Auerbach Alan J, Gale William

University of California, Berkeley, USA.

Urban-Brookings Tax Policy Center, Washington, DC USA.

Bus Econ. 2020;55(4):202-212. doi: 10.1057/s11369-020-00188-y. Epub 2020 Oct 12.

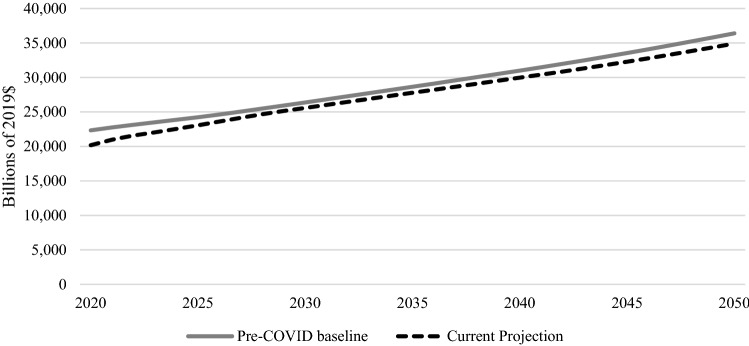

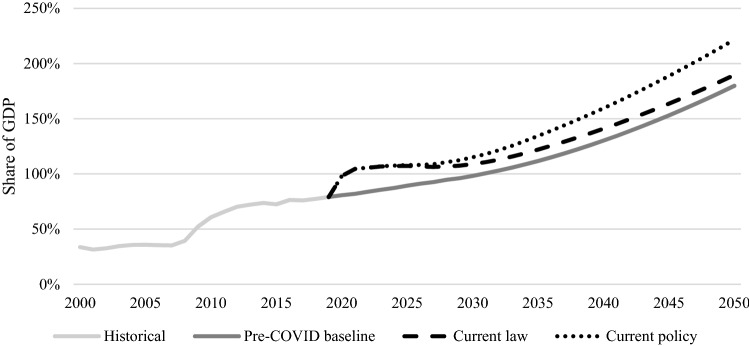

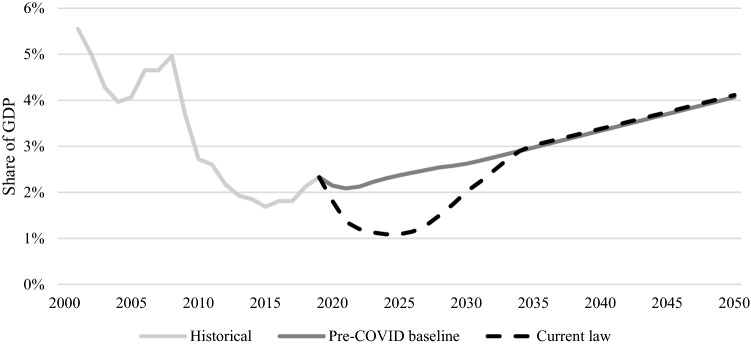

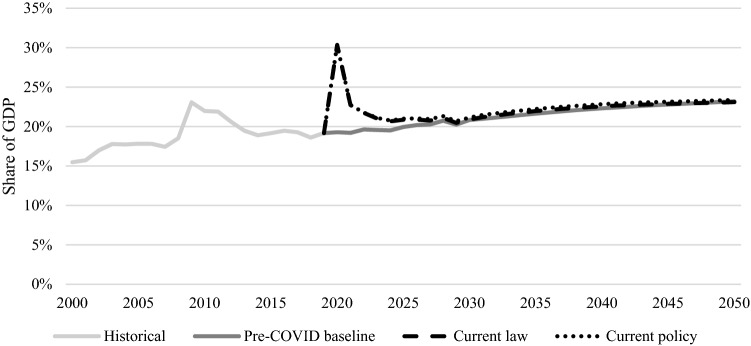

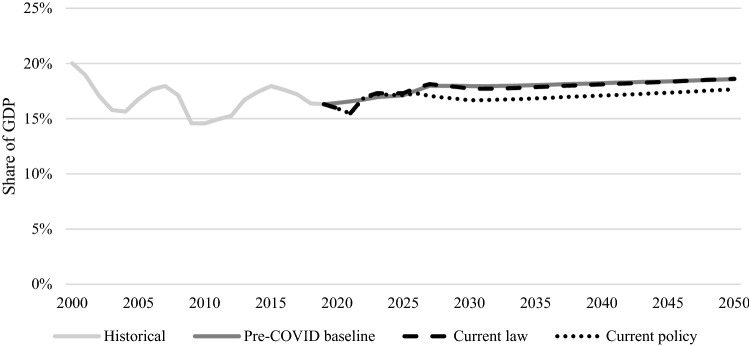

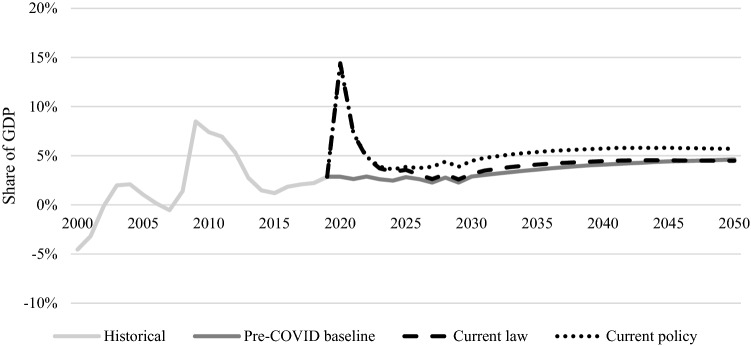

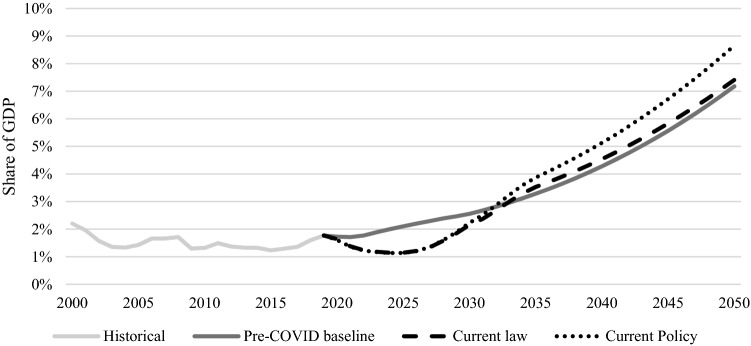

We examine the impact of COVID-19 on the federal budget outlook. We find substantial but temporary effects on spending and revenues, with more moderate but permanent effects on the long-term projections. We project that the debt-to-GDP ratio, currently 98%, will rise to 190% in 2050 under current law, compared to a CBO pre-COVID projection of 180%. Sharply lower interest rates projected for the next dozen years help moderate future debt accumulation. Under a "current policy" projection that allows temporary tax provisions-such as those in the Tax Cut and Jobs Act of 2017-to be made permanent, the debt-to-GDP ratio would rise to 222% by 2050 and would continuing rising thereafter. The long-term projections are sensitive to interest rates. We discuss several aspects of these results, including how the current episode compares to past debt changes, the role of historically low interest rates, and the role of recent Federal Reserve Board policies and actions. Because of the macro-stabilization effects of fiscal tightening, and because low interest rates create "breathing room" for fiscal policy, we do not see the large, short-run debt accumulation resulting from the current pandemic as necessitating any immediate offsetting response. But the long-term projections show that significant fiscal imbalances remain and will eventually require attention.

我们研究了新冠疫情对联邦预算前景的影响。我们发现疫情对支出和收入产生了重大但暂时的影响,对长期预测的影响则较为温和但具有永久性。我们预计,按照现行法律,目前债务与国内生产总值(GDP)的比率为98%,到2050年将升至190%,而国会预算办公室(CBO)在疫情前的预测为180%。预计未来十几年利率大幅下降有助于缓解未来债务积累。在“现行政策”预测下,即允许诸如2017年《减税与就业法案》中的临时税收条款永久化,到2050年债务与GDP的比率将升至222%,此后还会继续上升。长期预测对利率很敏感。我们讨论了这些结果的几个方面,包括当前情况与过去债务变化的比较、历史低利率的作用以及美联储近期政策和行动的作用。由于财政紧缩的宏观稳定效应,且低利率为财政政策创造了“喘息空间”,我们认为当前疫情导致的大规模短期债务积累并不需要立即做出抵消性反应。但长期预测表明,重大财政失衡依然存在,最终需要加以关注。