SAMRC/Wits Centre for Health Economics and Decision Science - Priority Cost Effective Lessons for Systems Strengthening (PRICELESS SA), School of Public Health, University of the Witwatersrand, Johannesburg, South Africa.

Menzies Centre for Health Policy and Director of Academic Titles, School of Public Health, The University of Sydney, Sydney, Australia.

Glob Health Action. 2021 Jan 1;14(1):1884358. doi: 10.1080/16549716.2021.1884358.

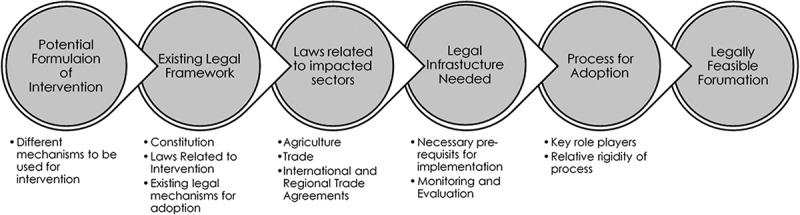

: A number of countries have adopted sugar-sweetened beverage taxes to prevent non-communicable diseases but there is variance in the structures and rates of the taxes. As interventions, sugar-sweetened beverage taxes could be cost-effective but must be compliant with existing legal and taxation systems.: To assess the legal feasibility of introducing or strengthening taxation laws related to sugar-sweetened beverages, for prevention of non-communicable diseases in seven countries: Botswana, Kenya, Namibia, Rwanda, Tanzania, Uganda and Zambia.: We assessed the legal feasibility of adopting four types of sugar-sweetened beverage tax formulations in each of the seven countries, using the novel FELIP framework. We conducted a desk-based review of the legal system related to sugar-sweetened beverage taxation and assessed the barriers to, and facilitators and legal feasibility of, introducing each of the selected formulations by considering the existing laws, laws related to impacted sectors, legal infrastructure, and processes involved in adopting laws.: Six countries had legal mandates to prevent non-communicable diseases and protect the health of citizens. As of 2019, all countries had excise tax legislation. Five countries levied excise taxes on all soft drinks, but most did not exclusively target sugar-sweetened beverages, and taxation rates were well below the World Health Organization's recommended 20%. In Uganda and Kenya, agricultural or HIV-related levies offered alternative mechanisms to disincentivise consumption of sugar-sweetened beverages without the introduction of new taxes. Nutrition-labelling laws in all countries made it feasible to adopt taxes linked to the sugar content of beverages, but there were lacunas in existing infrastructure for more sophisticated taxation structures.: Sugar-sweetened beverage taxes are legally feasible in all seven countries Existing laws provide a means to implement taxes as a public health intervention.

一些国家已采取含糖饮料税来预防非传染性疾病,但这些税收的结构和税率存在差异。作为干预措施,含糖饮料税可能具有成本效益,但必须符合现行法律和税收制度。

为评估在七个国家(博茨瓦纳、肯尼亚、纳米比亚、卢旺达、坦桑尼亚、乌干达和赞比亚)引入或加强与含糖饮料相关的税收法律以预防非传染性疾病的法律可行性:

我们使用新颖的 FELIP 框架评估了在这七个国家中的每一个国家中采用四种类型的含糖饮料税方案的法律可行性。我们对与含糖饮料征税相关的法律制度进行了基于桌面的审查,并通过考虑现行法律、受影响部门的相关法律、法律基础设施以及采用法律所涉及的程序,评估了每种选定方案的引入障碍、促进因素和法律可行性。

六个国家具有预防非传染性疾病和保护公民健康的法律授权。截至 2019 年,所有国家都有消费税立法。五个国家对所有软饮料征收消费税,但大多数国家并未专门针对含糖饮料征税,且税率远低于世界卫生组织建议的 20%。在乌干达和肯尼亚,农业或 HIV 相关的征税提供了一种替代机制,可以在不引入新税的情况下抑制含糖饮料的消费。所有国家的营养标签法都使得采用与饮料含糖量相关的税收成为可能,但在更复杂的税收结构方面,现有基础设施存在空白。

在所有七个国家,含糖饮料税在法律上都是可行的,现有法律为实施作为公共卫生干预措施的税收提供了一种手段。