National Clinician Scholars Program, University of Pennsylvania, Philadelphia.

Corporal Michael J. Crescenz VA Medical Center, Philadelphia, Pennsylvania.

JAMA Health Forum. 2022 May 20;3(5):e221096. doi: 10.1001/jamahealthforum.2022.1096. eCollection 2022 May.

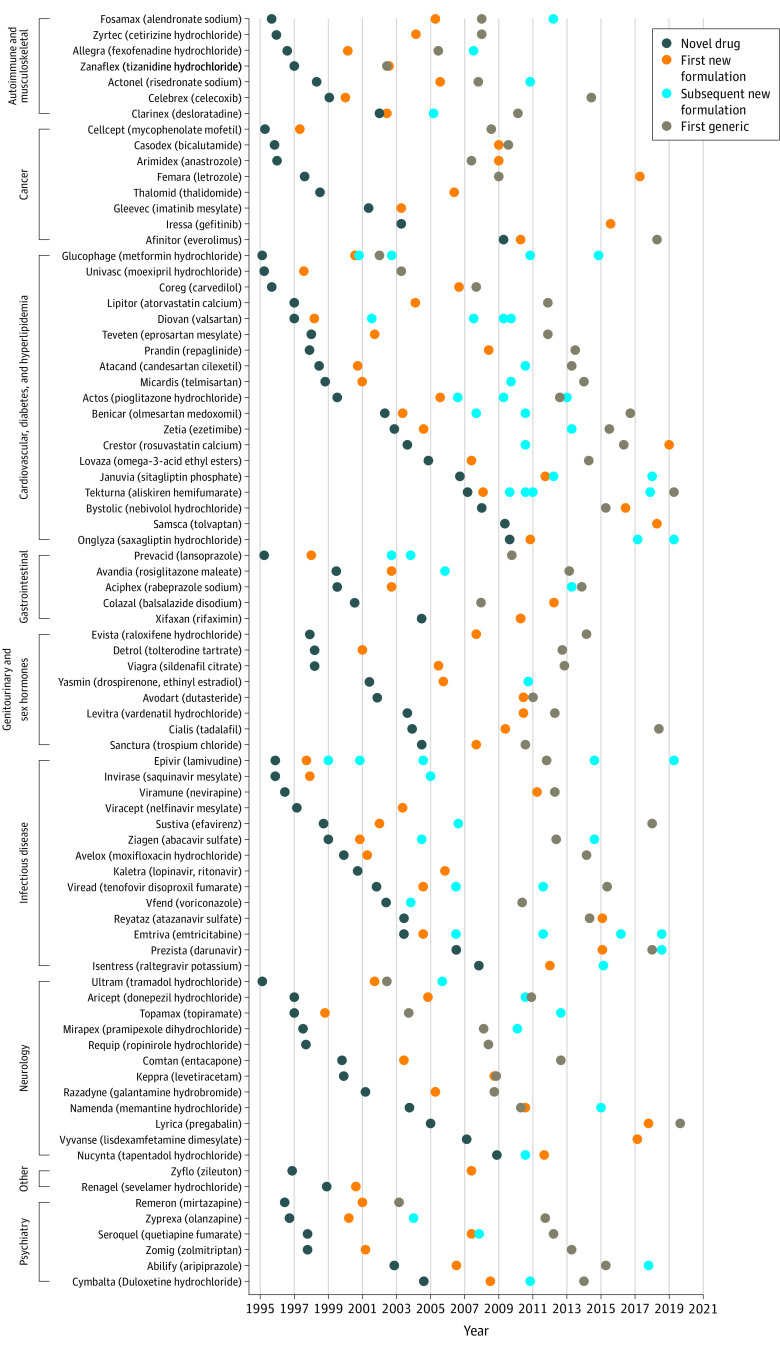

New formulations of prescription drugs can improve convenience and tolerability for patients, but they also constitute manufacturer strategies to extend brand-name drug market exclusivity periods.

To examine whether new formulations of brand-name novel drugs were associated with novel drugs' sales and/or therapeutic value, as well as characterize first new formulations' approval timing relative to the novel drug's generic approval.

This cross-sectional study used the Drugs@FDA database to identify all novel tablet and capsule drugs approved by the US Food and Drug Administration (FDA) between 1995 and 2010 and followed through December 31, 2021.

Novel drugs' blockbuster status, defined as annual sales of $1 billion or greater, and therapeutic value, measured by (1) accelerated approval status, (2) World Health Organization Model Lists of Essential Medicines inclusion, (3) innovativeness, and (4) clinical usefulness.

Approval of a new formulation and timing relative to a novel drug's first generic's approval.

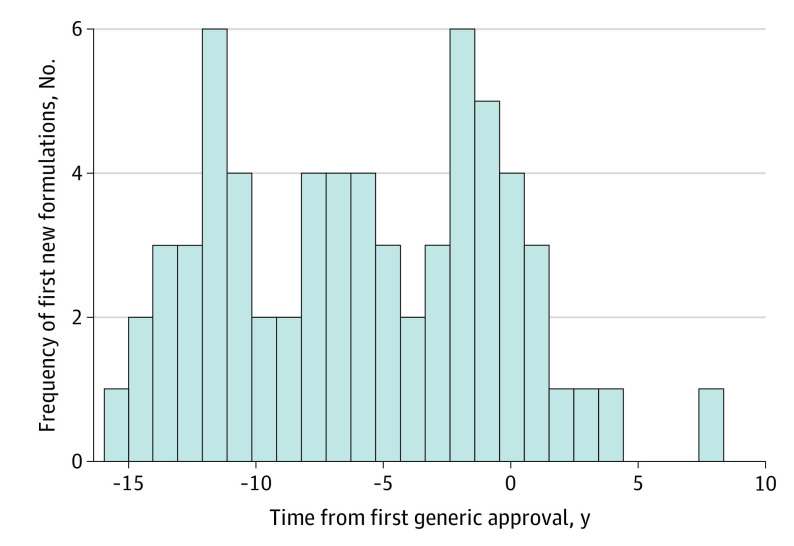

Among the 206 novel drugs in tablet or capsule form approved by the FDA from 1995 to 2010, 81 (39.3%) were followed by an FDA-approved new formulation, and 167 (81.1%) had a generic version as of December 31, 2021. In multivariable analyses, new formulations were statistically significantly more likely among blockbuster drugs vs not (58.2% vs 27.6%; adjusted odds ratio [AOR], 4.72; 95% CI, 2.26-9.87; < .001) and those granted accelerated approval vs not (50.0% vs 37.6%; AOR, 5.48; 95% CI, 1.52-19.67; = .009), and less likely among orphan products vs not (11.8% vs 44.8%; AOR, 0.13; 95% CI, 0.03-0.52; = .004). Essential medicine listing vs no listing (47.8% vs 36.9%; AOR, 1.32; 95% CI, 0.52-3.34; = .56), first-in-class or advance-in-class status vs addition-to-class status (37.8% vs 40.5%; AOR, 0.71; 95% CI, 0.32-1.58; = .40), and categorization as clinically useful vs not useful (40.9% vs 44.8%; AOR, 0.81; 95% CI, 0.34-1.92; = .64) were not associated with increased likelihood of a new formulation. First new formulations were statistically significantly less likely to be approved after the novel drug's first generic approval (84.6% vs 15.4%; < .001).

In this cross-sectional study of novel drugs in tablet or capsule form approved by the FDA between 1995 and 2010, manufacturers pursued new formulations of best-selling brand-name drugs and those granted accelerated approval but did so less frequently once generic competitors entered the market. Other measures of therapeutic value were not associated with new formulations.

新的处方药配方可以提高患者的便利性和耐受性,但它们也是制造商延长品牌药物市场独占期的策略。

研究新的品牌新药制剂是否与新药的销售和/或治疗价值相关,并描述新药首次批准与仿制药批准的时间关系。

设计、地点和参与者:本横断面研究使用 Drugs@FDA 数据库,确定了 1995 年至 2010 年间美国食品和药物管理局(FDA)批准的所有新型片剂和胶囊药物,并跟踪至 2021 年 12 月 31 日。

新药的重磅炸弹地位,定义为年销售额超过 10 亿美元,以及治疗价值,通过(1)加速批准地位,(2)世界卫生组织基本药物清单的纳入,(3)创新性和(4)临床有用性来衡量。

新制剂的批准以及与新药首次仿制药批准的时间关系。

在 1995 年至 2010 年间 FDA 批准的 206 种片剂或胶囊形式的新型药物中,81 种(39.3%)随后获得了 FDA 批准的新配方,截至 2021 年 12 月 31 日,其中 167 种(81.1%)有仿制药。在多变量分析中,与非重磅炸弹药物相比,新制剂在畅销药物中更有可能出现(58.2%比 27.6%;调整后的优势比[OR],4.72;95%CI,2.26-9.87; < .001)和获得加速批准的药物(50.0%比 37.6%;OR,5.48;95%CI,1.52-19.67; = .009),而孤儿产品的可能性较小(11.8%比 44.8%;OR,0.13;95%CI,0.03-0.52; = .004)。列入基本药物清单与未列入清单(47.8%比 36.9%;OR,1.32;95%CI,0.52-3.34; = .56),首创或领先类别地位与类别内附加地位(37.8%比 40.5%;OR,0.71;95%CI,0.32-1.58; = .40),以及临床有用性与无有用性分类(40.9%比 44.8%;OR,0.81;95%CI,0.34-1.92; = .64)与新制剂的可能性增加无关。与新药首次仿制药批准相比,新药的新制剂首次批准的可能性显著降低(84.6%比 15.4%; < .001)。

在这项对 1995 年至 2010 年间 FDA 批准的片剂或胶囊形式的新型药物的横断面研究中,制造商对畅销的品牌药物和获得加速批准的药物进行了新的制剂开发,但一旦仿制药竞争对手进入市场,他们这样做的频率就会降低。其他治疗价值的衡量标准与新制剂无关。