Guindon G Emmanuel, Fatima Tooba, Li David X, Joukova Alexandra, Sudhir Jitender, Mishra Sujata, Chaloupka Frank J, Jha Prabhat

Centre for Health Economics and Policy Analysis, McMaster University, Hamilton, Ontario, L8S 4K1, Canada.

Department of Health Research Methods, Evidence, and Impact, McMaster University, Hamilton, Ontario, L8S 4K1, Canada.

Gates Open Res. 2019 Jan 17;3:8. doi: 10.12688/gatesopenres.12894.1.

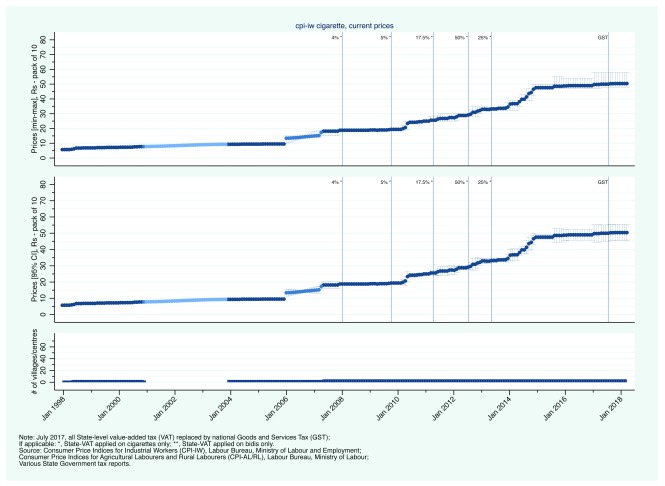

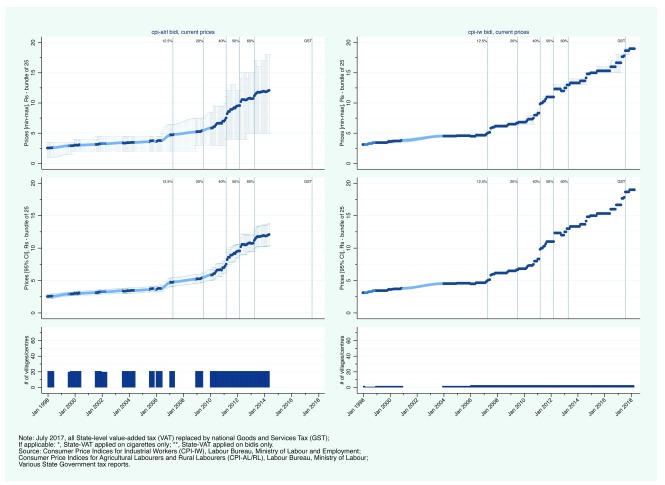

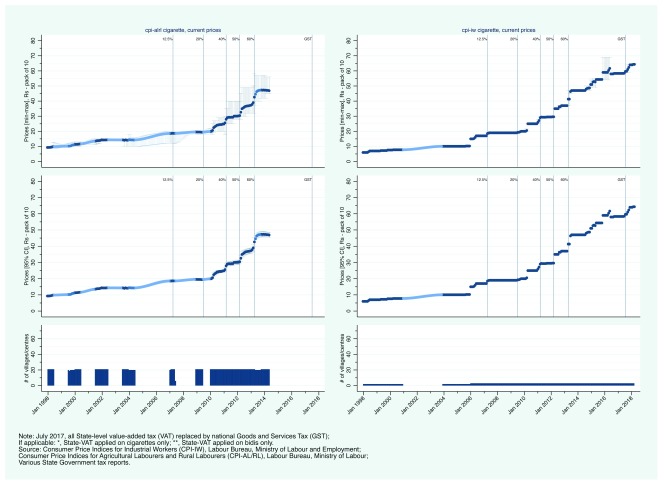

Tobacco smoking remains a leading risk factor for disease burden globally. In India alone, about 1 million deaths are caused annually by smoking. Although increasing tobacco prices has consistently been found to be the most effective intervention to reduce tobacco use, the documentation of prices and taxes across time and space has not been an essential component of tobacco control surveillance in most jurisdictions. This study aimed to examine, using graphical methods, trends in smoking tobacco taxes and prices in India at national and state-level. We used retail prices, price indices, and unit values (household expenditures on a commodity divided by the quantity purchased) collected and reported by government agencies. For bidis and cigarettes, we examined current and real (inflation-adjusted) prices, affordability (cost in terms of income), and key tax changes at both national and state-level. We show that real prices of bidis and cigarettes were relatively flat (even decreasing in the case of bidis) between 2000 and 2007, and clearly increasing from 2010. When rising income is taken into account, however, both cigarettes and bidis have become more affordable since 2000. We found that some but not all tax changes were accompanied by price changes and in particular, that tax decreases did not result in price decreases. It is feasible to evaluate tax and price policies at national and regional level using routinely collected data.

吸烟仍然是全球疾病负担的主要风险因素。仅在印度,每年就有约100万人因吸烟死亡。尽管一直以来提高烟草价格被认为是减少烟草使用最有效的干预措施,但在大多数司法管辖区,跨时空记录价格和税收并非烟草控制监测的重要组成部分。本研究旨在运用图表方法,考察印度全国及各邦层面烟草税和价格的趋势。我们使用了政府机构收集和报告的零售价格、价格指数及单位价值(家庭在某一商品上的支出除以购买数量)。对于比迪烟和香烟,我们考察了全国及各邦层面的当前价格和实际(经通胀调整)价格、可承受性(以收入衡量的成本)及关键税收变化。我们发现,2000年至2007年间,比迪烟和香烟的实际价格相对平稳(比迪烟甚至有所下降),2010年起则明显上涨。然而,考虑到收入增长,自2000年以来,香烟和比迪烟都变得更具可承受性。我们发现部分而非所有税收变化都伴随着价格变化,特别是税收降低并未导致价格下降。利用常规收集的数据评估国家和地区层面的税收及价格政策是可行的。