Samitas Aristeidis, Kampouris Elias, Polyzos Stathis

College of Business, Zayed University, P. O. Box 144534, Abu Dhabi, United Arab Emirates.

College of Business, Abu Dhabi University, P.O. Box 1790, Abu Dhabi, United Arab Emirates.

Int Rev Financ Anal. 2022 Mar;80:102005. doi: 10.1016/j.irfa.2021.102005. Epub 2021 Dec 23.

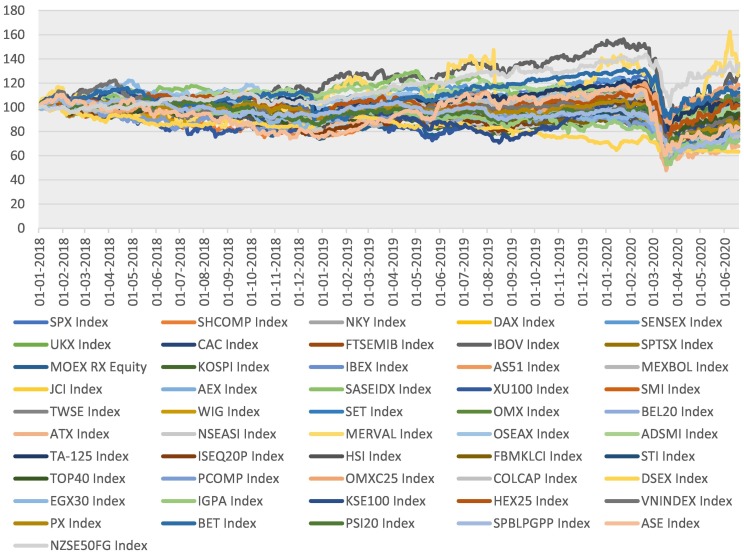

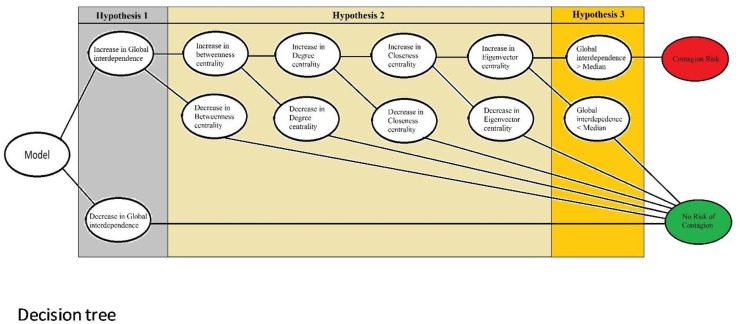

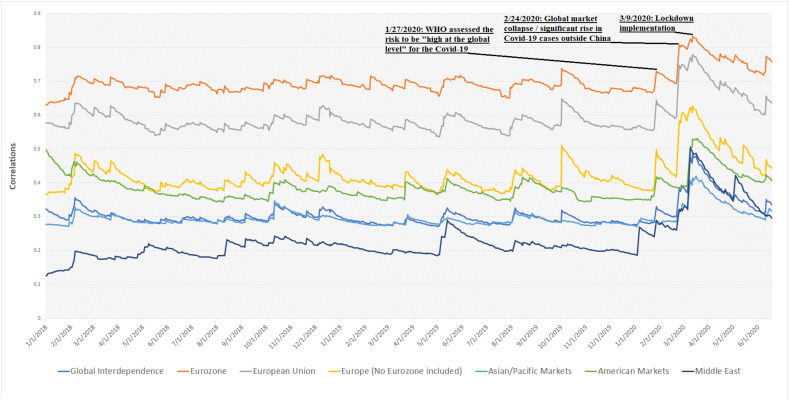

This paper examines the impact of the COVID-19 pandemic on 51 major stock markets, both emerging and developed. We isolated the countries susceptible to shock transmissions, and evaluated countries with immunity, during the lockdown. Specifically, using dependence dynamics and network analysis on a bivariate basis, we identify volatility and contagion risk among stock markets during the COVID-19 pandemic. The empirical findings add to the existing body of literature, given that previous work has not placed emphasis on network topologic metrics when it comes to financial networks, specifically during the COVID-19. The evidence shows instant financial contagion a result of the lockdown and the spread of the novel coronavirus. The methodological framework outlines important information for investors and policymakers on using financial networks to improve portfolio selection, by placing an emphasis on assets according to centrality.

本文研究了新冠疫情对51个主要股票市场(包括新兴市场和发达市场)的影响。我们分离出了易受冲击传导影响的国家,并评估了封锁期间具有免疫力的国家。具体而言,我们基于双变量使用依赖动态和网络分析,确定了新冠疫情期间股票市场之间的波动性和传染风险。鉴于以往的研究在涉及金融网络时,尤其是在新冠疫情期间,没有强调网络拓扑指标,因此实证结果丰富了现有文献。证据表明,封锁和新型冠状病毒的传播导致了即时金融传染。该方法框架为投资者和政策制定者提供了重要信息,即通过根据中心性对资产进行重点关注,利用金融网络来改善投资组合选择。