Research Group of Quantitative Psychology and Individual Differences, KU Leuven-University of Leuven, Leuven, Belgium.

Department of Electrical Engineering (ESAT), STADIUS Center for Dynamical Systems, Signal Processing and Data Analytics, KU Leuven-University of Leuven, Leuven, Belgium.

Sci Rep. 2018 Jan 15;8(1):769. doi: 10.1038/s41598-017-19067-2.

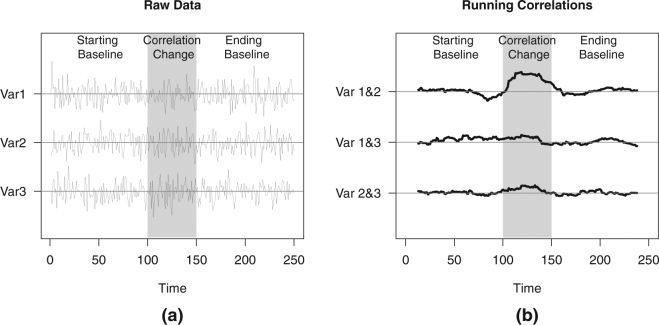

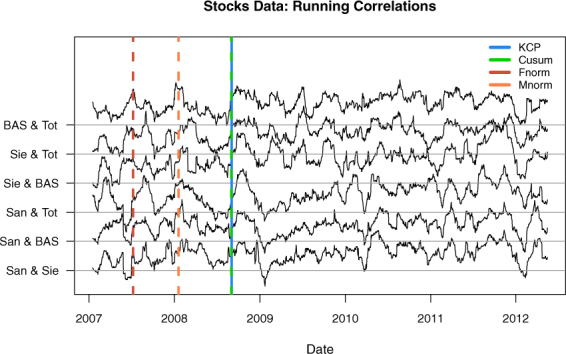

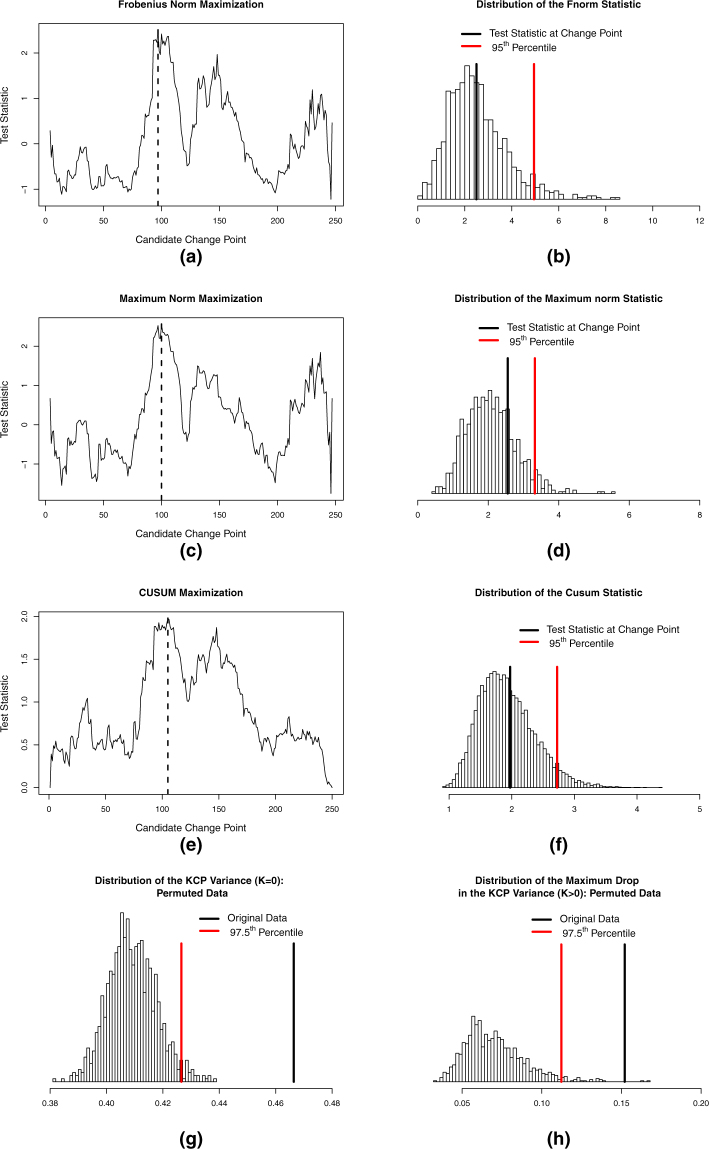

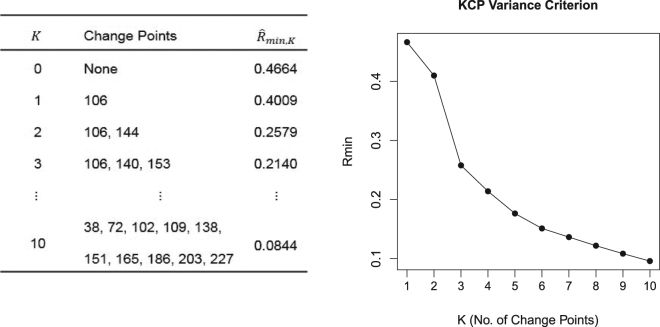

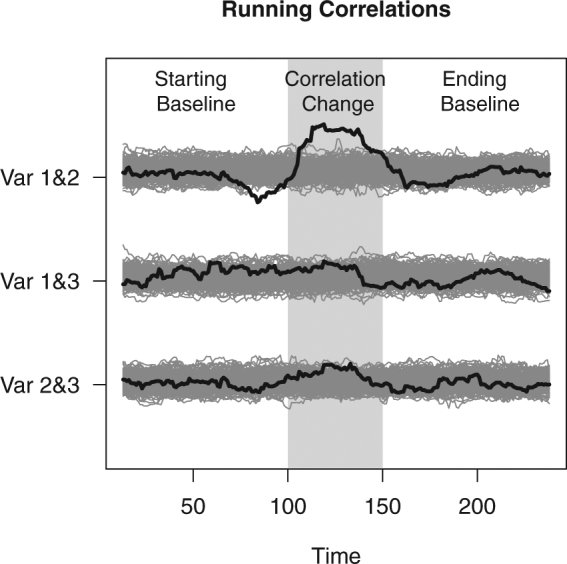

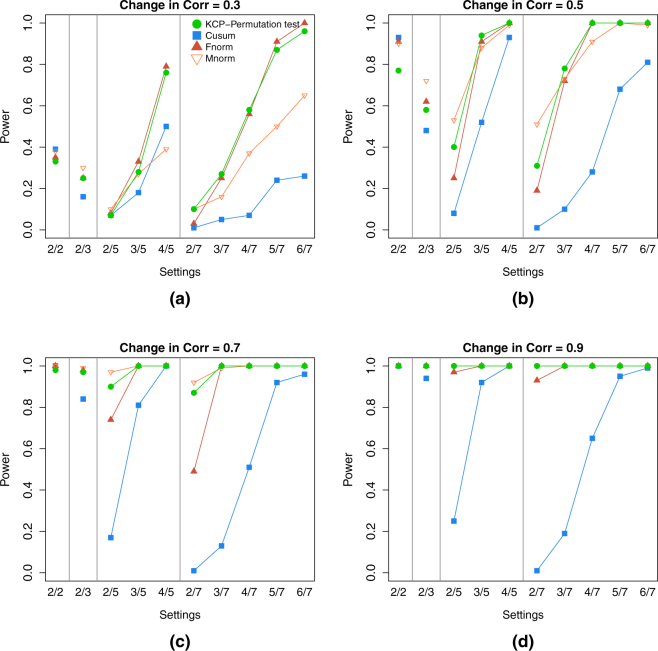

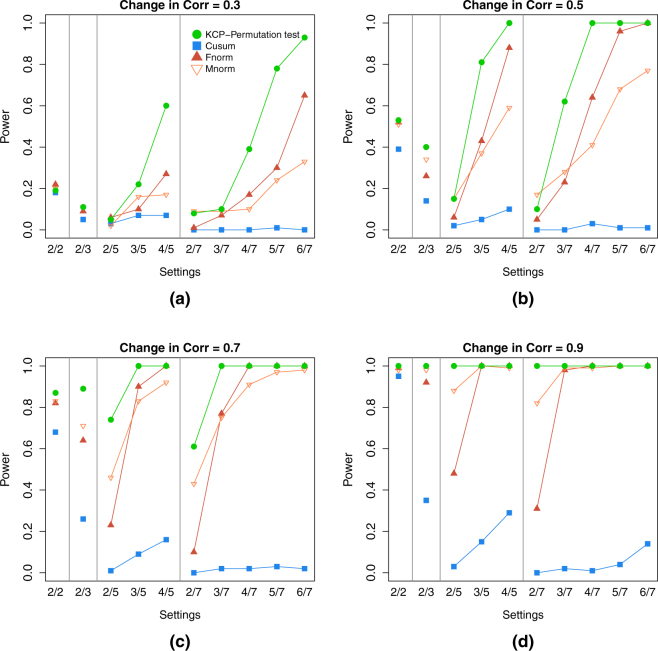

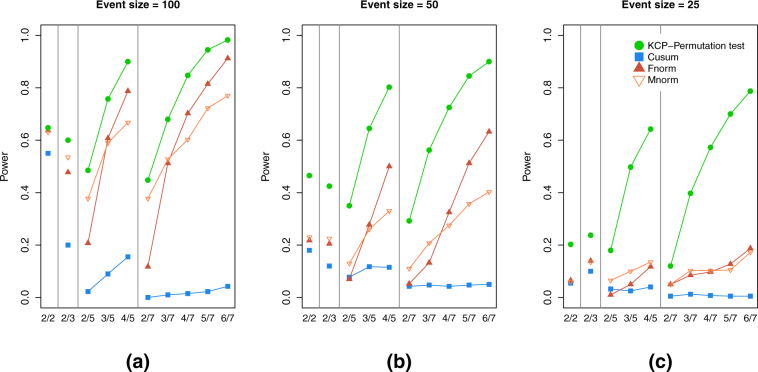

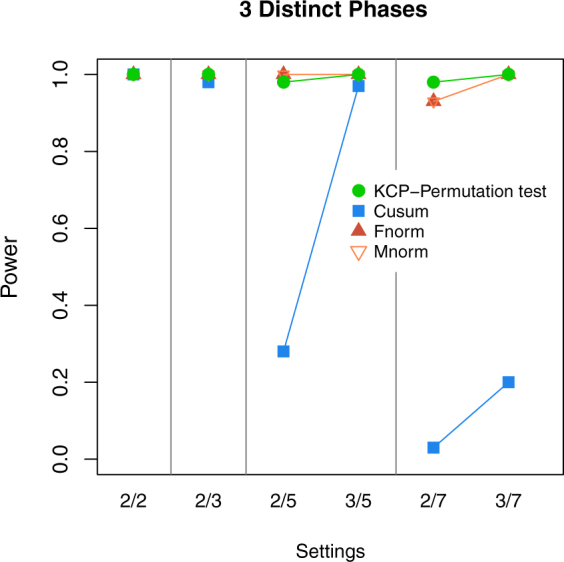

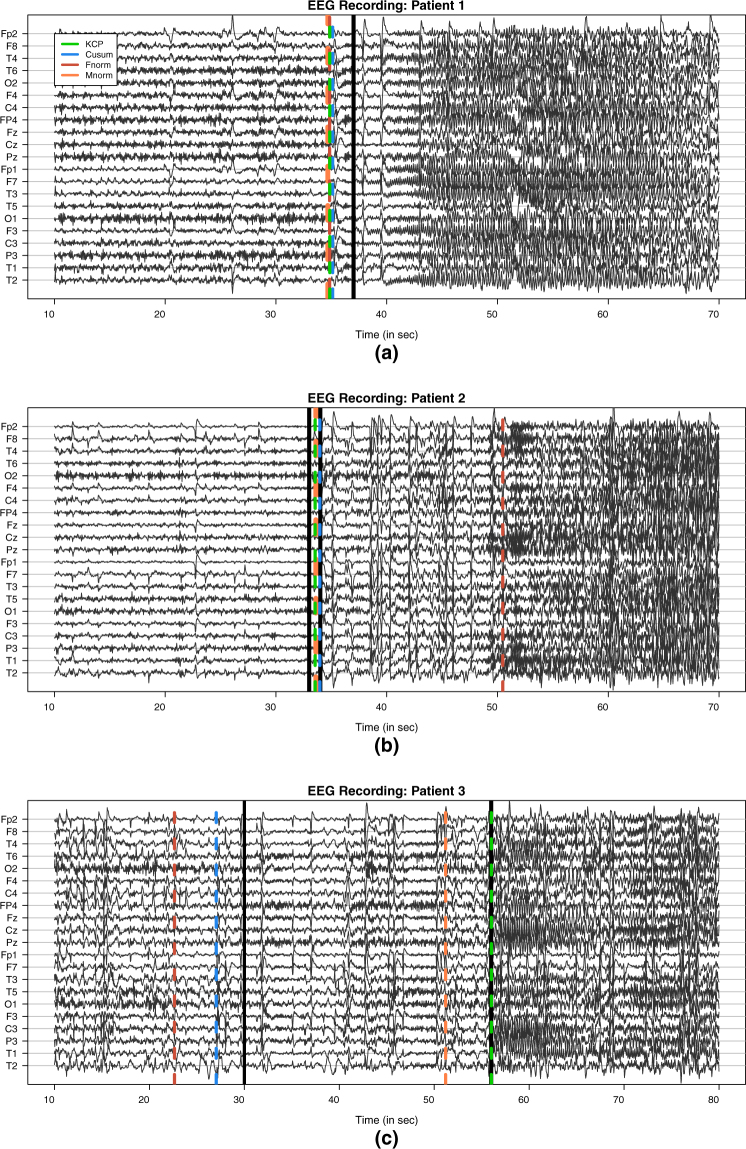

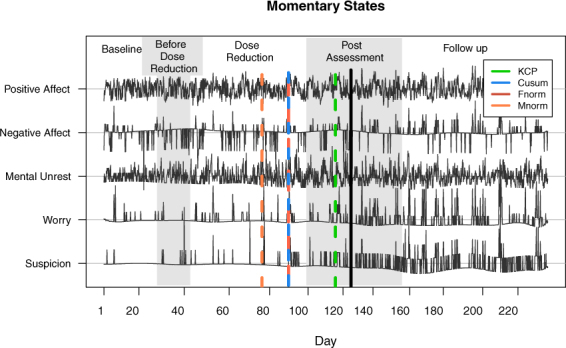

Detecting abrupt correlation changes in multivariate time series is crucial in many application fields such as signal processing, functional neuroimaging, climate studies, and financial analysis. To detect such changes, several promising correlation change tests exist, but they may suffer from severe loss of power when there is actually more than one change point underlying the data. To deal with this drawback, we propose a permutation based significance test for Kernel Change Point (KCP) detection on the running correlations. Given a requested number of change points K, KCP divides the time series into K + 1 phases by minimizing the within-phase variance. The new permutation test looks at how the average within-phase variance decreases when K increases and compares this to the results for permuted data. The results of an extensive simulation study and applications to several real data sets show that, depending on the setting, the new test performs either at par or better than the state-of-the art significance tests for detecting the presence of correlation changes, implying that its use can be generally recommended.

检测多元时间序列中的突然相关变化在信号处理、功能神经影像学、气候研究和金融分析等许多应用领域都至关重要。为了检测这种变化,存在几种有前途的相关变化测试方法,但当数据中实际上存在多个变化点时,它们可能会严重丧失功效。为了解决这个缺点,我们提出了一种基于排列的核变化点 (KCP) 检测的显着性检验方法,用于运行相关性。给定请求的变化点数量 K,KCP 通过最小化阶段内方差将时间序列分为 K+1 个阶段。新的排列检验着眼于当 K 增加时平均阶段内方差如何减小,并将其与排列数据的结果进行比较。广泛的模拟研究和对几个真实数据集的应用结果表明,根据设置的不同,新的检验方法的性能要么与检测相关变化存在的最新显着性检验方法相当,要么更好,这意味着其使用通常可以推荐。