Division of Health Policy and Administration, School of Public Health, University of Illinois at Chicago, Chicago, IL, USA.

Department of Agricultural and Resource Economics, University of Connecticut, Storrs, CT, USA.

J Public Health Policy. 2020 Jun;41(2):125-138. doi: 10.1057/s41271-019-00217-x.

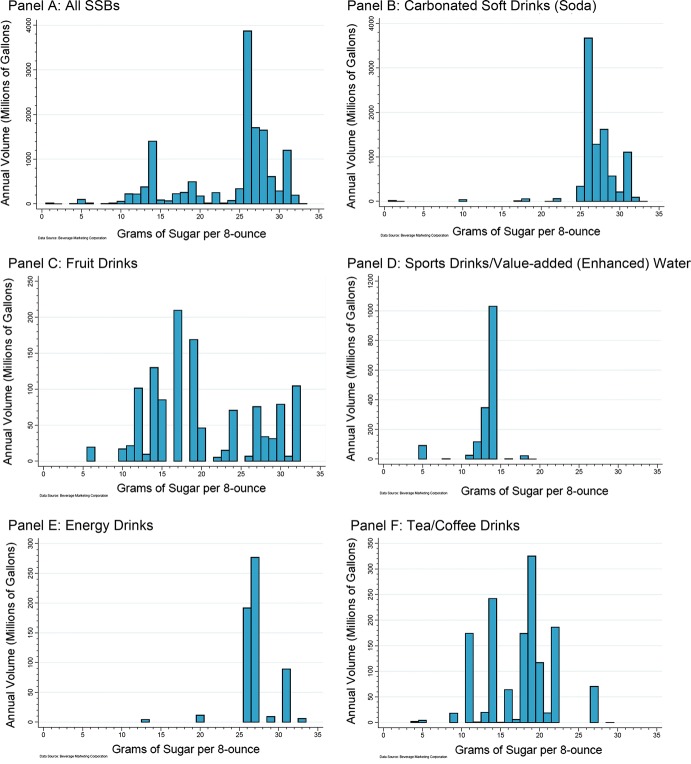

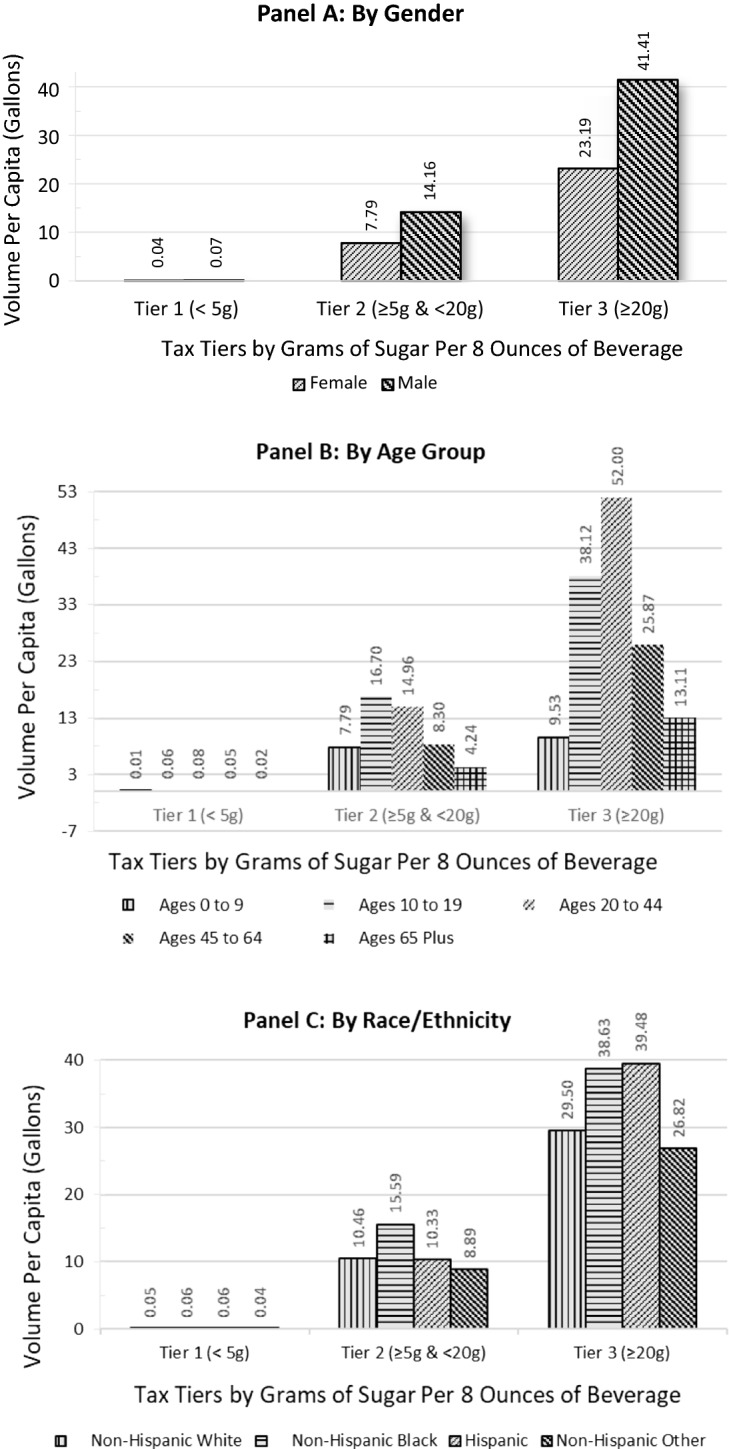

This study draws on data on sales volume, brand-level market shares, and sugar content to calculate the distribution of sugar-sweetened beverage (SSB) sales volume by sugar content, propose sugar content thresholds for a tiered tax structure, and estimate tax revenue. The most common SSBs sold had 26 g of sugar/8-oz serving; 70.8% had ≥ 25 g of sugar/8-oz serving, 16.9% were in the 10-15 g range, and 8.7% were in the 16-20 g range. A tiered tax with cut points at < 20 g and < 5 g of sugar/8-oz serving is proposed. A tax of 1¢/oz for SSBs in the second tier and 2¢/oz in third tier is projected to raise $18.2 billion in tax revenue similar to the 1.5¢/oz flat tax projection ($18.0 billion) but would yield 9% lower SSB volume. Understanding the distribution of SSB sales volume by sugar content informs policymakers on tiered tax structures, which may discourage consumption of SSBs with high levels of sugar and incentivize reformulation.

本研究利用销售量、品牌市场份额和含糖量数据,计算了含糖量的含糖饮料(SSB)销售量分布,提出了分层税收结构的含糖量阈值,并估计了税收收入。销售的最常见 SSB 每 8 盎司含有 26 克糖;70.8%的 SSB 每 8 盎司含糖量≥25 克,16.9%的 SSB 含糖量在 10-15 克之间,8.7%的 SSB 含糖量在 16-20 克之间。建议采用分层税,起征点为<20 克和<5 克糖/8 盎司。预计对含糖量为 2 美分/盎司的 SSB 征收 1 美分/盎司的税,对含糖量为 3 美分/盎司的 SSB 征收 2 美分/盎司的税,可带来 182 亿美元的税收收入,与 1.5 美分/盎司的平税预测(180 亿美元)相似,但 SSB 销量将降低 9%。了解 SSB 销售量的含糖量分布可为政策制定者提供分层税收结构的信息,这可能会抑制高糖 SSB 的消费,并鼓励配方改革。