Department of Agricultural and Resource Economics, Rudd Center for Food Policy & Health, University of Connecticut, Hartford.

The Heller School for Social Policy and Management, Brandeis University, Waltham, Massachusetts.

JAMA Netw Open. 2022 Jun 1;5(6):e2215276. doi: 10.1001/jamanetworkopen.2022.15276.

More than 45 countries and several local jurisdictions have implemented sugar-sweetened beverage (SSB) taxes to improve nutrition and population health, and evidence on their outcomes to date is essential to inform policy discussions. Responding to this need, the World Health Organization commissioned a systematic literature review on the outcomes of fiscal policies, including SSB taxes.

To assess the associations of implemented SSB taxes with prices, sales, consumption, diet, body weight, product changes, unintended consequences, health, and pregnancy outcomes.

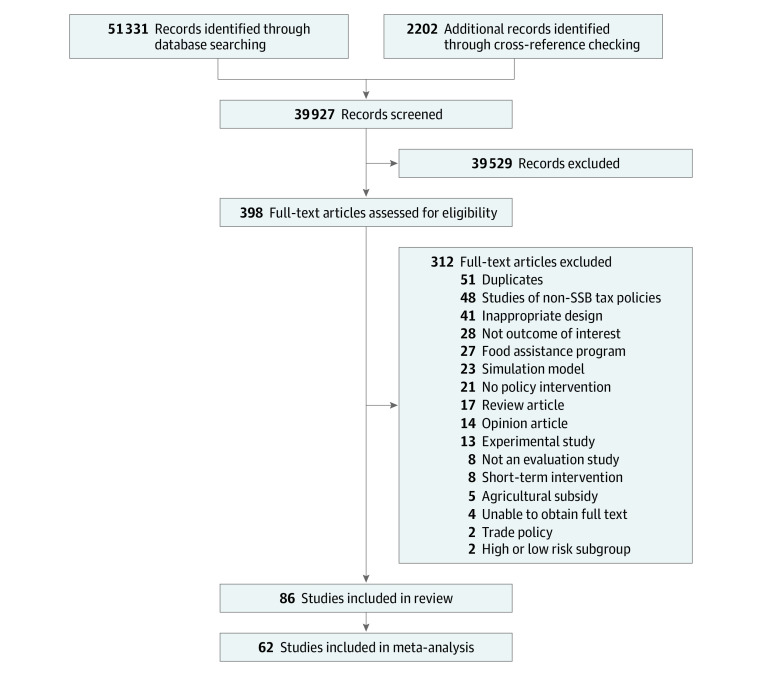

Searches of 8 bibliographic databases (Business Source Complete, Cochrane Central Register of Controlled Trials, Cochrane Database of Systematic Reviews, CINAHL, EconLit, PsycINFO, PubMed, and Scopus) were performed from database inception through June 1, 2020, with no language or setting restrictions. Grey literature was assessed using 14 sources and government websites.

The review included primary studies of implemented SSB taxes.

The review followed the Preferred Reporting Items for Systematic Reviews and Meta-analyses guidelines. For prices, sales and consumption, results were meta-analyzed using a 3-level random-effects model. Study quality was assessed at the outcome level.

Tax pass-through rate for prices, percentage reduction in SSB demand, and price elasticity of demand for sales and consumption. Heterogeneity was assessed using τ2 and the I2 statistic.

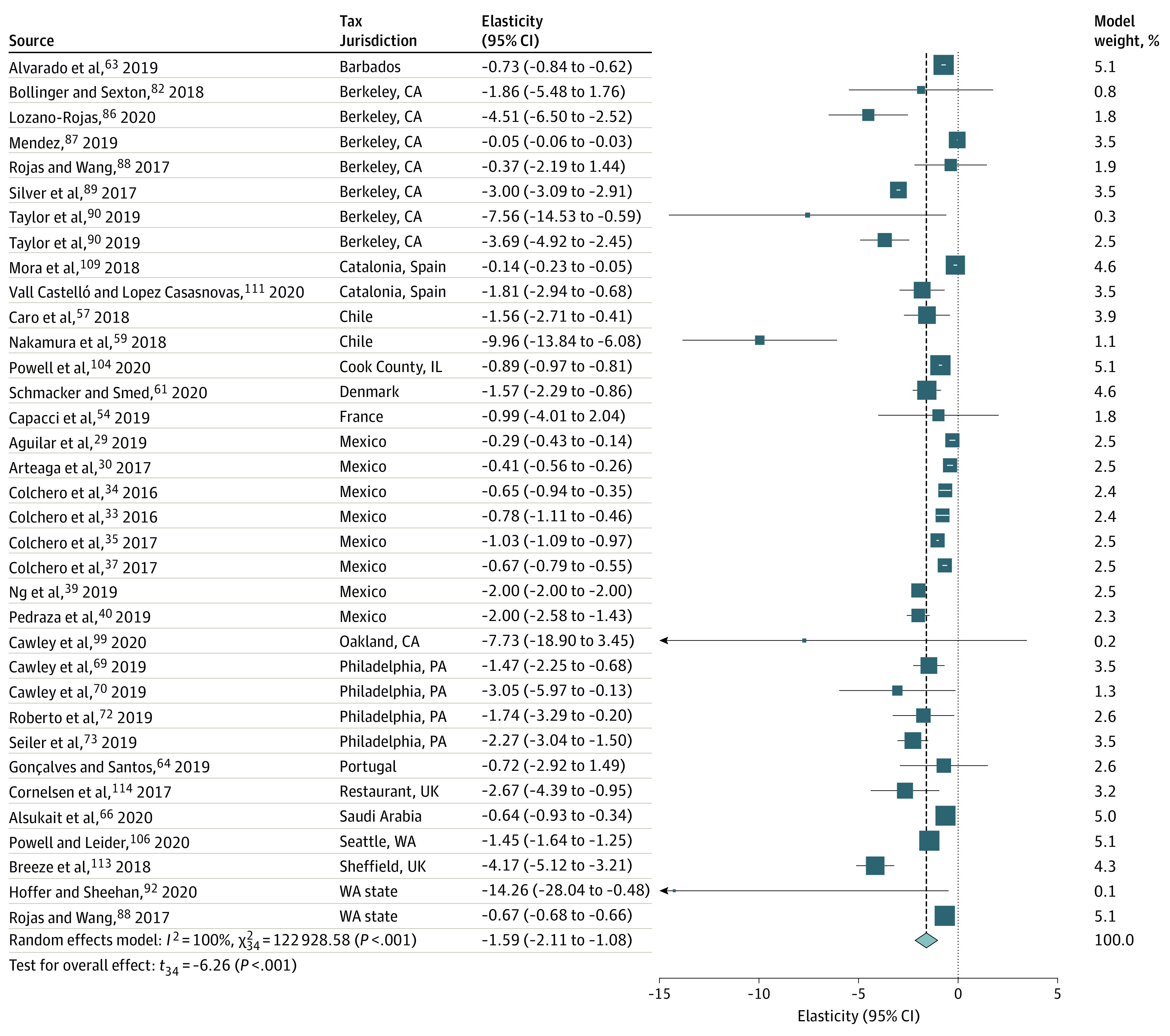

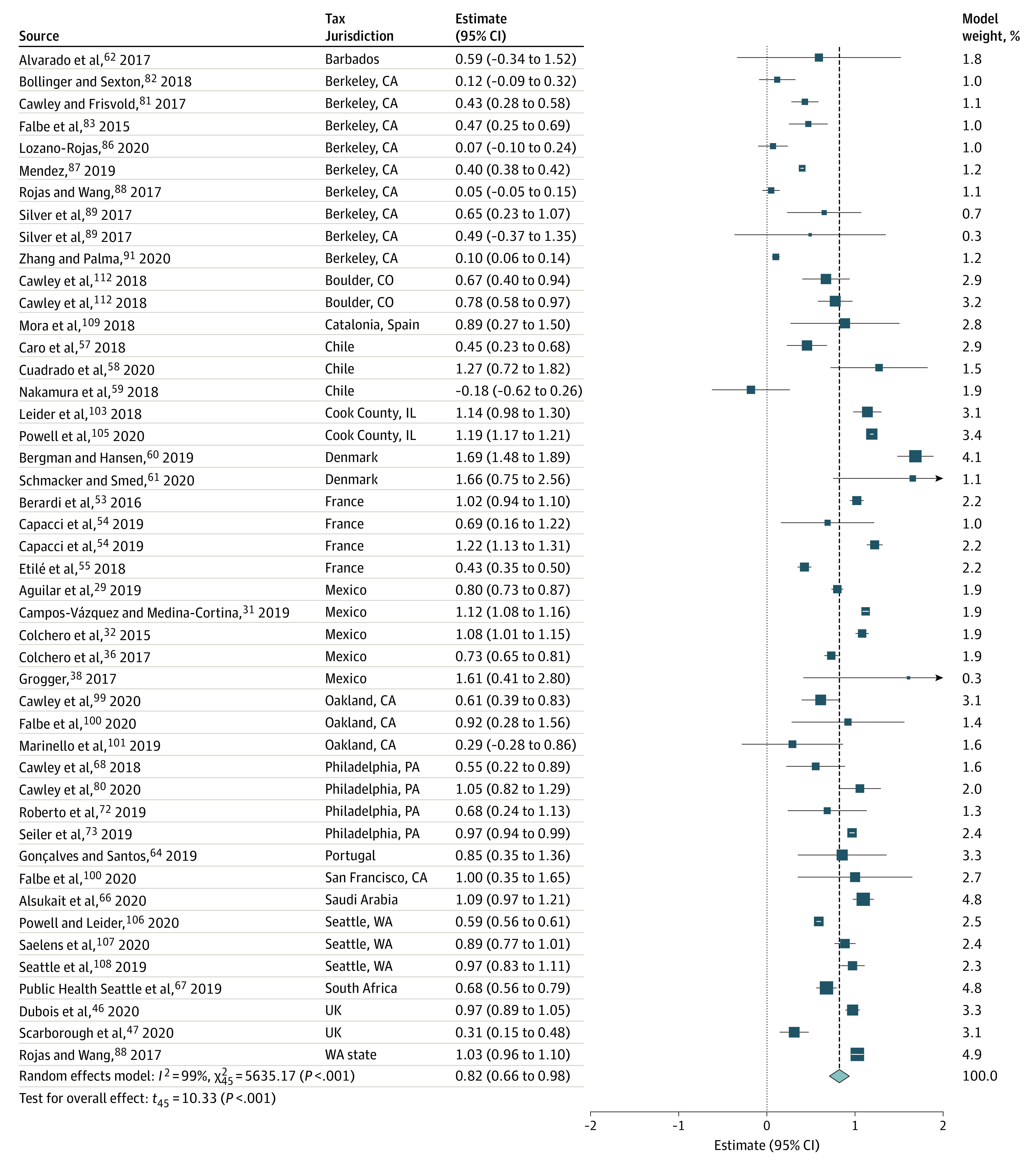

A total of 86 articles were eligible, with 62 studies contributing to the meta-analysis. The overall tax pass-through rate was 82% (95% CI, 66% to 98%; P < .001, I2 = 99%), suggesting tax undershifting. The demand for SSBs was highly sensitive to tax-induced price increases, with the price elasticity of demand of -1.59 (95% CI, -2.11 to -1.08; P < .001; I2 = 100%) and a mean reduction in SSB sales of 15% (95% CI, -20% to -9%; P < .001; I2 = 100%). There was no evidence of substitution to untaxed beverages, and changes in SSB consumption were not significant. The narrative synthesis found reformulation and reduced sugar content of taxed beverages for tiered taxes, cross-border shopping in most studies of local-level taxes, and no negative changes in employment. Data on the heterogeneity of SSB tax outcomes across subpopulations were limited.

In this systematic review and meta-analysis of implemented SSB taxes worldwide, SSB taxes were associated with higher prices and lower sales of taxed beverages.

超过 45 个国家和几个地方司法管辖区已实施含糖饮料(SSB)税以改善营养和人口健康,因此,了解这些政策的结果对于推动政策讨论至关重要。为满足这一需求,世界卫生组织委托进行了一项关于财政政策(包括 SSB 税)结果的系统文献综述。

评估实施的 SSB 税与价格、销售、消费、饮食、体重、产品变化、意外后果、健康和妊娠结果之间的关联。

从数据库创建到 2020 年 6 月 1 日,对 8 个书目数据库(商业来源完整、考科蓝中心对照试验注册、考科蓝系统评价数据库、CINAHL、经济学摘要、心理文摘、PubMed 和 Scopus)进行了搜索,没有语言或设置限制。使用 14 个来源和政府网站评估灰色文献。

该综述纳入了实施 SSB 税的主要研究。

该综述遵循系统评价和荟萃分析的首选报告项目准则。对于价格、销售和消费,使用 3 级随机效应模型对结果进行了荟萃分析。在结果层面评估了研究质量。

价格的税收传递率、SSB 需求减少的百分比以及销售和消费的需求价格弹性。使用 τ2 和 I2 统计量评估异质性。

共有 86 篇文章符合条件,其中 62 项研究为荟萃分析提供了数据。总体税收传递率为 82%(95%置信区间,66%至 98%;P<0.001,I2=99%),表明税收转移不足。SSB 的需求对税收引起的价格上涨非常敏感,需求价格弹性为-1.59(95%置信区间,-2.11 至-1.08;P<0.001;I2=100%),SSB 销售额平均减少 15%(95%置信区间,-20%至-9%;P<0.001;I2=100%)。没有证据表明替代未征税饮料,SSB 消费的变化并不显著。叙述性综述发现,分层税会使征税饮料的配方和含糖量降低,地方一级税收的大多数研究中会出现跨境购物,而且就业没有负面变化。关于 SSB 税结果在亚人群中的异质性的数据有限。

在这项对全球实施的 SSB 税的系统评价和荟萃分析中,SSB 税与征税饮料价格上涨和销售下降有关。