Department of Mechanical, Aerospace and Civil Engineering, University of Manchester, Manchester, UK.

Centre for Crisis Studies and Mitigation, University of Manchester, Manchester, UK.

Sci Rep. 2022 Jun 13;12(1):9729. doi: 10.1038/s41598-022-13588-1.

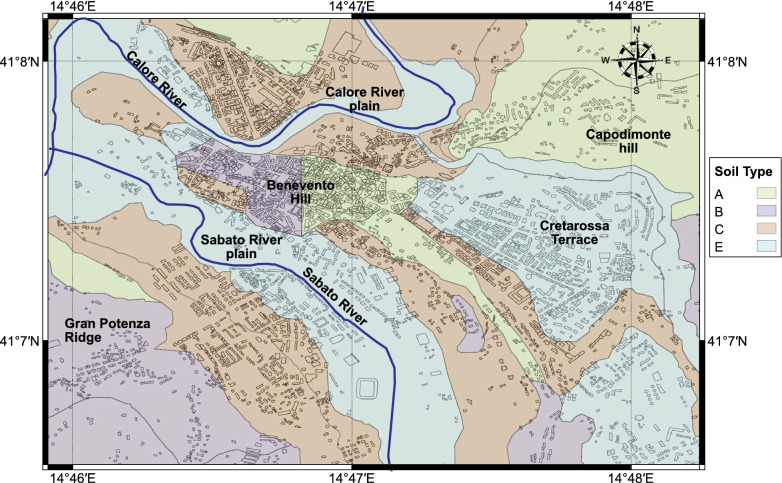

Catastrophe risk-based bonds are used by governments, financial institutions and (re)insurers to transfer the financial risk associated to the occurrence of catastrophic events, such as earthquakes, to the capital market. In this study, we show how municipalities prone to earthquakes can use this type of insurance-linked security to protect their building stock and communities from economic losses, and ultimately increase their earthquake resilience. We consider Benevento, a middle-sized historical town in southern Italy, as a case study, although the same approach is applicable to other urban areas in seismically active regions. One of the crucial steps in pricing catastrophe bonds is the computation of aggregate losses. We compute direct economic losses for each exposed asset based on high spatial resolution hazard and exposure models. Finally, we use the simulated loss data to price two types of catastrophe bonds (zero-coupon and coupon bonds) for different thresholds and maturity times. Although the present application focuses on earthquakes, the framework can potentially be applied to other natural disasters, such as hurricanes, floods, and other extreme weather events.

巨灾风险债券被政府、金融机构和(再)保险公司用于将与地震等巨灾事件相关的金融风险转移到资本市场。在本研究中,我们展示了易受地震影响的城市如何利用这种保险关联证券来保护其建筑存量和社区免受经济损失,并最终提高其抵御地震的能力。我们以意大利南部的一个中等历史城镇贝内文托(Benevento)为例进行研究,但同样的方法适用于地震活跃地区的其他城市地区。为巨灾债券定价的关键步骤之一是计算总损失。我们根据高空间分辨率的灾害和暴露模型,为每个暴露资产计算直接经济损失。最后,我们使用模拟的损失数据为不同阈值和到期时间的两种类型的巨灾债券(零息债券和附息债券)定价。尽管本应用侧重于地震,但该框架有可能应用于其他自然灾害,如飓风、洪水和其他极端天气事件。