University of Otago Wellington, PO Box 7343, Wellington, New Zealand.

University of Otago, Dunedin, New Zealand.

Int J Behav Nutr Phys Act. 2020 Jul 9;17(1):90. doi: 10.1186/s12966-020-00980-1.

The Pacific Island nation of Tonga (a middle-income country) introduced a sweetened beverage tax of T$0.50/L in 2013, with this increasing further in 2016 (to T$1.00/L), and in 2017 (T$1.50/L; US$0.02/oz). Given the potential importance of such types of fiscal intervention for preventing chronic disease, we aimed to evaluate the impact of these tax changes in Tonga.

Interrupted time series analysis was used to examine monthly import volumes and quarterly price and manufacturing 1 year after each tax change, compared with a counterfactual based on existing trends. Autocorrelation was adjusted for when present, and adjustments were made for changes in GDP per capita, visitor numbers, season and T$/US$ exchange rate.

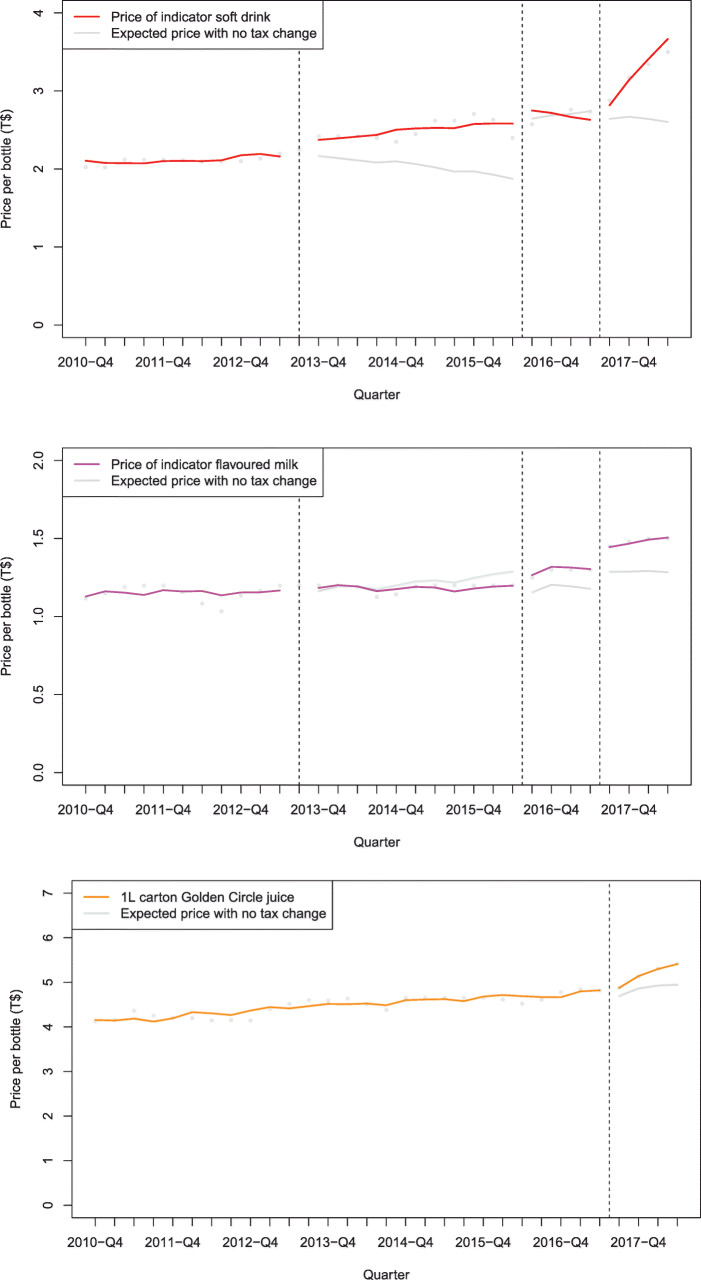

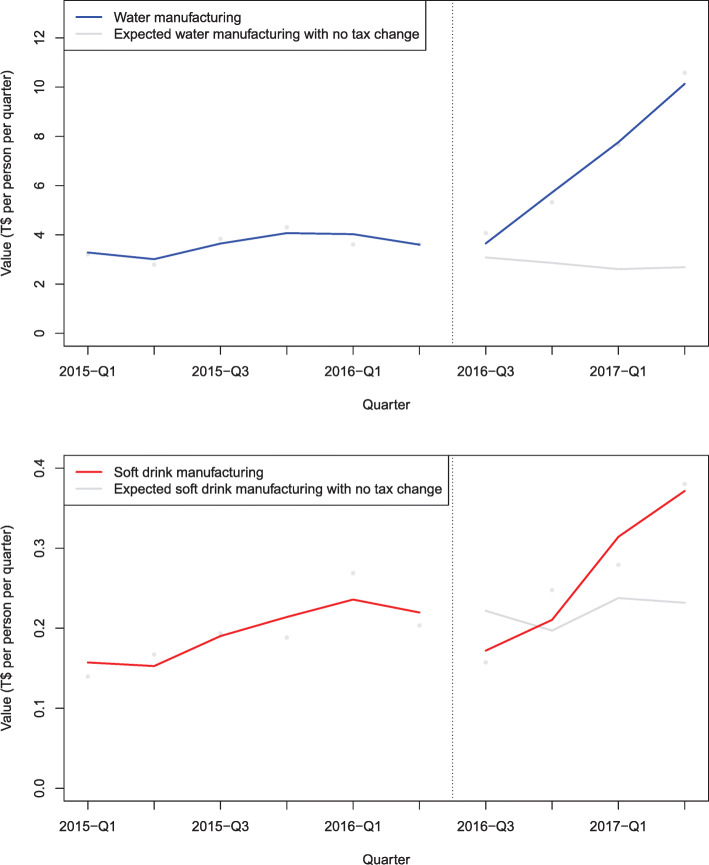

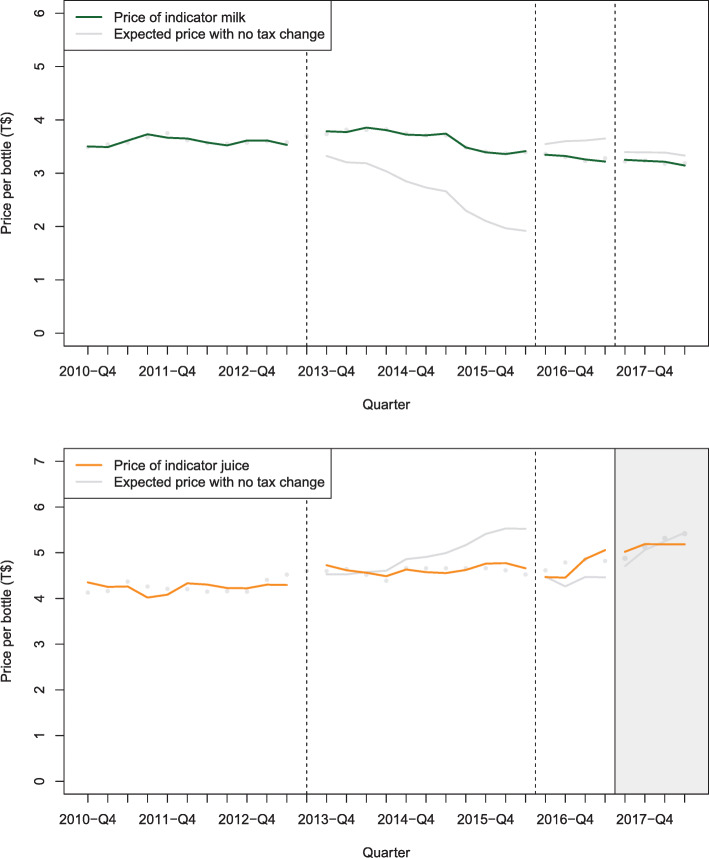

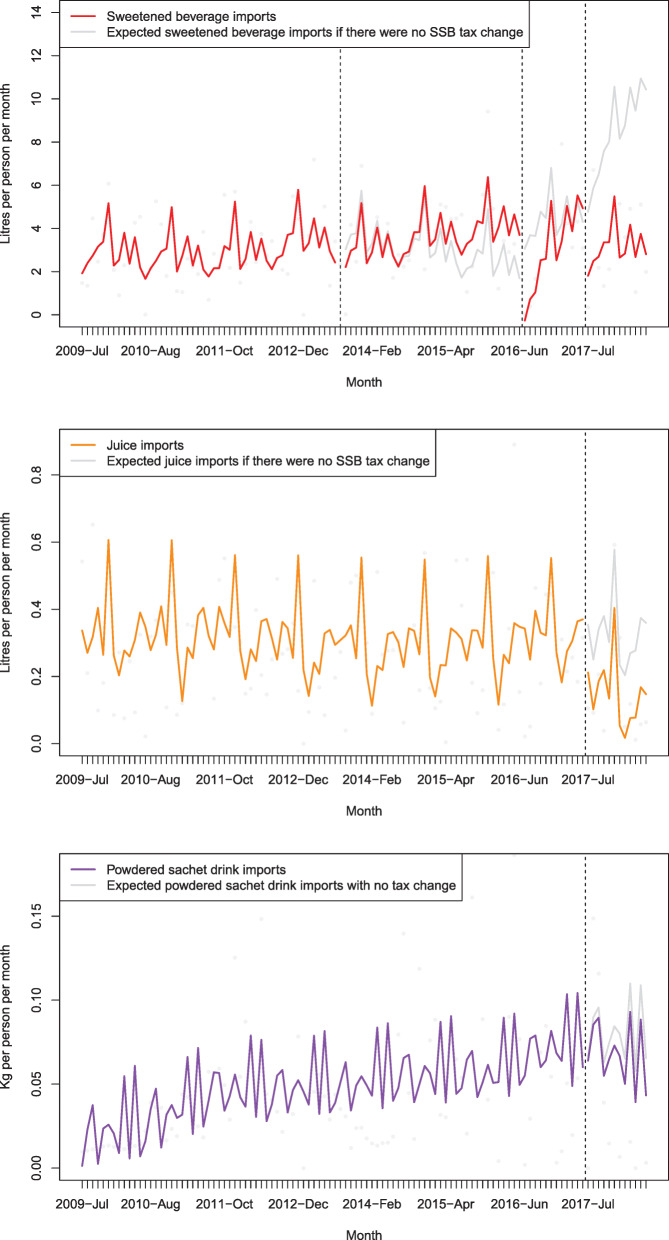

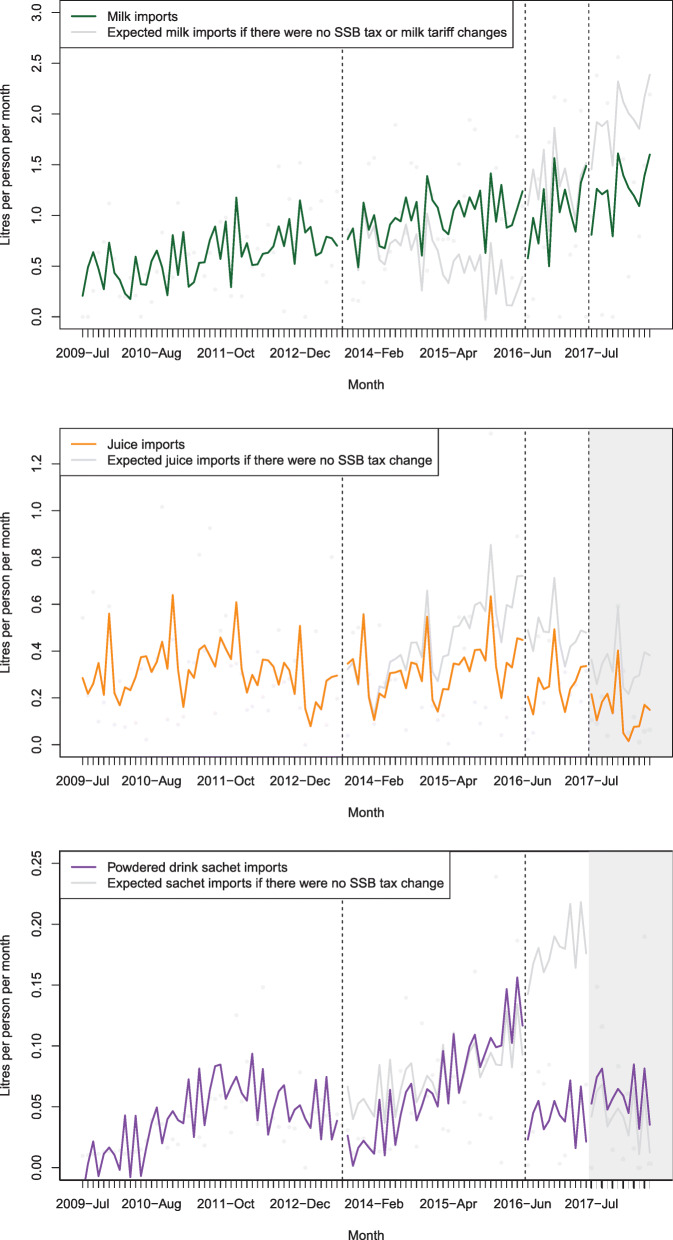

In the year after the 2013, 2016 and 2017 tax increases, the price of an indicator soft drink increased by 16.8% (95%CI: 6.3 to 29.6), 3.7% (- 0.6 to 8.3) and 17.6% (6.0 to 32.0) respectively. Imports of sweetened beverages decreased with changes of - 10.4% (- 23.6 to 9.0), - 30.3% (- 38.8 to - 20.5) and - 62.5% (- 73.1 to - 43.4) respectively. Juice imports changed by - 54.2% (- 93.2 to - 1.1), and sachet drinks by - 15.5% (- 67.8 to 88.3) after the 2017 tax increase. Tonga water bottling (T$) increased in value by 143% (69 to 334) after the 2016 tax increase and soft drink manufacturing increased by 20% (2 to 46, albeit 5% market share).

Consistent with international evaluations of sugar-sweetened beverage taxes, the taxes in Tonga were associated with increased prices, decreased taxed beverages imports, and increased locally bottled water.

汤加(一个中等收入国家)于 2013 年引入了每升 0.50 汤加元(T$)的含糖饮料税,2016 年进一步提高到每升 1.00 汤加元(T$)(0.02 美元/盎司),2017 年提高到每升 1.50 汤加元(T$)(0.02 美元/盎司)。鉴于此类财政干预措施对预防慢性病的重要性,我们旨在评估汤加税收变化的影响。

使用中断时间序列分析,在每次税收变化后 1 年,比较月度进口量和季度价格以及制造业数据,以现有趋势为对照。存在自相关时进行了调整,并对人均 GDP、游客人数、季节和汤加元/美元汇率变化进行了调整。

在 2013 年、2016 年和 2017 年税收增加后的一年中,指示性软饮料价格分别上涨 16.8%(95%CI:6.3 至 29.6)、3.7%(-0.6 至 8.3)和 17.6%(6.0 至 32.0)。含糖饮料进口分别减少 10.4%(-23.6 至 9.0)、30.3%(-38.8 至-20.5)和-62.5%(-73.1 至-43.4)。果汁进口在 2017 年税收增加后下降了 54.2%(-93.2 至-1.1),袋装饮料下降了 15.5%(-67.8 至 88.3)。2016 年税收增加后,汤加瓶装水(T$)的价值增加了 143%(69 至 334),软饮料制造业增加了 20%(2 至 46,尽管市场份额为 5%)。

与国际上对含糖饮料税的评估一致,汤加的税收与价格上涨、受税饮料进口减少和本地瓶装水增加有关。