Ouyang Fang-Yan, Zheng Bo, Jiang Xiong-Fei

Department of Physics, Zhejiang University, Hangzhou 310027, China; School of Electronics and Information, Zhejiang University of Media and Communications, Hangzhou 310018, China; Collaborative Innovation Center of Advanced Microstructures, Nanjing 210093, China.

Department of Physics, Zhejiang University, Hangzhou 310027, China; Collaborative Innovation Center of Advanced Microstructures, Nanjing 210093, China.

PLoS One. 2015 Oct 1;10(10):e0139420. doi: 10.1371/journal.pone.0139420. eCollection 2015.

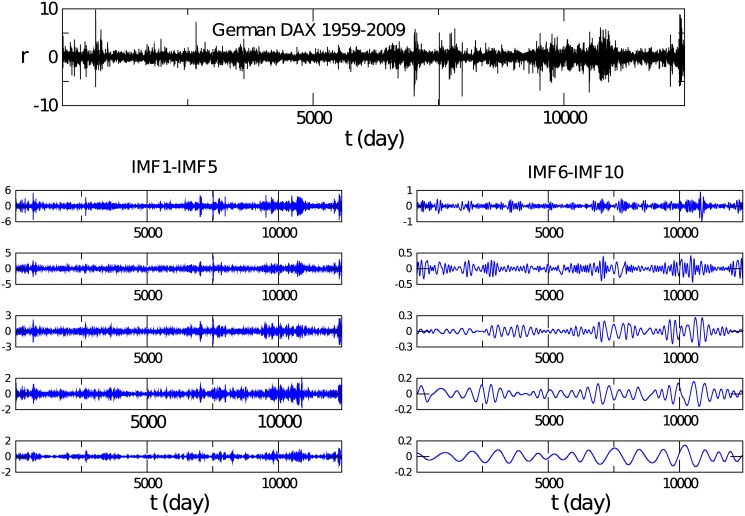

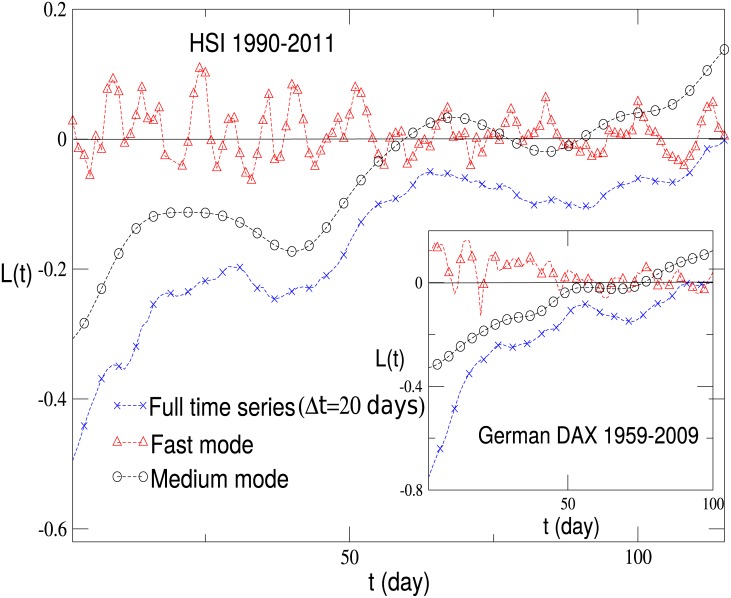

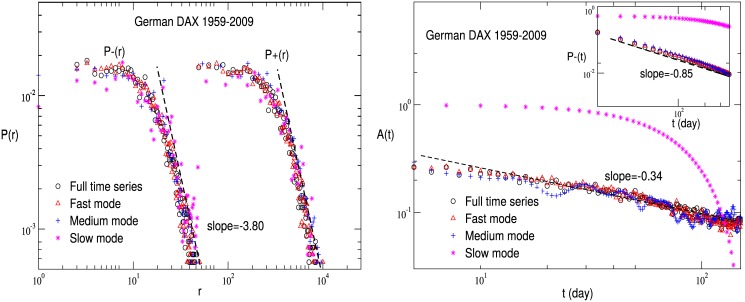

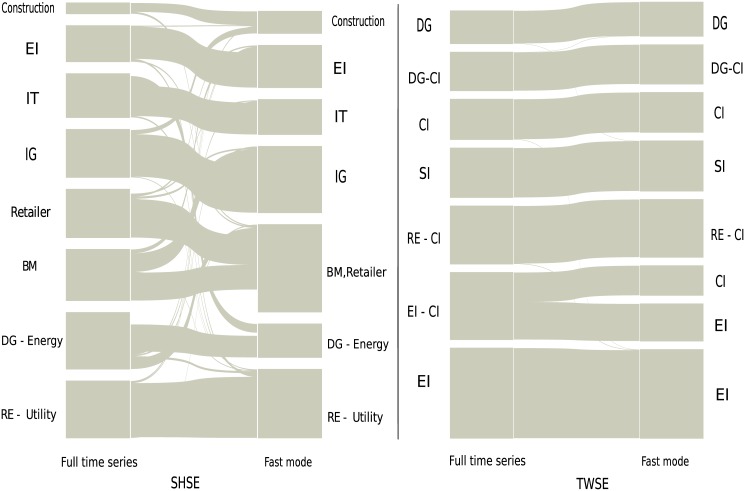

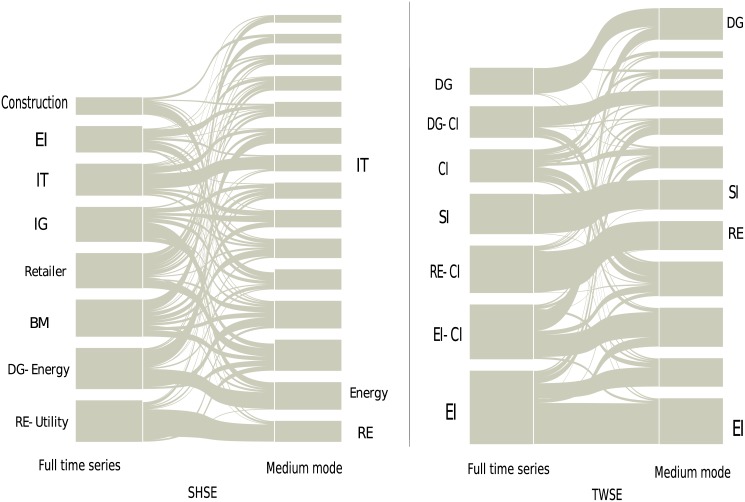

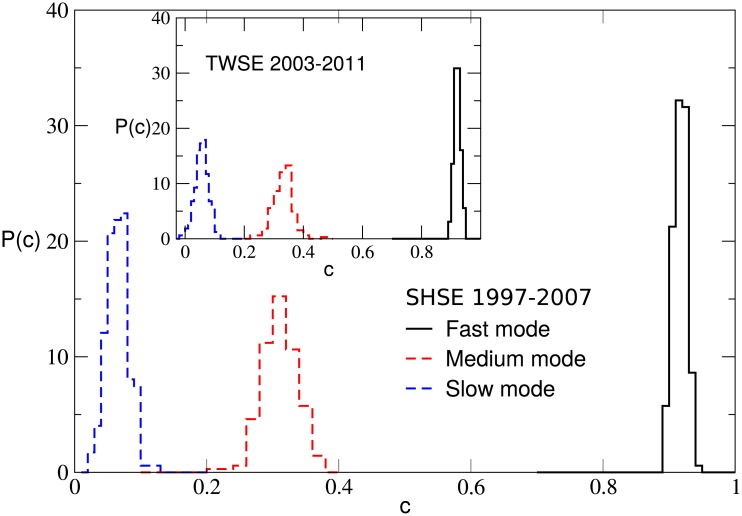

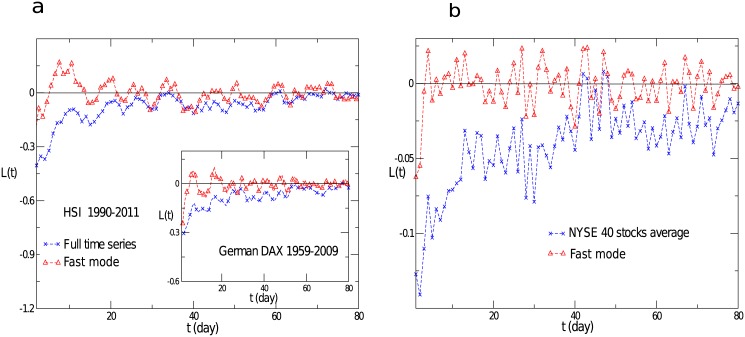

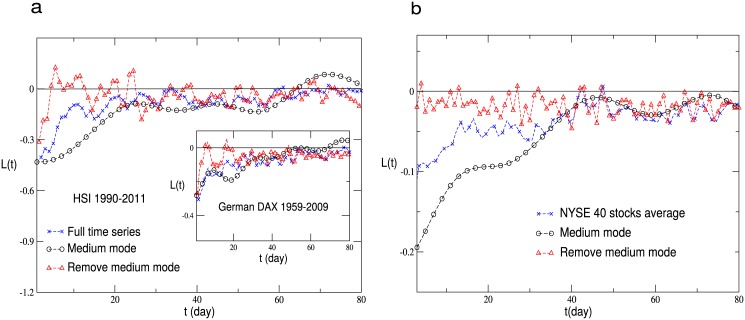

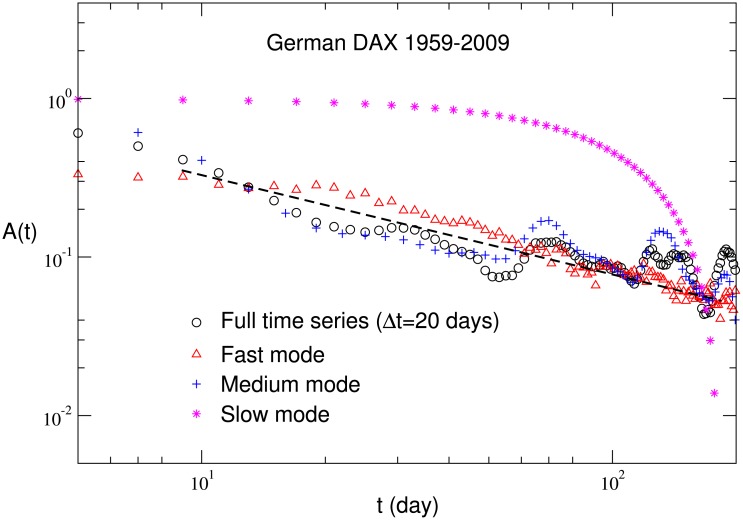

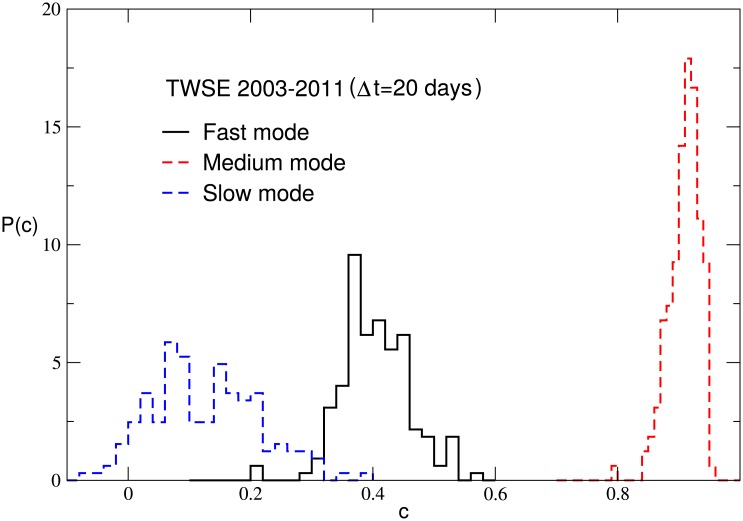

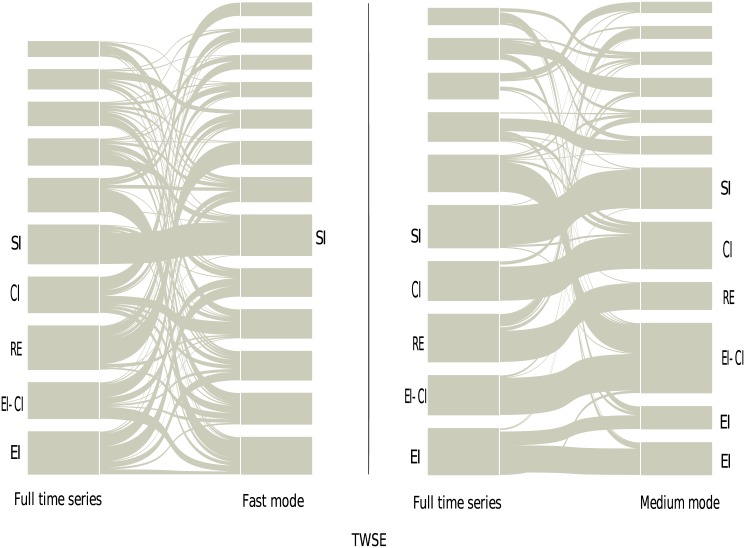

The empirical mode decomposition is applied to analyze the intrinsic multi-scale dynamic behaviors of complex financial systems. In this approach, the time series of the price returns of each stock is decomposed into a small number of intrinsic mode functions, which represent the price motion from high frequency to low frequency. These intrinsic mode functions are then grouped into three modes, i.e., the fast mode, medium mode and slow mode. The probability distribution of returns and auto-correlation of volatilities for the fast and medium modes exhibit similar behaviors as those of the full time series, i.e., these characteristics are rather robust in multi time scale. However, the cross-correlation between individual stocks and the return-volatility correlation are time scale dependent. The structure of business sectors is mainly governed by the fast mode when returns are sampled at a couple of days, while by the medium mode when returns are sampled at dozens of days. More importantly, the leverage and anti-leverage effects are dominated by the medium mode.

应用经验模态分解来分析复杂金融系统的内在多尺度动态行为。在这种方法中,每只股票价格回报的时间序列被分解为少量的本征模态函数,这些函数代表了从高频到低频的价格运动。然后将这些本征模态函数分为三种模式,即快速模式、中速模式和慢速模式。快速模式和中速模式的回报概率分布以及波动率的自相关性表现出与全时间序列相似的行为,即这些特征在多时间尺度上相当稳健。然而,个股之间的交叉相关性以及回报-波动率相关性是时间尺度依赖的。当回报以几天为采样间隔时,商业部门的结构主要由快速模式主导,而当回报以几十天为采样间隔时,则由中速模式主导。更重要的是,杠杆效应和反杠杆效应由中速模式主导。