Gangl Katharina, Pfabigan Daniela M, Lamm Claus, Kirchler Erich, Hofmann Eva

Department of Applied Psychology: Work, Education, Economy; Faculty of Psychology, University of Vienna, Vienna, Austria.

Economic and Social Psychology, Institute of Psychology, University of Goettingen, Goettingen, Germany.

Soc Cogn Affect Neurosci. 2017 Jul 1;12(7):1108-1117. doi: 10.1093/scan/nsx029.

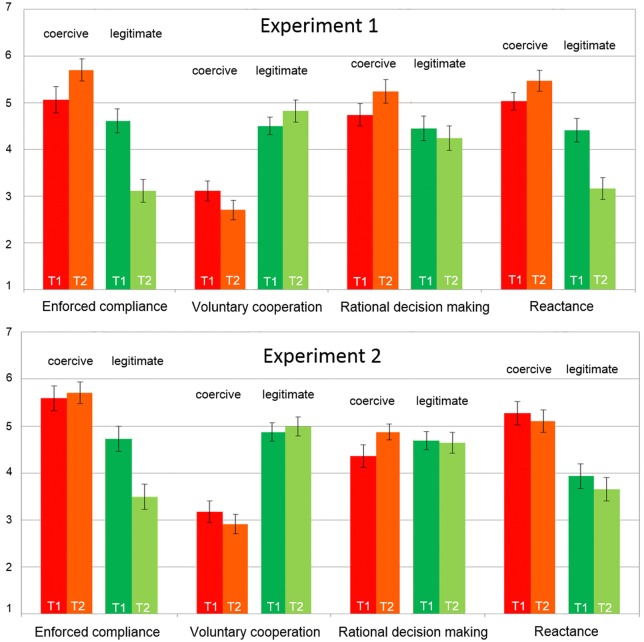

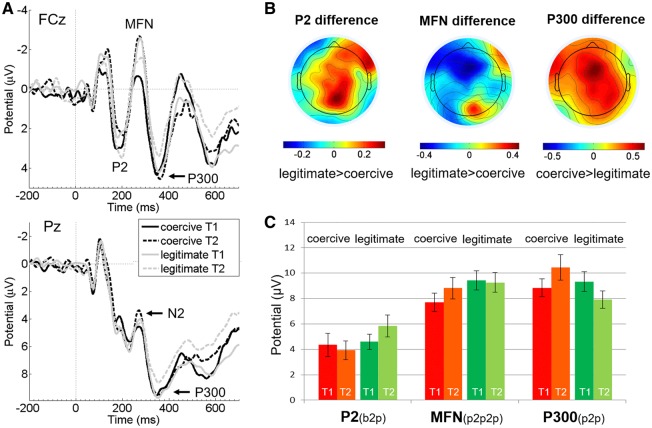

Cooperation in social systems such as tax honesty is of central importance in our modern societies. However, we know little about cognitive and neural processes driving decisions to evade or pay taxes. This study focuses on the impact of perceived tax authority and examines the mental chronometry mirrored in ERP data allowing a deeper understanding about why humans cooperate in tax systems. We experimentally manipulated coercive and legitimate authority and studied its impact on cooperation and underlying cognitive (experiment 1, 2) and neuronal (experiment 2) processes. Experiment 1 showed that in a condition of coercive authority, tax payments are lower, decisions are faster and participants report more rational reasoning and enforced compliance, however, less voluntary cooperation than in a condition of legitimate authority. Experiment 2 confirmed most results, but did not find a difference in payments or self-reported rational reasoning. Moreover, legitimate authority led to heightened cognitive control (expressed by increased MFN amplitudes) and disrupted attention processing (expressed by decreased P300 amplitudes) compared to coercive authority. To conclude, the neuronal data surprisingly revealed that legitimate authority may led to higher decision conflict and thus to higher cognitive demands in tax decisions than coercive authority.

在诸如税收诚信等社会体系中的合作,在我们现代社会中至关重要。然而,我们对驱动逃税或纳税决策的认知和神经过程知之甚少。本研究聚焦于感知到的税务机关的影响,并考察事件相关电位(ERP)数据中反映的心理时间测量,以便更深入地理解人类在税收体系中合作的原因。我们通过实验操纵了强制权威和合法权威,并研究了其对合作以及潜在认知(实验1、2)和神经(实验2)过程的影响。实验1表明,在强制权威条件下,纳税额更低,决策更快,参与者报告的理性推理和强制合规更多,但与合法权威条件相比,自愿合作更少。实验2证实了大部分结果,但未发现纳税额或自我报告的理性推理存在差异。此外,与强制权威相比,合法权威导致更高的认知控制(以增强的失匹配负波(MFN)振幅表示)和注意力处理中断(以降低的P300振幅表示)。总之,神经数据惊人地显示,与强制权威相比,合法权威可能导致更高的决策冲突,从而在税收决策中产生更高的认知需求。