Ben Ameur Hachmi, Boubaker Sahbi, Ftiti Zied, Louhichi Wael, Tissaoui Kais

INSEEC Grande Ecole, Omnes Education, Paris, France.

Department of Computer and Network Engineering, College of Computer Science and Engineering, University of Jeddah, Jeddah, 21959 Saudi Arabia.

Ann Oper Res. 2023 Jan 20:1-19. doi: 10.1007/s10479-022-05076-6.

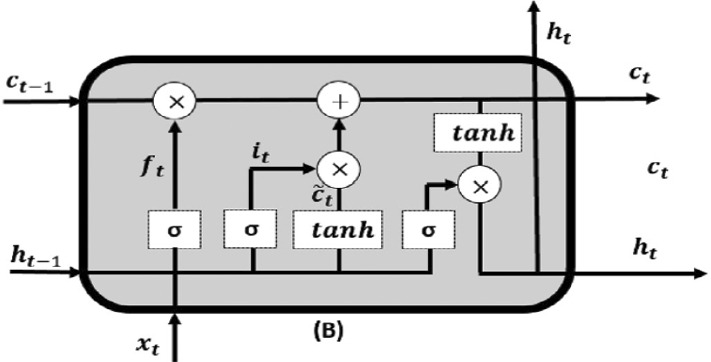

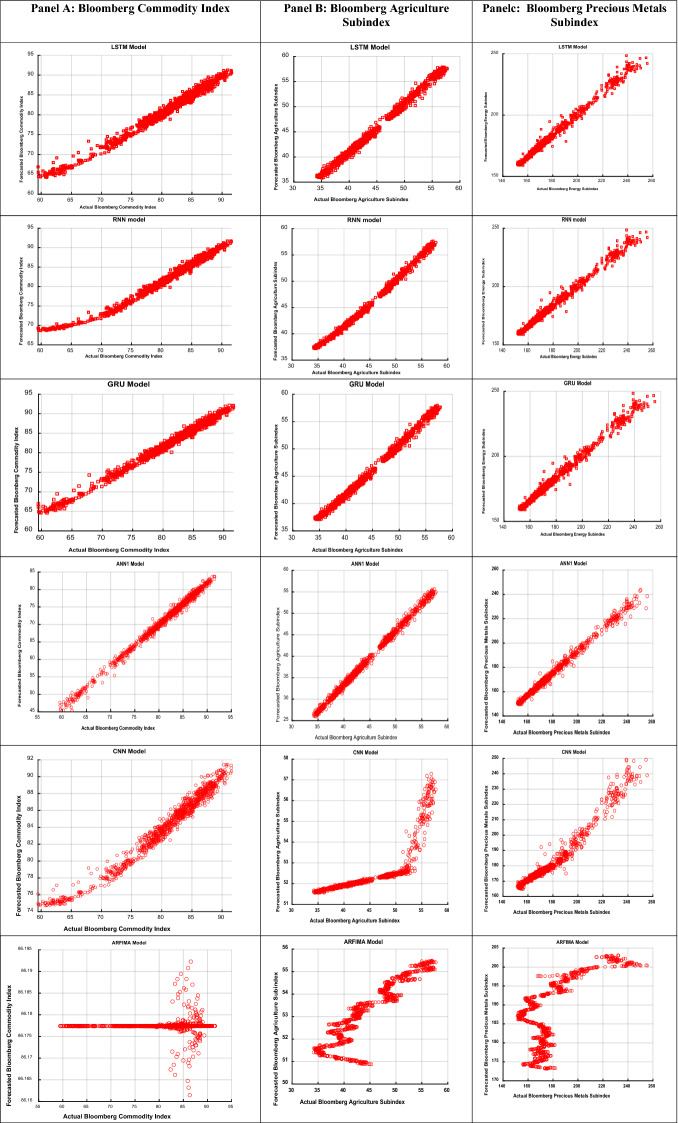

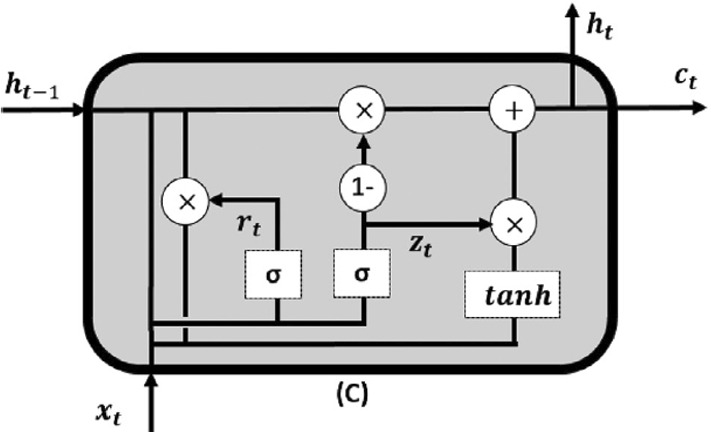

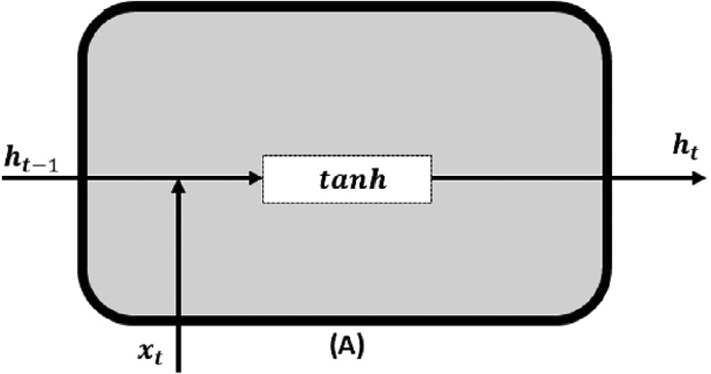

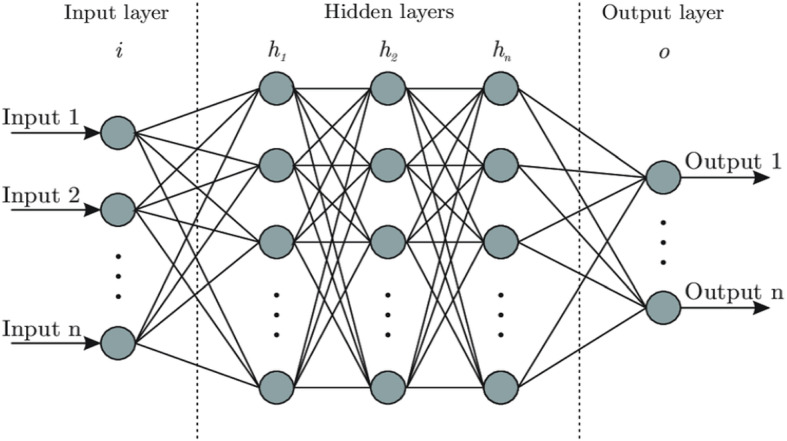

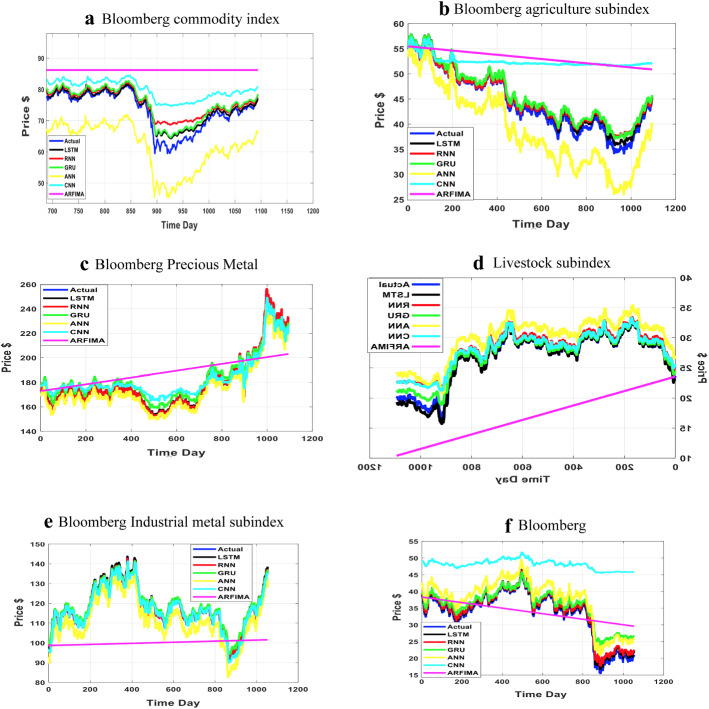

Since the last two decades, financial markets have exhibited several transformations owing to recurring crises episodes that has led to the development of alternative assets. Particularly, the commodity market has attracted attention from investors and hedgers. However, the operational research stream has also developed substantially based on the growth of the artificial intelligence field, which includes machine learning and deep learning. The choice of algorithms in both machine learning and deep learning is case-sensitive. Hence, AI practitioners should first attempt solutions related to machine learning algorithms, and if such solutions are unsatisfactory, they must apply deep learning algorithms. Using this perspective, this study aims to investigate the potential of various deep learning basic algorithms for forecasting selected commodity prices. Formally, we use the Bloomberg Commodity Index (noted by the Global Aggregate Index) and its five component indices: Bloomberg Agriculture Subindex, Bloomberg Precious Metals Subindex, Bloomberg Livestock Subindex, Bloomberg Industrial Metals Subindex, and Bloomberg Energy Subindex. Based on daily data from January 2002 (the beginning wave of commodity markets' financialization) to December 2020, results show the effectiveness of the Long Short-Term Memory method as a forecasting tool and the superiority of the Bloomberg Livestock Subindex and Bloomberg Industrial Metals Subindex for assessing other commodities' indices. These findings is important in term for investors in term of risk management as well as policymakers in adjusting public policy, especially during Russian-Ukrainian war.

在过去二十年中,由于反复出现的危机事件,金融市场发生了几次变革,这导致了另类资产的发展。特别是,商品市场吸引了投资者和套期保值者的关注。然而,运筹学领域也随着人工智能领域的发展而有了显著进步,人工智能领域包括机器学习和深度学习。机器学习和深度学习中算法的选择是视情况而定的。因此,人工智能从业者应首先尝试与机器学习算法相关的解决方案,如果这些解决方案不能令人满意,就必须应用深度学习算法。从这个角度出发,本研究旨在探讨各种深度学习基本算法在预测选定商品价格方面的潜力。具体而言,我们使用彭博商品指数(以全球综合指数表示)及其五个成分指数:彭博农业子指数、彭博贵金属子指数、彭博畜牧子指数、彭博工业金属子指数和彭博能源子指数。基于2002年1月(商品市场金融化的起始阶段)至2020年12月的每日数据,结果表明长短期记忆方法作为一种预测工具的有效性,以及彭博畜牧子指数和彭博工业金属子指数在评估其他商品指数方面的优越性。这些发现对于投资者进行风险管理以及政策制定者调整公共政策都具有重要意义,尤其是在俄乌战争期间。