Navarro Maricar M, Young Michael Nayat, Prasetyo Yogi Tri, Taylar Jonathan V

School of Industrial Engineering and Engineering Management, Mapúa University, 658 Muralla St., Intramuros, Manila 1002, Philippines.

School of Graduate Studies, Mapúa University, 658 Muralla St., Intramuros, Manila 1002, Philippines.

Heliyon. 2023 Jul;9(7):e17577. doi: 10.1016/j.heliyon.2023.e17577. Epub 2023 Jun 22.

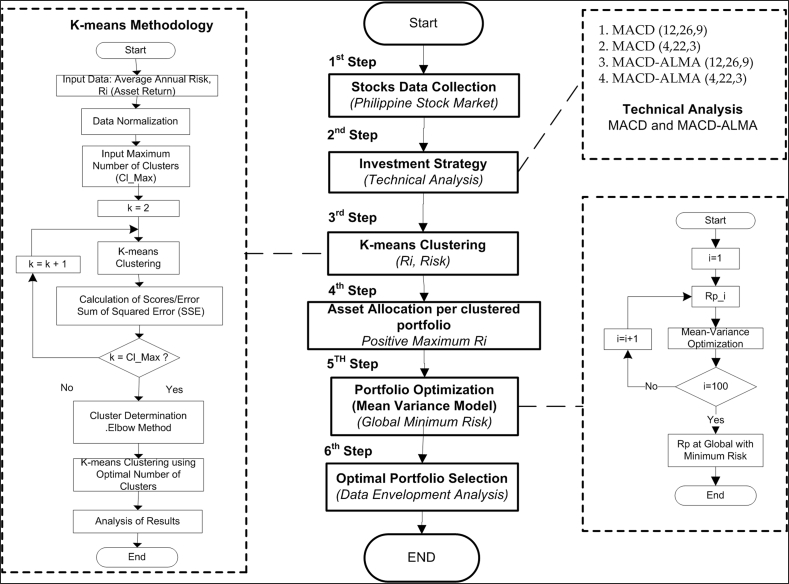

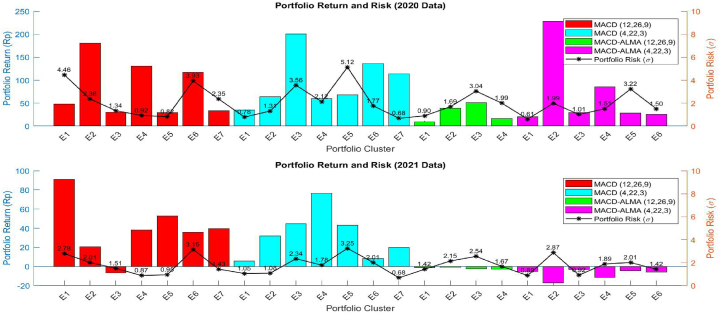

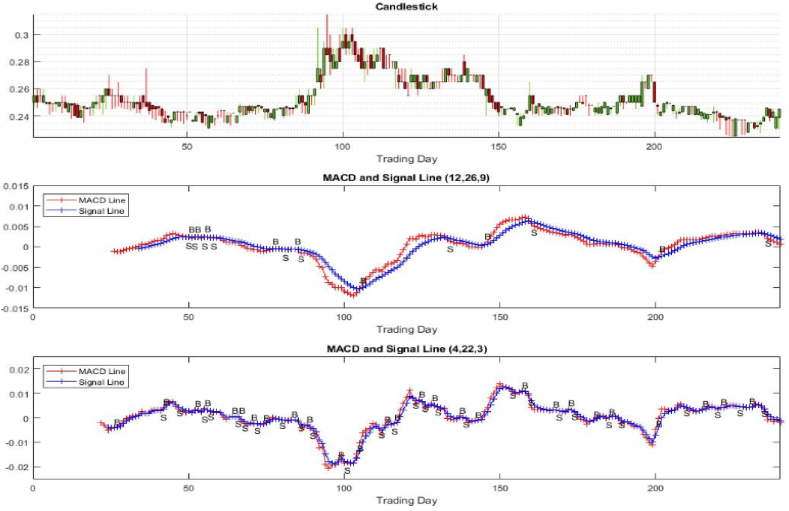

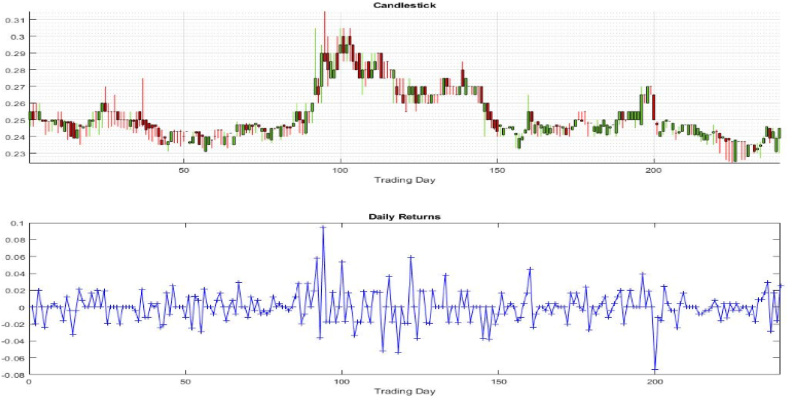

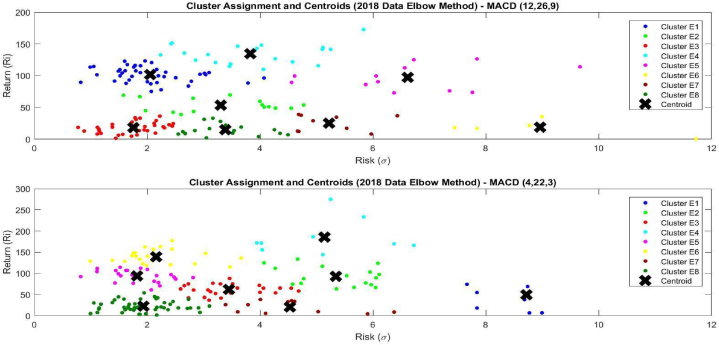

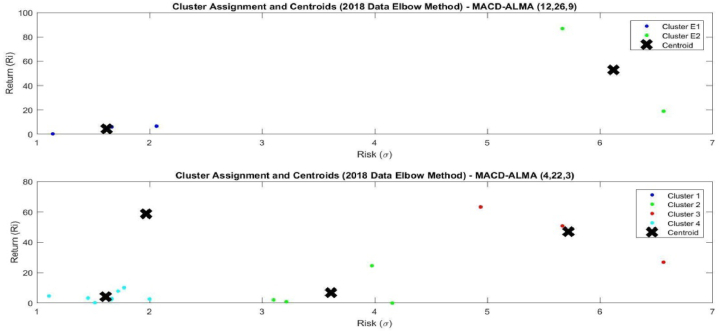

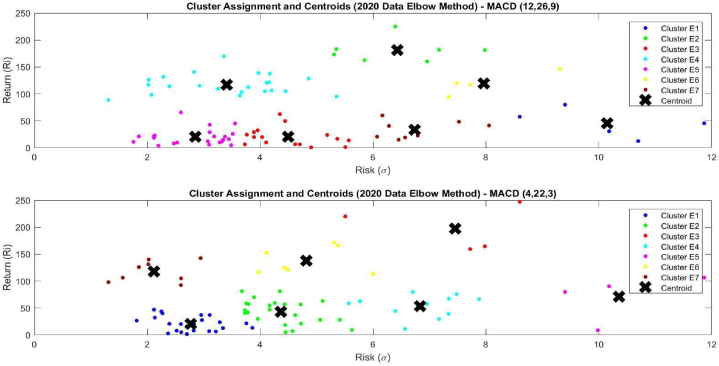

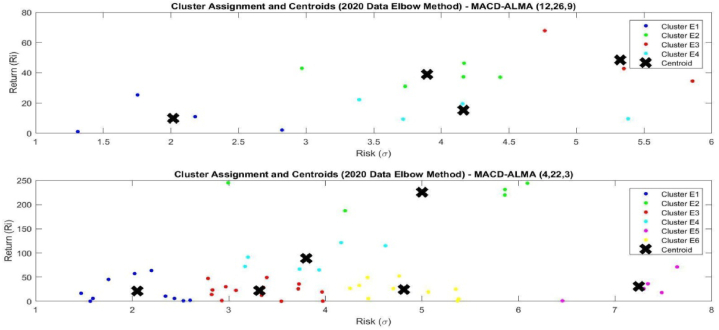

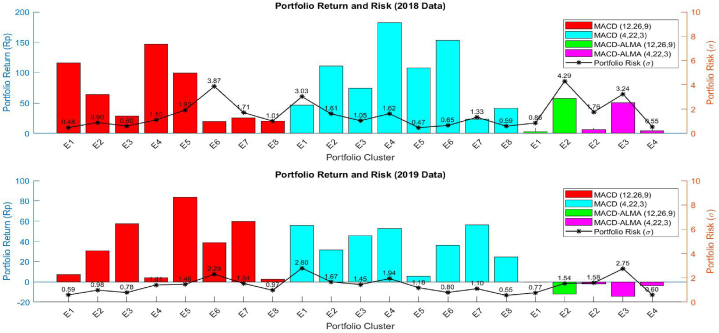

The Philippine stock market, just like most of its neighbors in the region, was seriously impacted by the global pandemic COVID-19. Investors remain hopeful while continuing to seek great ones in the damaged market. This paper developed a methodology for portfolio selection and optimization with the use of technical analysis, machine learning techniques, and portfolio optimization model. The combined methods of technical analysis, K-means clustering algorithm, and mean-variance portfolio optimization model will result in the development of the proposed TAKMV method. The study aims to integrate these three important analyses to identify portfolio investments. This paper uses the average annual risk and annual rate of return data for the years 2018 and 2020 to form the clusters and assessed the stocks that correspond to the investor's technical strategy such as Moving Average Convergence/Divergence (MACD) and Hybrid MACD with Arnaud Legoux Moving Average (ALMA). This paper solved the risk minimization problem on selected shares of the companies, based on the mean-variance portfolio optimization model. There are 230 and 239 companies for 2018 and 2020, respectively, listed in Philippine Stock Market, and all simulations were performed in MATLAB environment platform. Results showed that MACD strategy dominates the MACD-ALMA strategy in terms of the number of assets with a positive annual rate of return. The MACD works efficiently in the pre-COVID-19 condition while MACD-ALMA works efficiently during-COVID-19 condition, regardless of the number of assets with a positive annual rate of return. The results also show that the maximum expected portfolio return () can be achieved using the MACD and MACD-ALMA in the pre-and during-COVID-19 conditions, respectively. The MACD-ALMA shows an advantage during high-risk market conditions and can also provide maximum . The performance of the TAKMV method was validated by applying its results and comparing it to the next year's historical price. The 2018 results were compared to 2019 data and the 2020 results were compared to 2021 data. For consistency, the comparison was applied to the same company per portfolio. Simulation results show that the MACD strategy is more effective compared to MACD-ALMA.

与该地区的大多数邻国一样,菲律宾股市受到全球新冠疫情的严重冲击。投资者在受损的市场中仍满怀希望,同时继续寻找优质投资标的。本文运用技术分析、机器学习技术和投资组合优化模型,开发了一种投资组合选择与优化方法。将技术分析、K均值聚类算法和均值-方差投资组合优化模型相结合的方法,将产生本文所提出的TAKMV方法。该研究旨在整合这三种重要分析方法以识别投资组合。本文使用2018年和2020年的年均风险和年回报率数据来形成聚类,并评估与投资者技术策略相对应的股票,如移动平均收敛/发散指标(MACD)以及结合了阿诺德·勒古克斯移动平均线(ALMA)的混合MACD指标。本文基于均值-方差投资组合优化模型,解决了所选公司股票的风险最小化问题。菲律宾证券市场在2018年和2020年分别有230家和239家公司上市,所有模拟均在MATLAB环境平台上进行。结果表明,就年回报率为正的资产数量而言,MACD策略优于MACD-ALMA策略。无论年回报率为正的资产数量如何,MACD在新冠疫情前的情况下有效运作而MACD-ALMA在新冠疫情期间有效运作;结果还表明,在新冠疫情前和疫情期间分别使用MACD和MACD-ALMA可以实现最大预期投资组合回报()。MACD-ALMA在高风险市场条件下显示出优势,并且也能提供最大回报。通过应用TAKMV方法的结果并将其与下一年的历史价格进行比较,验证了该方法的性能。将2018年的结果与2019年的数据进行比较,将2020年的结果与2021年的数据进行比较。为保持一致性,每个投资组合的比较都应用于同一家公司。模拟结果表明,MACD策略比MACD-ALMA更有效。