Fabiani Gianluca, Evangelou Nikolaos, Cui Tianqi, Bello-Rivas Juan M, Martin-Linares Cristina P, Siettos Constantinos, Kevrekidis Ioannis G

Modelling Engineering Risk and Complexity, Scuola Superiore Meridionale, Naples, Italy.

Department of Chemical and Biomolecular Engineering, Johns Hopkins University, Baltimore, MD, USA.

Nat Commun. 2024 May 15;15(1):4117. doi: 10.1038/s41467-024-48024-7.

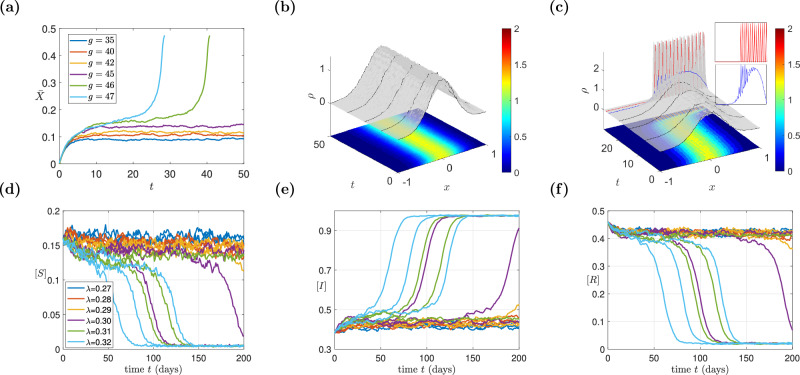

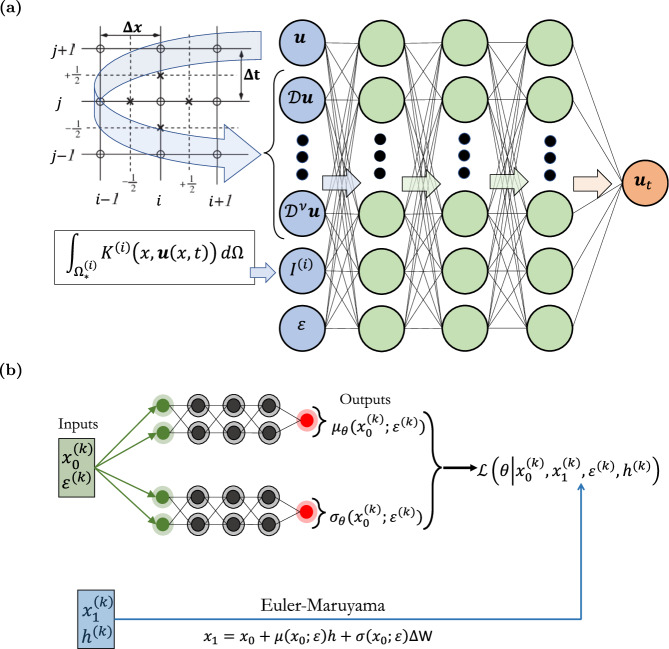

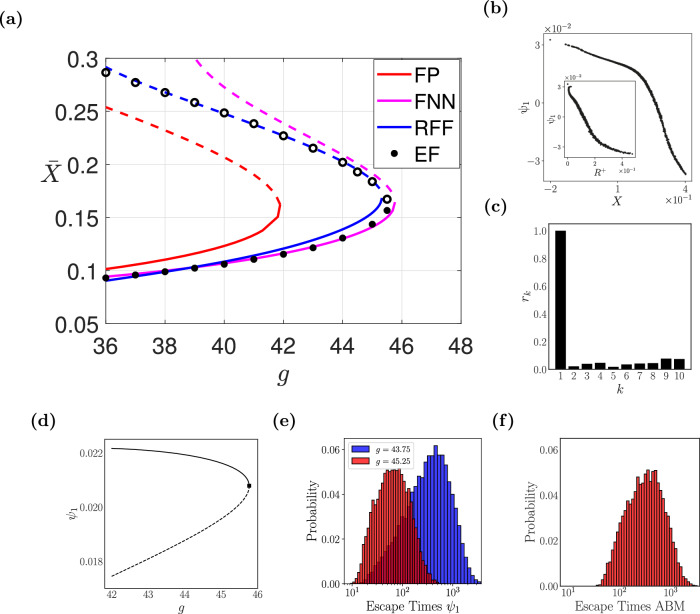

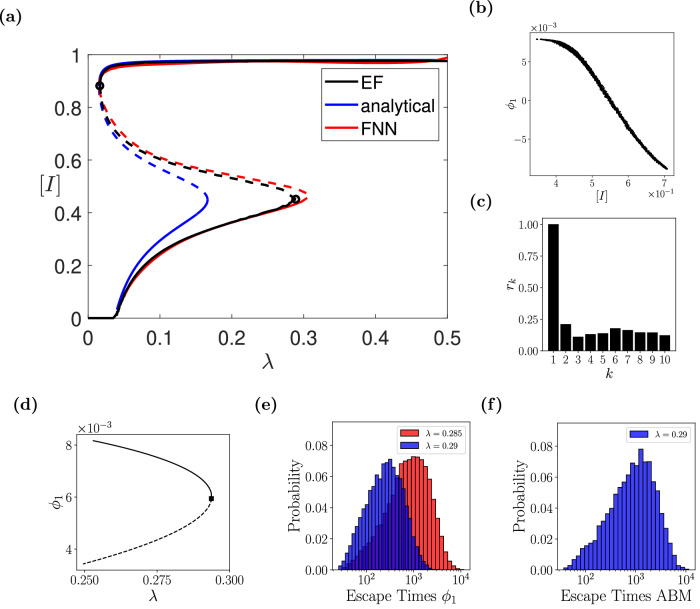

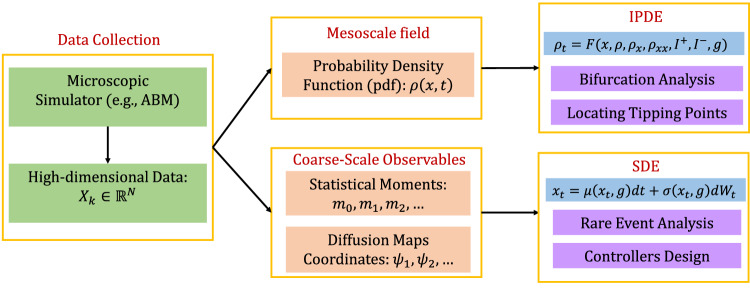

We present a machine learning framework bridging manifold learning, neural networks, Gaussian processes, and Equation-Free multiscale approach, for the construction of different types of effective reduced order models from detailed agent-based simulators and the systematic multiscale numerical analysis of their emergent dynamics. The specific tasks of interest here include the detection of tipping points, and the uncertainty quantification of rare events near them. Our illustrative examples are an event-driven, stochastic financial market model describing the mimetic behavior of traders, and a compartmental stochastic epidemic model on an Erdös-Rényi network. We contrast the pros and cons of the different types of surrogate models and the effort involved in learning them. Importantly, the proposed framework reveals that, around the tipping points, the emergent dynamics of both benchmark examples can be effectively described by a one-dimensional stochastic differential equation, thus revealing the intrinsic dimensionality of the normal form of the specific type of the tipping point. This allows a significant reduction in the computational cost of the tasks of interest.

我们提出了一个机器学习框架,它将流形学习、神经网络、高斯过程和无方程多尺度方法联系起来,用于从基于智能体的详细模拟器构建不同类型的有效降阶模型,并对其涌现动力学进行系统的多尺度数值分析。这里感兴趣的具体任务包括临界点的检测以及临界点附近罕见事件的不确定性量化。我们的示例是一个描述交易者模仿行为的事件驱动型随机金融市场模型,以及一个在厄多斯 - 雷尼网络上的 compartmental 随机流行病模型。我们对比了不同类型替代模型的优缺点以及学习它们所涉及的工作量。重要的是,所提出的框架表明,在临界点附近,两个基准示例的涌现动力学都可以由一维随机微分方程有效描述,从而揭示了特定类型临界点范式的内在维度。这使得感兴趣任务的计算成本大幅降低。