Hartl Barbara, Hofmann Eva, Gangl Katharina, Hartner-Tiefenthaler Martina, Kirchler Erich

University of Vienna, Vienna, Austria.

Vienna University of Technology, Vienna, Austria.

PLoS One. 2015 Apr 29;10(4):e0123355. doi: 10.1371/journal.pone.0123355. eCollection 2015.

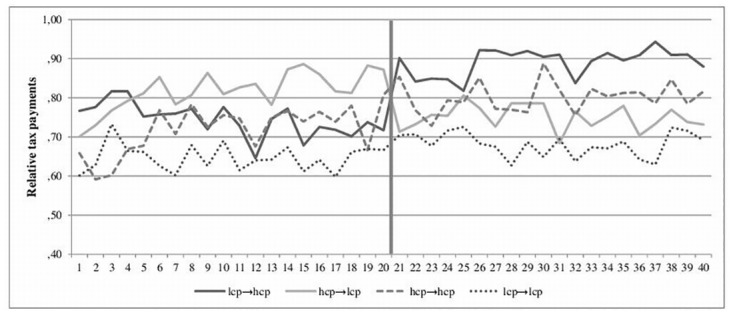

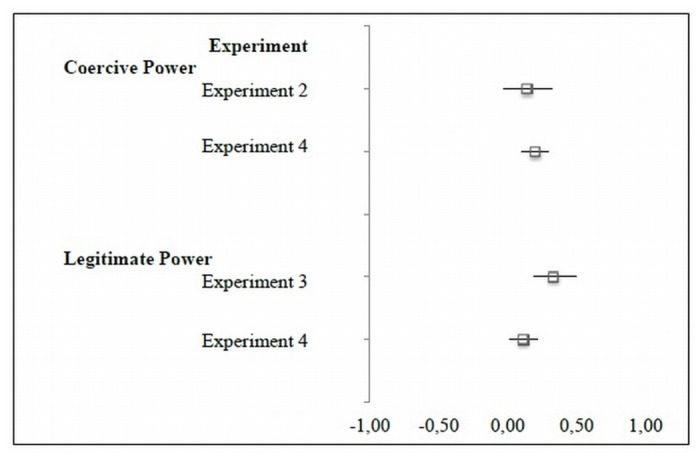

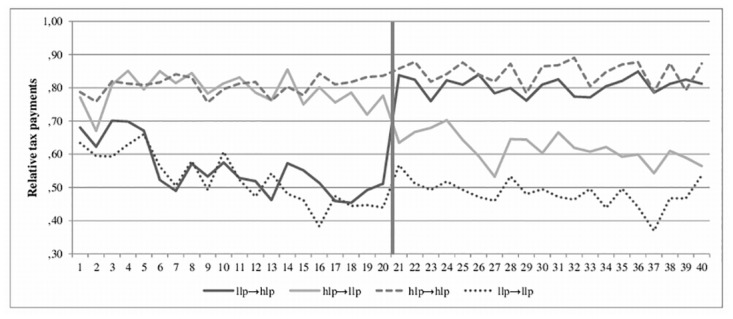

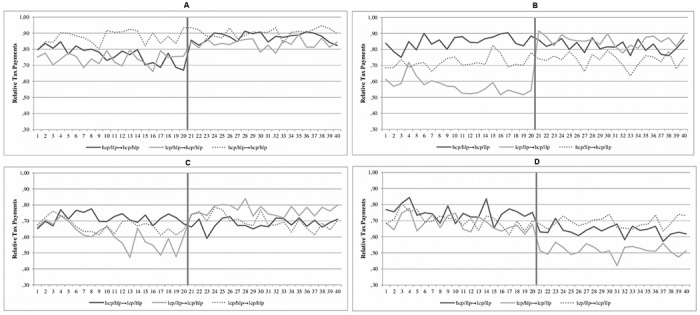

Following the classic economic model of tax evasion, taxpayers base their tax decisions on economic determinants, like fine rate and audit probability. Empirical findings on the relationship between economic key determinants and tax evasion are inconsistent and suggest that taxpayers may rather rely on their beliefs about tax authority's power. Descriptions of the tax authority's power may affect taxpayers' beliefs and as such tax evasion. Experiment 1 investigates the impact of fines and beliefs regarding tax authority's power on tax evasion. Experiments 2-4 are conducted to examine the effect of varying descriptions about a tax authority's power on participants' beliefs and respective tax evasion. It is investigated whether tax evasion is influenced by the description of an authority wielding coercive power (Experiment 2), legitimate power (Experiment 3), and coercive and legitimate power combined (Experiment 4). Further, it is examined whether a contrast of the description of power (low to high power; high to low power) impacts tax evasion (Experiments 2-4). Results show that the amount of fine does not impact tax payments, whereas participants' beliefs regarding tax authority's power significantly shape compliance decisions. Descriptions of high coercive power as well as high legitimate power affect beliefs about tax authority's power and positively impact tax honesty. This effect still holds if both qualities of power are applied simultaneously. The contrast of descriptions has little impact on tax evasion. The current study indicates that descriptions of the tax authority, e.g., in information brochures and media reports, have more influence on beliefs and tax payments than information on fine rates. Methodically, these considerations become particularly important when descriptions or vignettes are used besides objective information.

遵循经典的逃税经济模型,纳税人基于经济决定因素(如罚款率和审计概率)做出纳税决策。关于经济关键决定因素与逃税之间关系的实证研究结果并不一致,这表明纳税人可能更依赖于他们对税务机关权力的看法。对税务机关权力的描述可能会影响纳税人的看法,进而影响逃税行为。实验1研究了罚款以及对税务机关权力的看法对逃税的影响。进行实验2 - 4是为了检验对税务机关权力的不同描述对参与者看法及相应逃税行为的影响。研究了逃税是否受到对拥有强制权力(实验2)、合法权力(实验3)以及强制权力和合法权力相结合(实验4)的机关的描述的影响。此外,还研究了权力描述的对比(从低权力到高权力;从高权力到低权力)是否会影响逃税行为(实验2 - 4)。结果表明,罚款金额不会影响纳税情况,而参与者对税务机关权力的看法会显著影响纳税决策。对高强制权力以及高合法权力的描述会影响对税务机关权力的看法,并对纳税诚信产生积极影响。如果同时运用这两种权力特质,这种影响仍然成立。描述的对比对逃税行为影响不大。当前研究表明,税务机关的描述(例如在信息手册和媒体报道中)对看法和纳税情况的影响比罚款率信息更大。从方法上讲,当除了客观信息之外还使用描述或 vignettes 时,这些考虑因素就变得尤为重要。