Fenwick Elisabeth, Marshall Deborah A, Levy Adrian R, Nichol Graham

Public Health and Health Policy, University of Glasgow, Glasgow, UK.

BMC Health Serv Res. 2006 Apr 19;6:52. doi: 10.1186/1472-6963-6-52.

The cost-effectiveness acceptability curve (CEAC) is a method for summarizing the uncertainty in estimates of cost-effectiveness. The CEAC, derived from the joint distribution of costs and effects, illustrates the (Bayesian) probability that the data are consistent with a true cost-effectiveness ratio falling below a specified ceiling ratio. The objective of the paper is to illustrate how to construct and interpret a CEAC.

A retrospective cost-effectiveness analysis of the Atrial Fibrillation Follow-up Investigation of Rhythm Management (AFFIRM) randomized controlled trial with 4060 patients followed for 3.5 years. The target population was patients with atrial fibrillation who were 65 years of age or had other risk factors for stroke or death similar to those enrolled in AFFIRM. The intervention involved the management of patients with atrial fibrillation with antiarrhythmic drugs (rhythm-control) compared with drugs that control heart rate (rate-control). Measurements of mean survival, mean costs and incremental cost-effectiveness were made. The uncertainty surrounding the estimates of cost-effectiveness was illustrated through a cost-effectiveness acceptability curve.

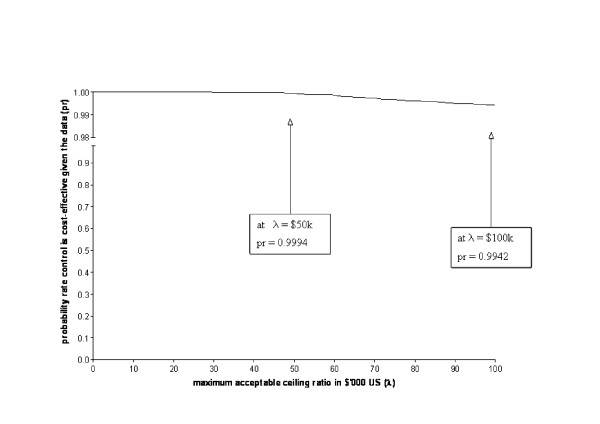

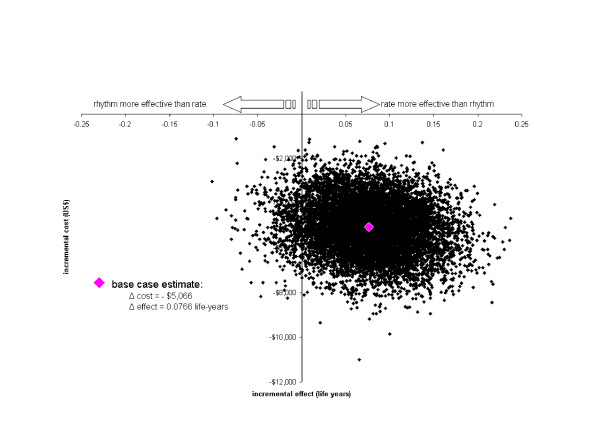

The base case point estimate for the difference in effects and costs between rate and rhythm-control is 0.08 years (95% CI: -0.1 years to 0.24 years) and -5,077 US dollars (95% CI: -1,100 dollars to -11,006 dollars). The CEAC shows that the decision uncertainty surrounding the adoption of rate-control strategies is less than 1.7% regardless of the maximum acceptable ceiling ratio. Thus, there is very little uncertainty surrounding the decision to adopt rate-control compared to rhythm-control for patients with atrial fibrillation from a resource point of view.

The CEAC is straightforward to calculate, construct and interpret. The CEAC is useful to a decision maker faced with the choice of whether or not to adopt a technology because it provides a measure of the decision uncertainty surrounding the choice.

成本效益可接受性曲线(CEAC)是一种用于总结成本效益估计中不确定性的方法。CEAC源自成本和效果的联合分布,它说明了数据与低于指定上限比率的真实成本效益比率相一致的(贝叶斯)概率。本文的目的是说明如何构建和解释CEAC。

对心房颤动节律管理随访调查(AFFIRM)随机对照试验进行回顾性成本效益分析,该试验纳入4060例患者,随访3.5年。目标人群为65岁或有其他与AFFIRM研究入组患者相似的中风或死亡风险因素的心房颤动患者。干预措施包括使用抗心律失常药物(节律控制)与控制心率的药物(心率控制)对心房颤动患者进行管理。测量平均生存期、平均成本和增量成本效益。通过成本效益可接受性曲线说明了成本效益估计周围的不确定性。

心率控制和节律控制在效果和成本差异方面的基础病例点估计值分别为0.08年(95%置信区间:-0.1年至0.24年)和-5077美元(95%置信区间:-1100美元至-11006美元)。CEAC显示,无论最大可接受上限比率如何,采用心率控制策略的决策不确定性均小于1.7%。因此,从资源角度来看,对于心房颤动患者,与节律控制相比,采用心率控制的决策几乎没有不确定性。

CEAC易于计算、构建和解释。CEAC对于面临是否采用某项技术选择的决策者很有用,因为它提供了围绕该选择的决策不确定性的一种度量。