School of Humanities and Social Sciences, Aston University, Birmingham, B4 7ET, UK.

School of Law, University of Reading, Reading, Berkshire, RG6 6AH, UK.

Global Health. 2019 Sep 25;15(1):56. doi: 10.1186/s12992-019-0495-5.

Sugar sweetened beverages (SSB) are a major source of sugar in the diet. Although trends in consumption vary across regions, in many countries, particularly LMICs, their consumption continues to increase. In response, a growing number of governments have introduced a tax on SSBs. SSB manufacturers have opposed such taxes, disputing the role that SSBs play in diet-related diseases and the effectiveness of SSB taxation, and alleging major economic impacts. Given the importance of evidence to effective regulation of products harmful to human health, we scrutinised industry submissions to the South African government's consultation on a proposed SSB tax and examined their use of evidence.

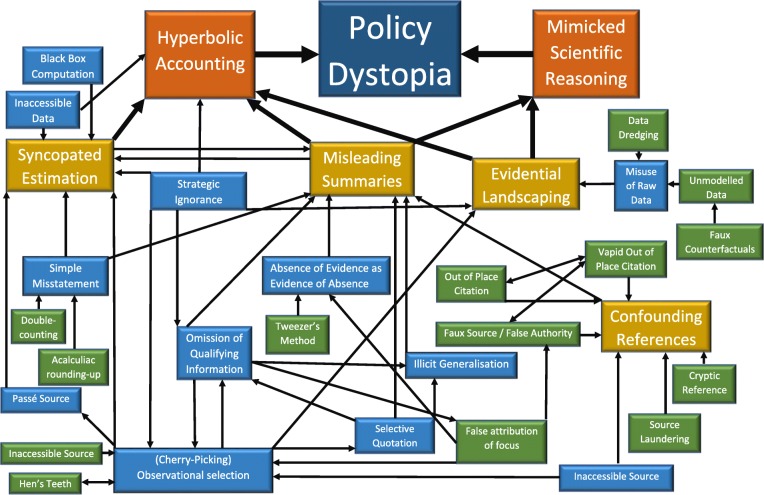

Corporate submissions were underpinned by several strategies involving the misrepresentation of evidence. First, references were used in a misleading way, providing false support for key claims. Second, raw data, which represented a pliable, alternative evidence base to peer reviewed studies, was misused to dispute both the premise of targeting sugar for special attention and the impact of SSB taxes on SSB consumption. Third, purposively selected evidence was used in conjunction with other techniques, such as selective quoting from studies and omitting important qualifying information, to promote an alternative evidential narrative to that supported by the weight of peer-reviewed research. Fourth, a range of mutually enforcing techniques that inflated the effects of SSB taxation on jobs, public revenue generation, and gross domestic product, was used to exaggerate the economic impact of the tax. This "hyperbolic accounting" included rounding up figures in original sources, double counting, and skipping steps in economic modelling.

Our research raises fundamental questions concerning the bona fides of industry information in the context of government efforts to combat diet-related diseases. The beverage industry's claims against SSB taxation rest on a complex interplay of techniques, that appear to be grounded in evidence, but which do not observe widely accepted approaches to the use of either scientific or economic evidence. These techniques are similar, but not identical, to those used by tobacco companies and highlight the problems of introducing evidence-based policies aimed at managing the market environment for unhealthful commodities.

含糖饮料(SSB)是饮食中糖分的主要来源。尽管不同地区的消费趋势有所不同,但在许多国家,特别是中低收入国家,其消费仍在继续增加。对此,越来越多的政府对 SSB 征收了税款。SSB 制造商反对征收此类税款,他们对 SSB 在与饮食相关的疾病中所扮演的角色以及 SSB 征税的有效性提出质疑,并声称会产生重大的经济影响。鉴于证据对于有效监管危害人类健康的产品的重要性,我们仔细审查了行业向南非政府就拟议 SSB 税进行的磋商提交的意见,并审查了其使用证据的情况。

公司的意见主要基于以下几种策略,这些策略涉及对证据的错误表述。首先,引用被以误导的方式使用,为关键主张提供虚假支持。其次,原始数据被滥用,这些数据代表了可替代同行评审研究的灵活证据基础,用来质疑将糖作为特别关注对象的前提以及 SSB 税对 SSB 消费的影响。第三,有选择地使用有针对性选择的证据,同时结合其他技术,如选择性引用研究和省略重要的限定信息,来推广与同行评审研究支持的证据叙事相反的替代叙事。第四,使用了一系列相互强化的技术,夸大了 SSB 税对就业、公共收入和国内生产总值的影响,从而夸大了税收的经济影响。这种“夸张会计”包括在原始来源中四舍五入数字、重复计算和跳过经济建模步骤。

我们的研究提出了一些根本性的问题,即考虑到政府对抗与饮食相关的疾病的努力,行业信息的可信度如何。饮料行业对 SSB 税的反对意见基于一系列技术的复杂相互作用,这些技术似乎基于证据,但却不符合广泛接受的科学或经济证据使用方法。这些技术与烟草公司使用的技术类似,但并不完全相同,这凸显了引入基于证据的政策来管理不健康商品市场环境所面临的问题。