Leibinger Anna, Huizinga Oliver, Emmert-Fees Karl, Pedron Sara, Laxy Michael, Rehfuess Eva, Burns Jacob, von Philipsborn Peter

Chair of Public Health and Health Services Research, Institute of Medical Information Processing, Biometry and Epidemiology (IBE), Faculty of Medicine, LMU Munich, Munich, Germany.

Pettenkofer School of Public Health, Munich, Germany.

BMC Public Health. 2025 Jun 5;25(1):2106. doi: 10.1186/s12889-025-23331-w.

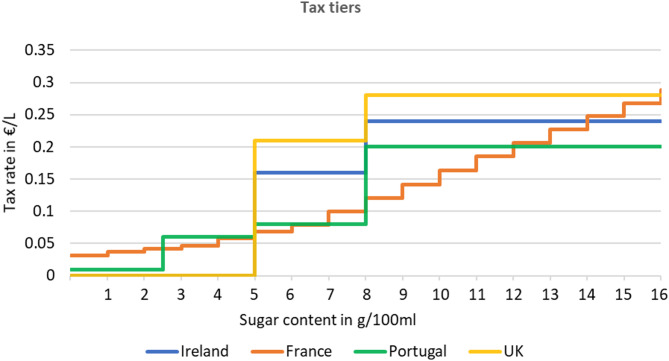

High sugar intake from soft drinks is associated with increased risk of non-communicable diseases. Tiered soft drink taxes applying higher tax rates on beverages with higher sugar content have been used to incentivize producers to reduce sugar content of soft drinks. This study assesses the impact of tiered soft drink taxes in four European countries on the sugar content of soft drinks.

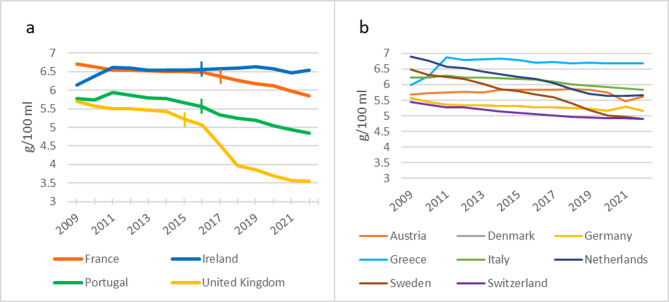

We used annual sales data from 12 countries from Euromonitor International for 2009 to 2022 to estimate the effect of tiered soft drink taxes in France, Ireland, Portugal, and the United Kingdom (UK) on soft drinks' mean annual sales-weighted sugar content. We conducted a quasi-experimental study, applying a synthetic control approach in which we used a weighted combination of eight European countries without a soft drink tax serving as control for the four intervention countries.

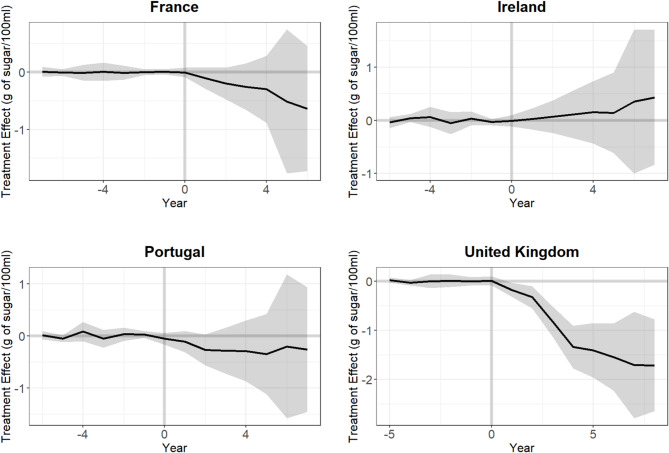

France, Portugal, and the UK exhibited negative estimated treatment effects, indicating a reduction in average sugar content in these countries. The UK demonstrated the largest estimated effect (-1.7 g sugar/100 ml; 95%-CI: -2.6; -0.8), followed by France (-0.6; 95%-CI: -1.7; 0.4) and Portugal (-0.3; 95%-CI: -1.5; 1.0). Ireland (0.4; 95%-CI: -0.8; 1.7) displayed effects in the opposite direction. Results of the sensitivity analyses indicate that results are robust concerning assumptions underlying the study design and analysis strategy.

Varying effect sizes emphasize the importance of considering specific tax design, co-interventions and contextual factors when implementing tax policies. Further research could help to shed light on these variations and to achieve a higher level of accuracy and precision in the effect estimates.

软饮料中的高糖摄入与非传染性疾病风险增加有关。分级软饮料税对含糖量较高的饮料适用更高的税率,已被用于激励生产商降低软饮料的含糖量。本研究评估了四个欧洲国家的分级软饮料税对软饮料含糖量的影响。

我们使用了欧睿国际提供的2009年至2022年12个国家的年度销售数据,以估计法国、爱尔兰、葡萄牙和英国的分级软饮料税对软饮料年平均销售加权含糖量的影响。我们进行了一项准实验研究,采用合成控制法,其中我们使用了八个没有软饮料税的欧洲国家的加权组合作为四个干预国家的对照。

法国、葡萄牙和英国呈现出负的估计处理效应,表明这些国家的平均含糖量有所降低。英国的估计效应最大(-1.7克糖/100毫升;95%置信区间:-2.6;-0.8),其次是法国(-0.6;95%置信区间:-1.7;0.4)和葡萄牙(-0.