School of Accountancy, Henan Institute of Economics and Trade, Zhengzhou, Henan, China.

PLoS One. 2023 Nov 14;18(11):e0294466. doi: 10.1371/journal.pone.0294466. eCollection 2023.

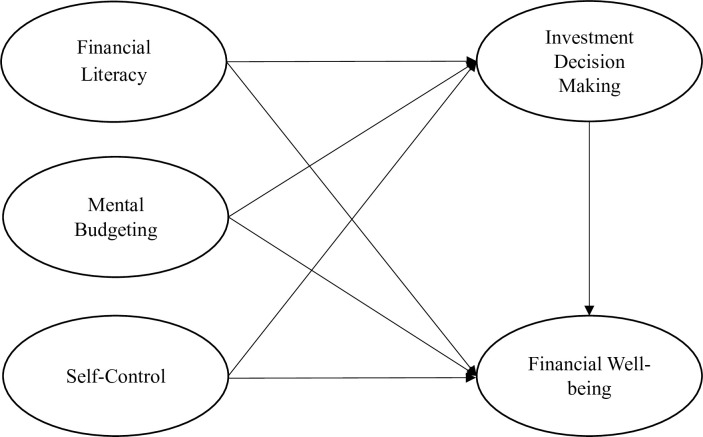

The topic of financial wellbeing is a current concern within the realm of personal and household finance. This study aims to examine the influence of cognitive factors, specifically financial literacy, mental budgeting, and self-control, on subjective financial wellbeing. While there exist multiple determinants of financial wellbeing, this research focuses on these particular cognitive factors. The present study aims to examine the mediating role of investment decision-making behavior in the association between cognitive factors and financial well-being. The study employed Partial Least Squares Structural Equation Modeling (PLS-SEM) to analyze the data collected from a sample of 449 Chinese university students, with the aim of assessing the empirical associations. The results indicate that financial literacy, mental budgeting, and self-control exert a favorable and noteworthy influence on an individual's financial well-being. The results indicate that individuals with a greater degree of financial literacy are more prone to achieving superior financial well-being. Moreover, individuals who practice mental budgeting, a technique that entails mentally classifying and monitoring their expenditures, demonstrate elevated levels of financial well-being. Likewise, the exercise of self-regulation is identified as a pivotal element that impacts an individual's financial wellbeing. The findings indicate that there is evidence to support the mediator, investment decision-making behavior. This mediator partially mediates the association between the independent variables, namely financial literacy, mental budgeting, and self-control, and financial well-being. The results suggest that individuals with elevated levels of financial literacy, proficient mental budgeting skills, and self-regulatory abilities are inclined towards demonstrating favorable investment decision-making conduct. Consequently, this contributes to their general financial welfare. In general, the study's theoretical implications augment the current knowledge repository, while its practical implications provide feasible perspectives for policymakers, financial institutions, and individuals to foster financial wellness and enhance financial results.

财务幸福感是个人和家庭财务领域当前关注的话题。本研究旨在探讨认知因素,特别是金融知识、心理预算和自我控制,对主观财务幸福感的影响。虽然财务幸福感有多种决定因素,但本研究侧重于这些特定的认知因素。本研究旨在探讨投资决策行为在认知因素与财务幸福感之间的关系中的中介作用。本研究采用偏最小二乘结构方程模型(PLS-SEM)分析了来自 449 名中国大学生样本的数据,旨在评估实证关联。结果表明,金融知识、心理预算和自我控制对个人的财务幸福感有积极显著的影响。结果表明,金融知识程度较高的个体更容易获得更好的财务幸福感。此外,实行心理预算的个体,即通过心理分类和监测支出来进行预算的个体,表现出更高的财务幸福感。同样,自我调节的运用被认为是影响个人财务幸福感的关键因素。研究结果表明,有证据支持中介变量,即投资决策行为。该中介变量部分中介了自变量,即金融知识、心理预算和自我控制与财务幸福感之间的关系。结果表明,金融知识水平较高、心理预算技能熟练、自我调节能力较强的个体倾向于表现出有利的投资决策行为。因此,这有助于他们的整体财务福利。总的来说,该研究的理论意义增加了当前的知识库,而其实际意义为政策制定者、金融机构和个人提供了可行的视角,以促进财务健康并提高财务成果。