Division of Health Policy and Administration, School of Public Health, University of Illinois Chicago, Chicago, Illinois, United States of America.

Institute for Health Research and Policy, University of Illinois Chicago, Chicago, Illinois, United States of America.

PLoS One. 2021 Jun 2;16(6):e0252094. doi: 10.1371/journal.pone.0252094. eCollection 2021.

Sugar-sweetened beverage (SSB) taxes have been implemented worldwide to raise revenue and reduce consumption of SSBs, which is associated with health harms. Empirical evaluations have found that these taxes are successful at reducing demand for SSBs; however, SSB taxes face opposition, in part because of claims that they will lead to substantial job losses. The purpose of this study is to examine the impact of the San Francisco SSB tax, implemented on January 1st, 2018, on employment.

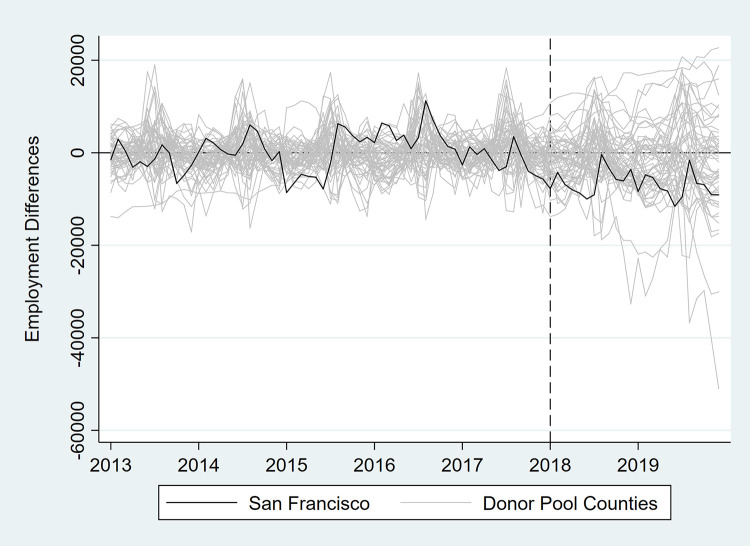

Monthly employment counts were obtained from the Bureau of Labor Statistics from January 2013 (5-years pre-tax) through December 2019 (2-years post-tax) for the overall economy, private sector, supermarkets and other grocery stores, convenience stores, limited-service restaurants, and beverage manufacturing. A synthetic control analysis was conducted for each employment outcome. The synthetic controls (i.e., estimated counterfactuals) were generated from a pool of urban control counties using pre-tax labor market-related characteristics.

The synthetic controls had similar labor market-related characteristics and employment outcomes to those in San Francisco in the pre-tax period. Up to 2 years post-tax, differences in employment between San Francisco and the synthetic controls were small and not "statistically significant" based on placebo tests for all employment outcomes.

Up to two years post-tax, we do not find evidence that the San Francisco SSB tax negatively impacted net employment, employment in the private sector, or employment in specific SSB-related industries.

全球范围内已实施了含糖饮料(SSB)税,以增加收入并减少 SSB 的消费,因为 SSB 的消费与健康危害有关。实证评估发现,这些税收在降低 SSB 的需求方面是成功的;然而,SSB 税面临着反对,部分原因是有人声称它们将导致大量失业。本研究的目的是检验 2018 年 1 月 1 日生效的旧金山 SSB 税对就业的影响。

从劳工统计局获得了 2013 年 1 月(征税前 5 年)至 2019 年 12 月(征税后 2 年)的总体经济、私营部门、超市和其他杂货店、便利店、有限服务餐厅以及饮料制造业的每月就业人数。对每个就业结果进行了合成控制分析。合成控制(即估计的反事实)是从征税前的劳动市场相关特征的一组城市对照县中生成的。

合成控制在征税前与旧金山具有相似的劳动市场相关特征和就业结果。在征税后长达 2 年的时间里,旧金山和合成控制之间的就业差异很小,根据所有就业结果的安慰剂检验,差异并不“具有统计学意义”。

在征税后长达 2 年的时间里,我们没有发现证据表明旧金山 SSB 税对净就业、私营部门就业或特定 SSB 相关行业的就业产生负面影响。