Augustin Patrick, Sokolovski Valeri, Subrahmanyam Marti G, Tomio Davide

Desautels Faculty of Management, McGill University & Canadian Derivatives Institute, 1001 Sherbrooke Street West, Montréal QC H3A 1G5, Canada.

HEC Montréal; 3000 Chemin de la Côte-Sainte-Catherine, Montréal QC H3T 2A7, Canada.

J financ econ. 2022 Mar;143(3):1251-1274. doi: 10.1016/j.jfineco.2021.05.009. Epub 2021 May 11.

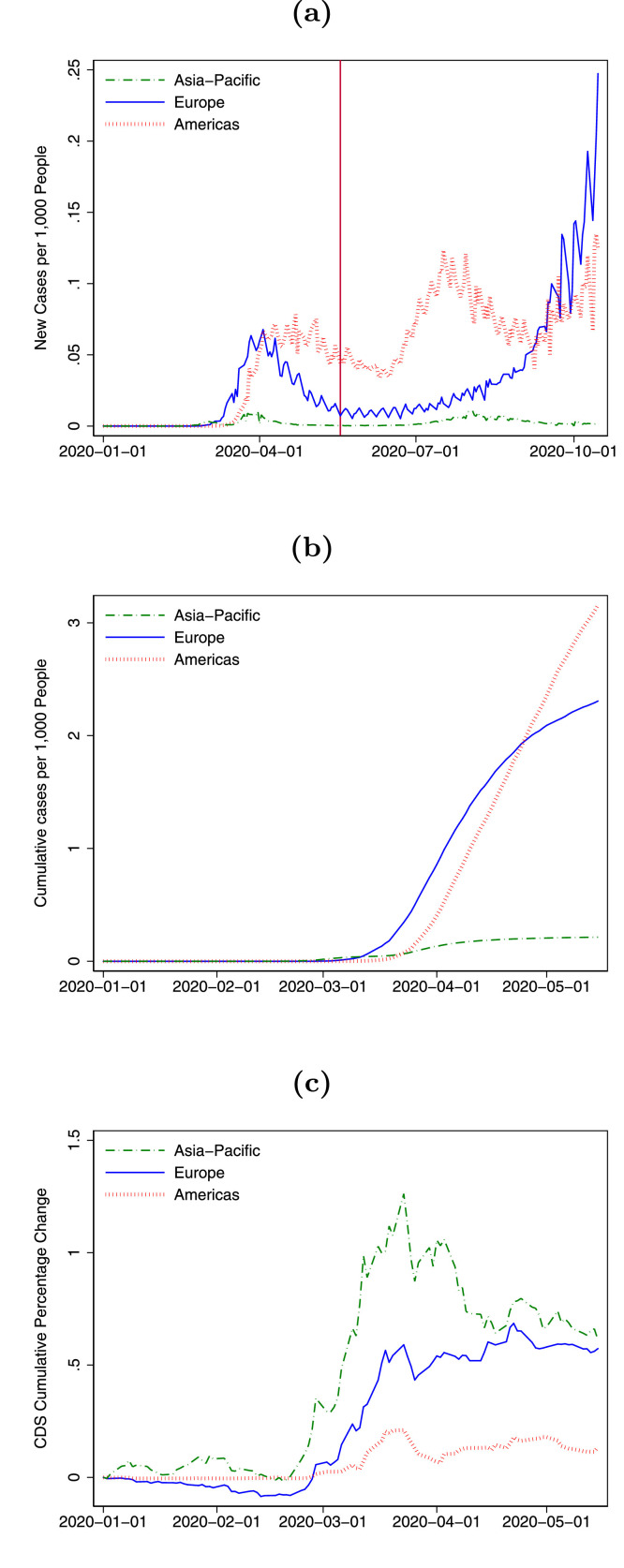

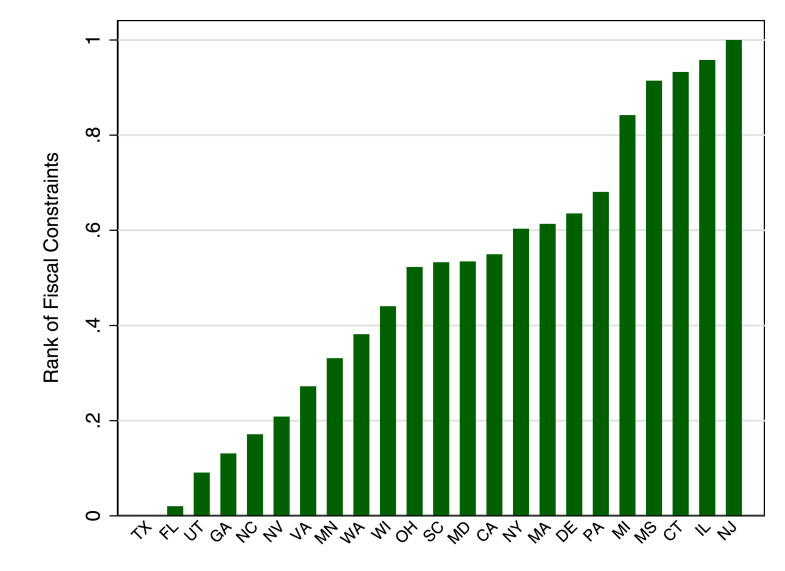

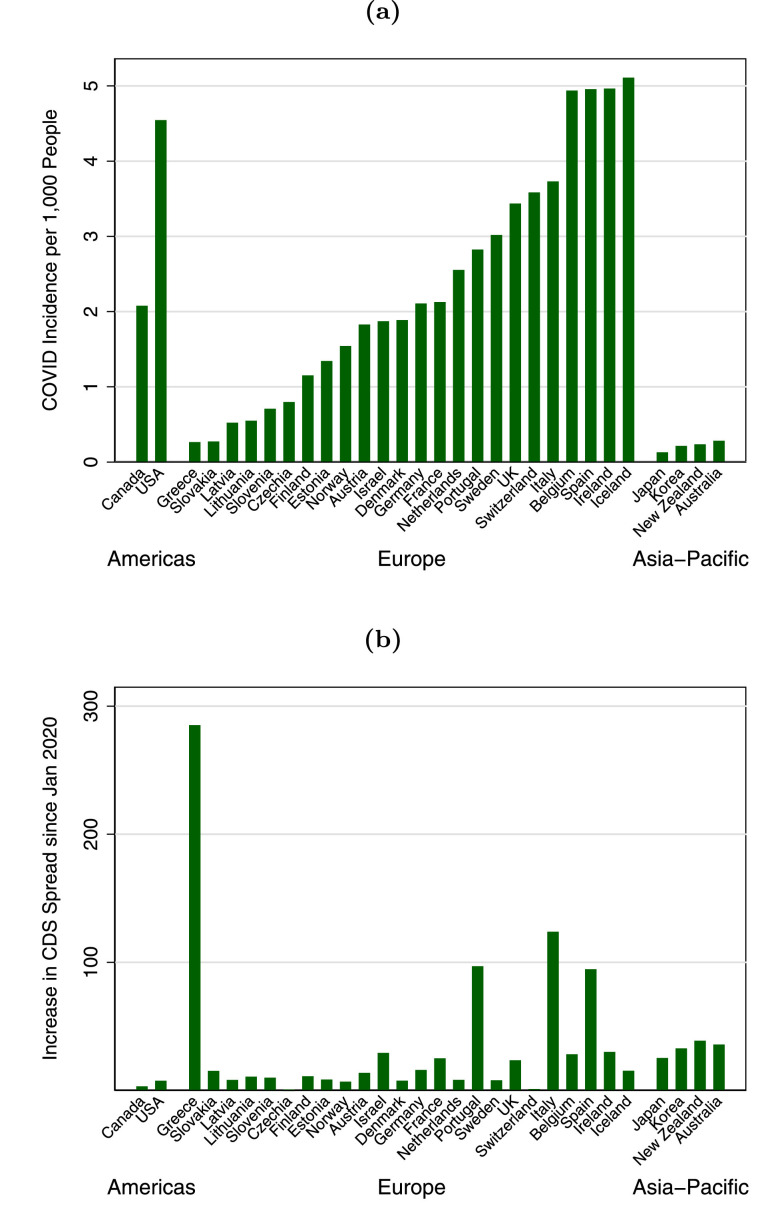

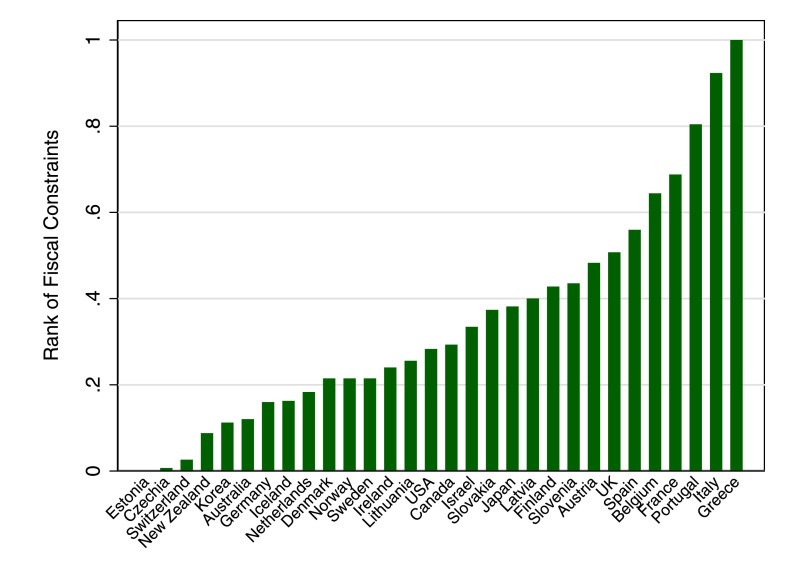

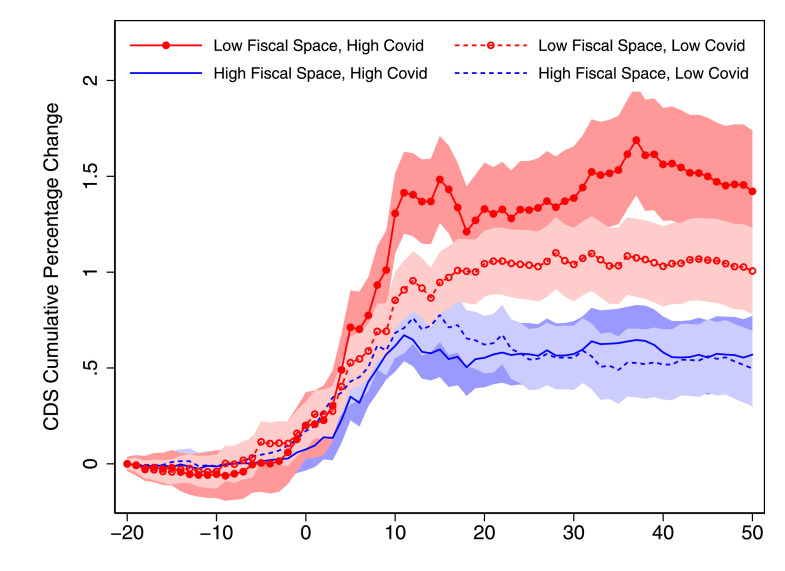

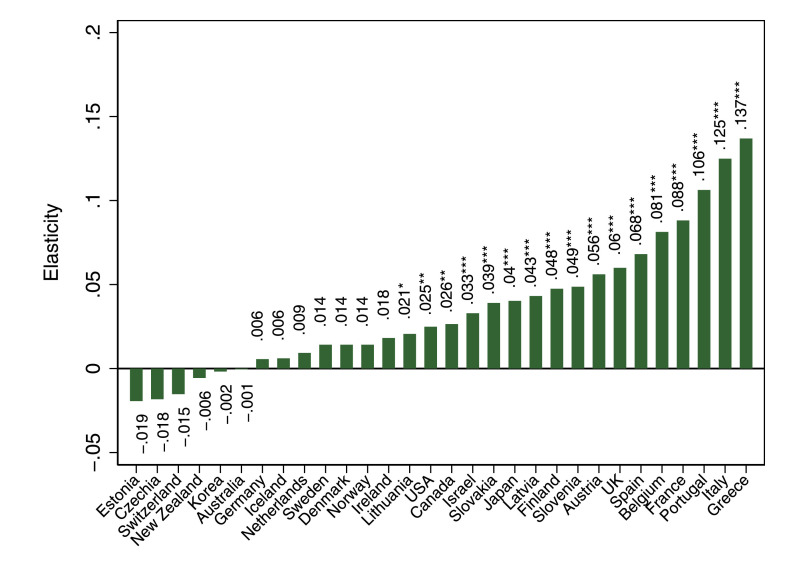

The COVID-19 pandemic provides a unique setting in which to evaluate the importance of a country's fiscal capacity in explaining the relation between economic growth shocks and sovereign default risk. For a sample of 30 developed countries, we find a positive and significant sensitivity of sovereign default risk to the intensity of the virus's spread for fiscally constrained governments. Supporting the fiscal channel, we confirm the results for Eurozone countries and U.S. states, for which monetary policy can be held constant. Our analysis suggests that financial markets penalize sovereigns with low fiscal space, impairing their resilience to external shocks.

新冠疫情提供了一个独特的背景,可用于评估一个国家的财政能力在解释经济增长冲击与主权违约风险之间关系时的重要性。对于30个发达国家的样本,我们发现,对于财政受限的政府而言,主权违约风险对病毒传播强度具有正向且显著的敏感性。为支持财政渠道,我们证实了欧元区国家和美国各州的结果,因为这些地区的货币政策可以保持不变。我们的分析表明,金融市场会惩罚财政空间狭小的主权国家,削弱其抵御外部冲击的能力。