Chahuán-Jiménez Karime, Rubilar Rolando, de la Fuente-Mella Hanns, Leiva Víctor

Escuela de Auditoría, Centro de Investigación en Negocios y Gestión Empresarial, Facultad de Ciencias Económicas y Administrativas, Universidad de Valparaíso, Valparaíso 2362735, Chile.

Instituto de Estadística, Facultad de Ciencias, Universidad de Valparaíso, Valparaíso 2360102, Chile.

Entropy (Basel). 2021 Jan 12;23(1):100. doi: 10.3390/e23010100.

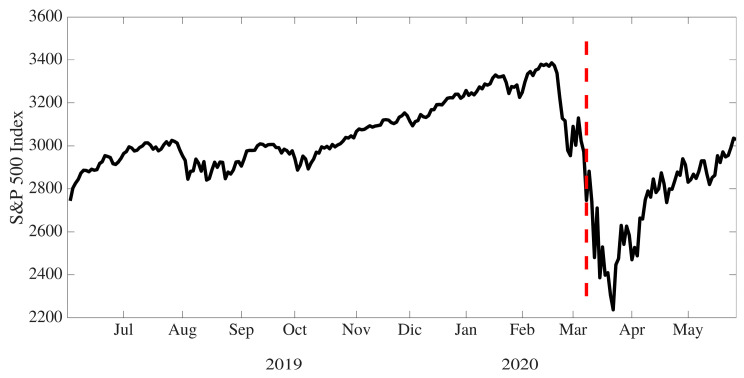

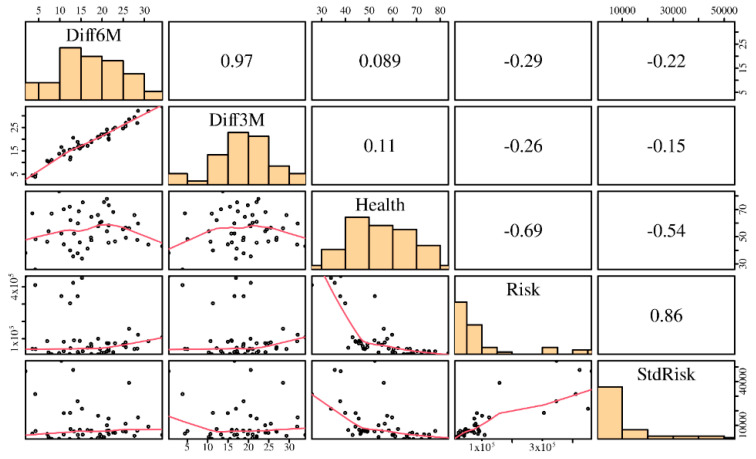

In this research, statistical models are formulated to study the effect of the health crisis arising from COVID-19 in global markets. Breakpoints in the price series of stock indexes are considered. Such indexes are used as an approximation of the stock markets in different countries, taking into account that they are indicative of these markets because of their composition. The main results obtained in this investigation highlight that countries with better institutional and economic conditions are less affected by the pandemic. In addition, the effect of the health index in the models is associated with their non-significant parameters. This is due to that the health index used in the modeling would not determine the different capacities of the countries analyzed to respond efficiently to the pandemic effect. Therefore, the contagion is the preponderant factor when analyzing the structural breakdown that occurred in the world economy.

在本研究中,构建了统计模型以研究新冠疫情引发的健康危机对全球市场的影响。考虑了股票指数价格序列中的断点。这些指数被用作不同国家股票市场的近似值,因为考虑到它们的构成能反映这些市场。本次调查获得的主要结果表明,制度和经济条件较好的国家受疫情影响较小。此外,模型中健康指数的影响与其不显著的参数相关。这是因为建模中使用的健康指数无法确定所分析国家有效应对疫情影响的不同能力。因此,在分析世界经济中发生的结构性崩溃时,传染是首要因素。