过了其他疾病领域(26%比 8%,p<0.001)。

围绕孤儿药指定的临床和经济条件为生物企业家和投资者带来了有利的财务风险回报。生物企业家在谈判收购或许可协议时,必须意识到其多适应证药物可能带来的上行真实期权价值。