Shi Wen, Hu Xiao-Min, Chen Wei-Neng

School of Computer Science and Engineering, South China University of Technology, Guangzhou, China.

School of Computers, Guangdong University of Technology, Guangzhou, China.

Complex Intell Systems. 2022;8(5):3989-4003. doi: 10.1007/s40747-021-00640-2. Epub 2022 Mar 5.

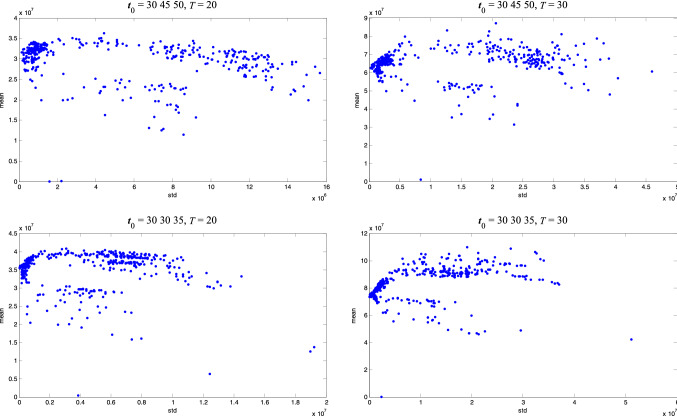

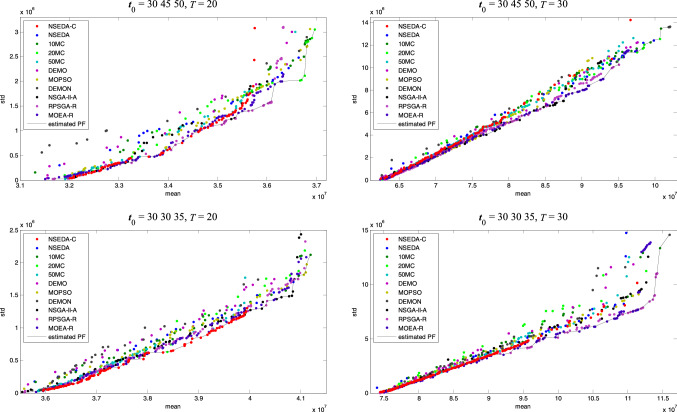

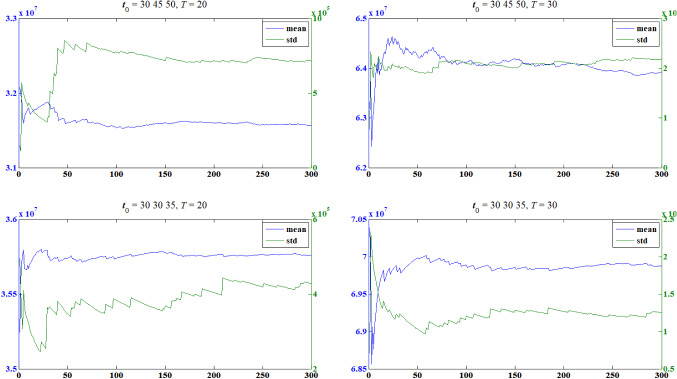

One important problem in financial optimization is to search for robust investment plans that can maximize return while minimizing risk. The market environment, namely the scenario of the problem in optimization, always affects the return and risk of an investment plan. Those financial optimization problems that the performance of the investment plans largely depends on the scenarios are defined as scenario-based optimization problems. This kind of uncertainty is called scenario-based uncertainty. The consideration of scenario-based uncertainty in multi-objective optimization problem is a largely under explored domain. In this paper, a nondominated sorting estimation of distribution algorithm with clustering (NSEDA-C) is proposed to deal with scenario-based robust financial problems. A robust group insurance portfolio problem is taken as an instance to study the features of scenario-based robust financial problems. A simplified simulation method is applied to measure the return while an estimation model is devised to measure the risk. Applications of the NSEDA-C on the group insurance portfolio problem for real-world insurance products have validated the effectiveness of the proposed algorithm.

金融优化中的一个重要问题是寻找稳健的投资计划,该计划能够在将风险降至最低的同时实现回报最大化。市场环境,即优化问题中的情景,始终会影响投资计划的回报和风险。那些投资计划的表现很大程度上取决于情景的金融优化问题被定义为基于情景的优化问题。这种不确定性被称为基于情景的不确定性。在多目标优化问题中考虑基于情景的不确定性是一个很大程度上尚未被探索的领域。本文提出了一种带聚类的非支配排序分布估计算法(NSEDA-C)来处理基于情景的稳健金融问题。以一个稳健的团体保险投资组合问题为例,研究基于情景的稳健金融问题的特征。应用一种简化的模拟方法来衡量回报,同时设计一个估计模型来衡量风险。NSEDA-C在实际保险产品的团体保险投资组合问题上的应用验证了所提算法的有效性。