IÉSEG School of Management (LEM - CNRS 9221), Socle de la Grande Arche, 1 Parvis de La Défense, 92044, Paris, La Défense Cedex, France.

University Paris 1 Panthéon-Sorbonne, Finance and Modeling Department, Centre d'Economie de la Sorbonne, 106-112 Boulevard de l'Hôpital, 75013, Paris, France.

Sci Rep. 2019 Apr 5;9(1):5671. doi: 10.1038/s41598-019-42223-9.

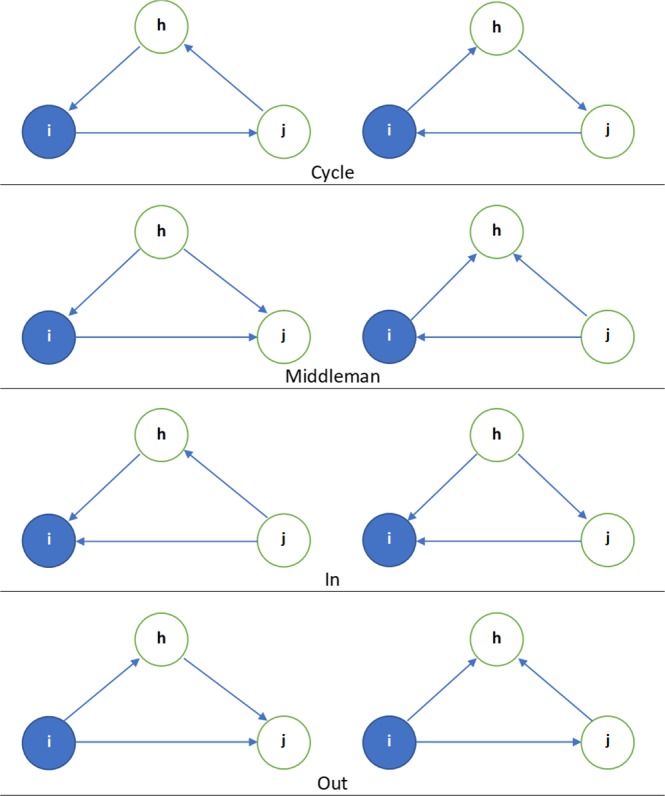

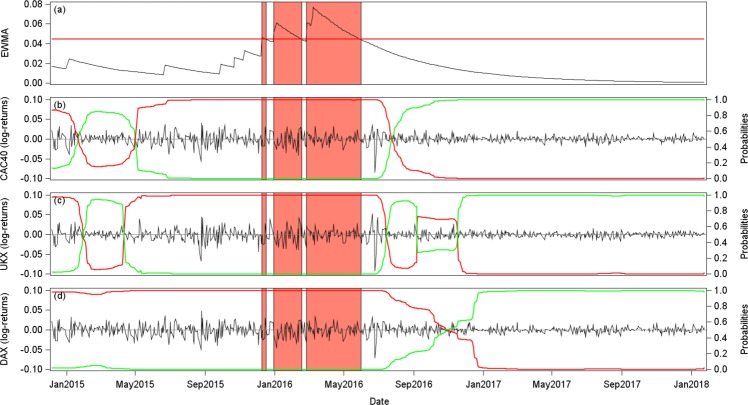

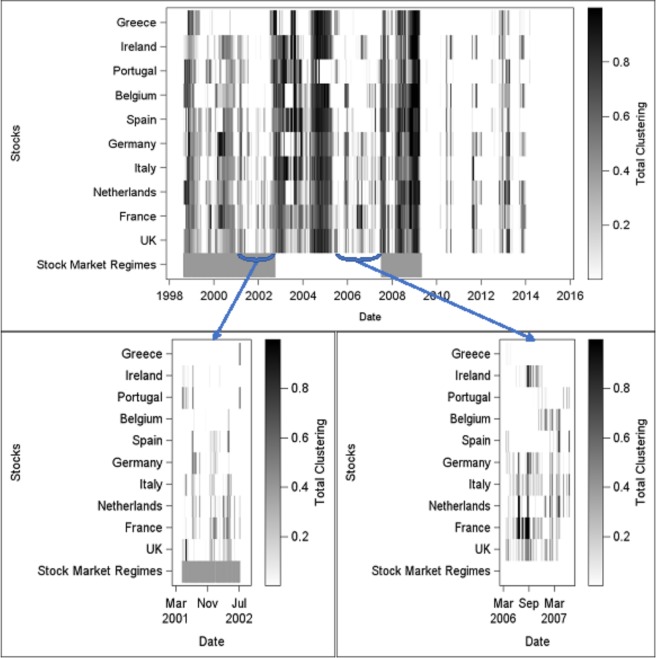

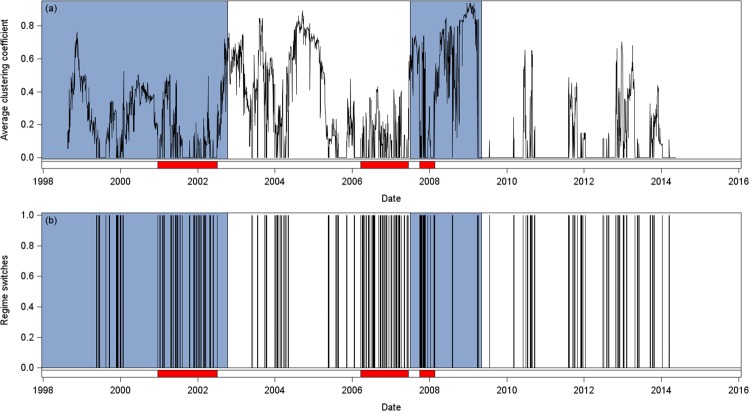

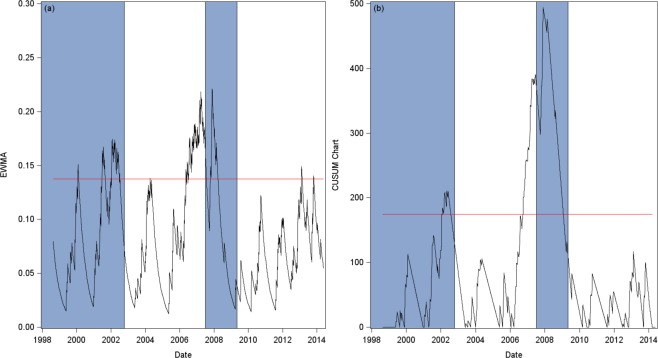

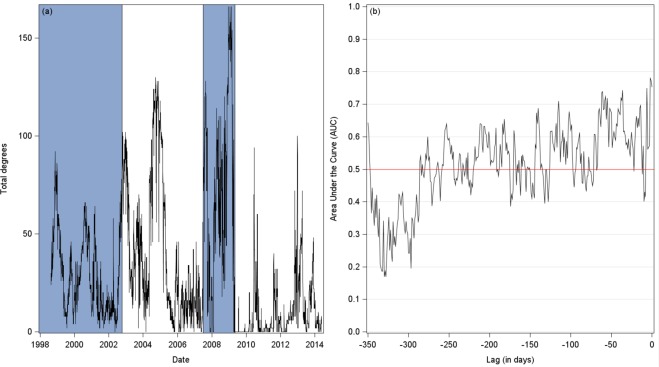

As many complex dynamical systems, financial markets exhibit sudden changes or tipping points that can turn into systemic risk. This paper aims at building and validating a new class of early warning signals of critical transitions. We base our analysis on information spreading patterns in dynamic temporal networks, where nodes are connected by short-term causality. Before a tipping point occurs, we observe flickering in information spreading, as measured by clustering coefficients. Nodes rapidly switch between "being in" and "being out" the information diffusion process. Concurrently, stock markets start to desynchronize. To capture these features, we build two early warning indicators based on the number of regime switches, and on the time between two switches. We divide our data into two sub-samples. Over the first one, using receiver operating curve, we show that we are able to detect a tipping point about one year before it occurs. For instance, our empirical model perfectly predicts the Global Financial Crisis. Over the second sub-sample, used as a robustness check, our two statistical metrics also capture, to a large extent, the 2016 financial turmoil. Our results suggest that our indicators have informational content about a future tipping point, and have therefore strong policy implications.

与许多复杂的动力系统一样,金融市场表现出突然的变化或转折点,可能会转化为系统性风险。本文旨在构建和验证一类新的关键转变预警信号。我们的分析基于动态时间网络中的信息传播模式,其中节点通过短期因果关系连接。在转折点发生之前,我们观察到信息传播中的闪烁,这可以通过聚类系数来衡量。节点在信息扩散过程中快速地在“参与”和“不参与”之间切换。同时,股票市场开始失步。为了捕捉这些特征,我们构建了两个基于状态转换数量和两次转换之间时间的预警指标。我们将数据分为两个子样本。在第一个子样本上,通过接收者操作曲线,我们表明我们能够在转折点发生前大约一年检测到它。例如,我们的实证模型完美地预测了全球金融危机。在第二个子样本上,作为稳健性检验,我们的两个统计指标也在很大程度上捕捉到了 2016 年的金融动荡。我们的结果表明,我们的指标具有关于未来转折点的信息内容,因此具有很强的政策意义。