Ahundjanov Behzod B, Akhundjanov Sherzod B, Okhunjanov Botir B

Department of Economics, Bucknell University, 1 Dent Drive, Lewisburg, PA 17837, USA.

Department of Applied Economics, Utah State University, 4835 Old Main Hill, Logan, UT 84322-4835, USA.

Entropy (Basel). 2020 Jul 20;22(7):791. doi: 10.3390/e22070791.

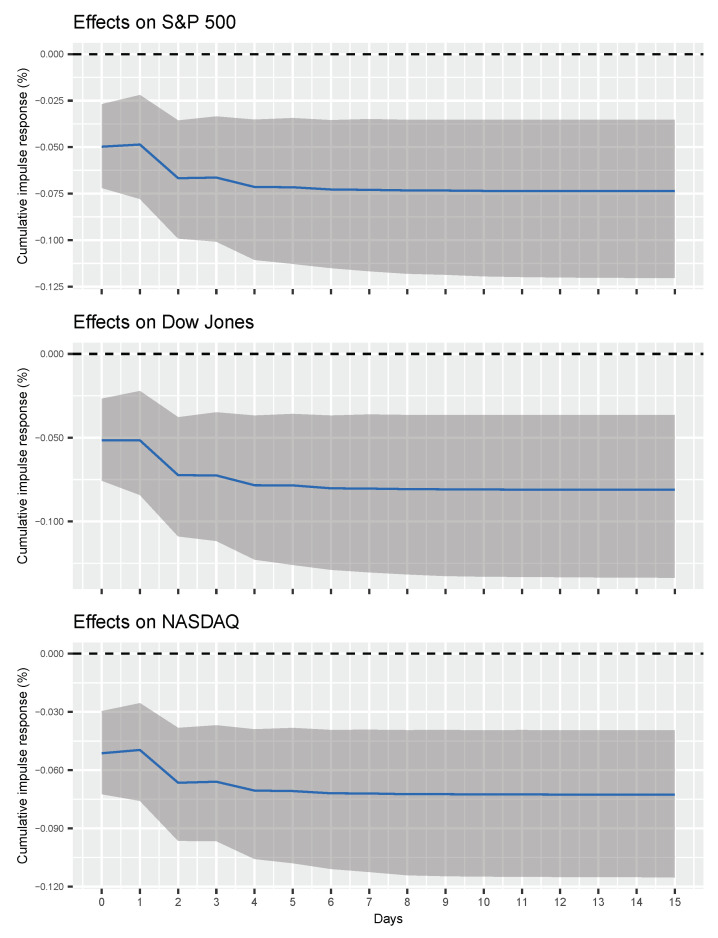

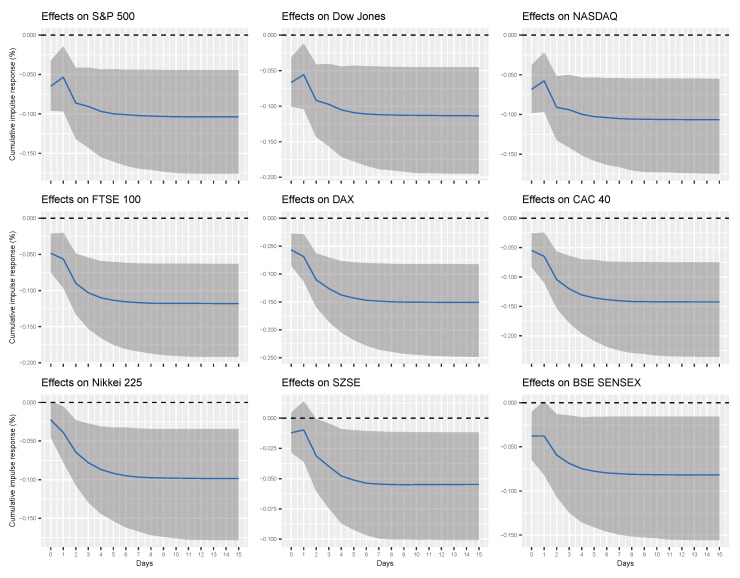

The discovery and sudden spread of the novel coronavirus (COVID-19) exposed individuals to a great uncertainty about the potential health and economic ramifications of the virus, which triggered a surge in demand for information about COVID-19. To understand financial market implications of individuals' behavior upon such uncertainty, we explore the relationship between Google search queries related to COVID-19-information search that reflects one's level of concern or risk perception-and the performance of major financial indices. The empirical analysis based on the Bayesian inference of a structural vector autoregressive model shows that one unit increase in the popularity of COVID-19-related global search queries, after controlling for COVID-19 cases, results in 0.038 - 0.069 % of a cumulative decline in global financial indices after one day and 0.054 - 0.150 % of a cumulative decline after one week.

新型冠状病毒(COVID-19)的发现和迅速传播,使人们对该病毒可能产生的健康和经济影响面临极大的不确定性,这引发了对COVID-19相关信息的需求激增。为了理解个体在这种不确定性下的行为对金融市场的影响,我们探究了与COVID-19信息搜索相关的谷歌搜索查询(反映一个人的关注程度或风险感知水平)与主要金融指数表现之间的关系。基于结构向量自回归模型的贝叶斯推断进行的实证分析表明,在控制了COVID-19病例数之后,与COVID-19相关的全球搜索查询热度每增加一个单位,全球金融指数在一天后会累计下跌0.038 - 0.069%,一周后会累计下跌0.054 - 0.150%。