Mattingly T Joseph, Sahu Maitreyi, Anderson Kelly E

Department of Pharmacotherapy, University of Utah College of Pharmacy, Salt Lake City.

Department of Health Metrics Sciences, University of Washington, Seattle.

JAMA Health Forum. 2025 Aug 1;6(8):e251988. doi: 10.1001/jamahealthforum.2025.1988.

While community pharmacies provide many valuable prescription and professional services, they are also retail businesses. Evaluating pharmacy closures through the lens of a retail business framework may provide more context on what is happening in this industry and identify potential solutions to address closures and/or shortages.

To evaluate community pharmacy turnover (openings and closings) in the US over time and by ownership type.

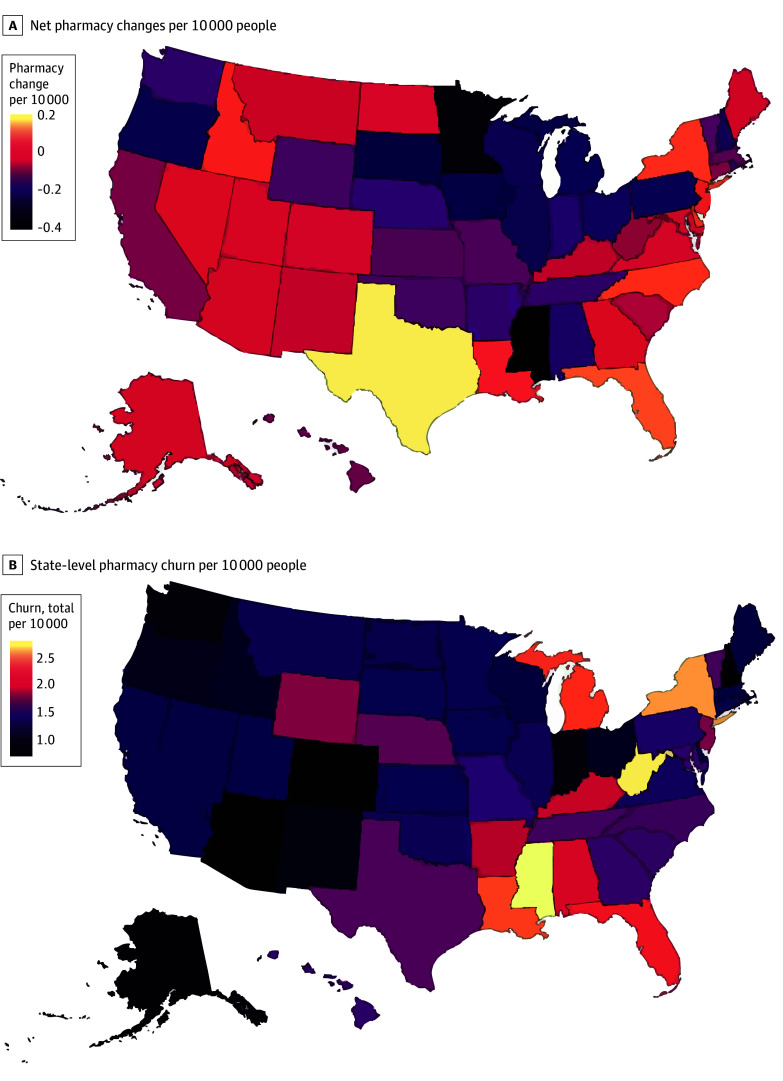

This cross-sectional analysis of all community pharmacy openings and closings in the US from 2010 to 2023 used pharmacy-level data from the US National Council for Prescription Drug Programs database. National-, state-, and county-level turnover was assessed using economic indicators of business dynamics, such as total population, population growth, household income, total firm changes for all industries, and net job creation.

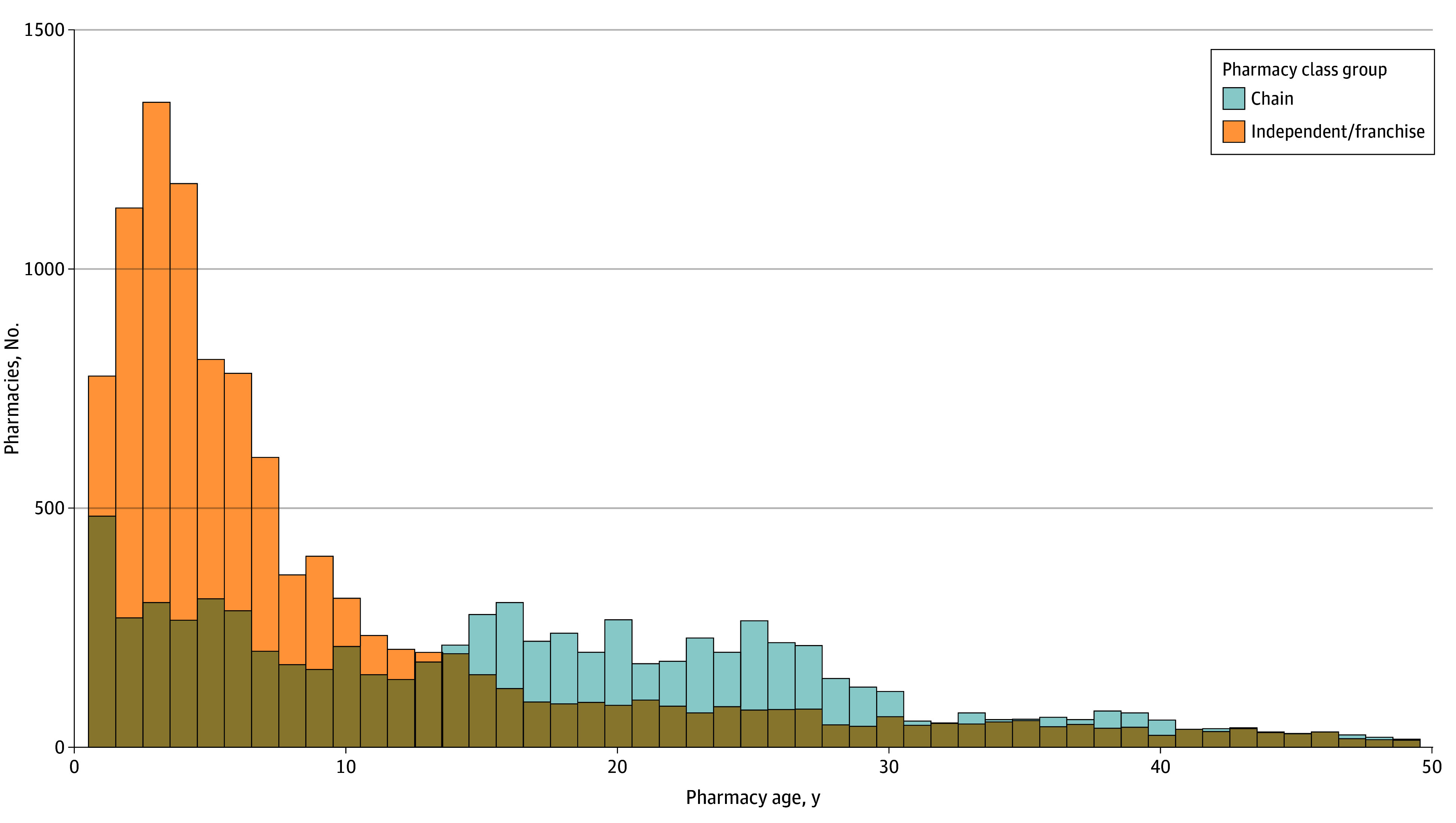

Pharmacy class type defined as either a chain pharmacy (4 or more pharmacies under common ownership) or an independent or franchise pharmacy using the US National Council for Prescription Drug Programs classifications.

Pharmacy turnover rate from 2010 to 2023, calculated as the sum of pharmacy openings and closings over the full study period divided by the total pharmacies in the market at the beginning of the period (2010).

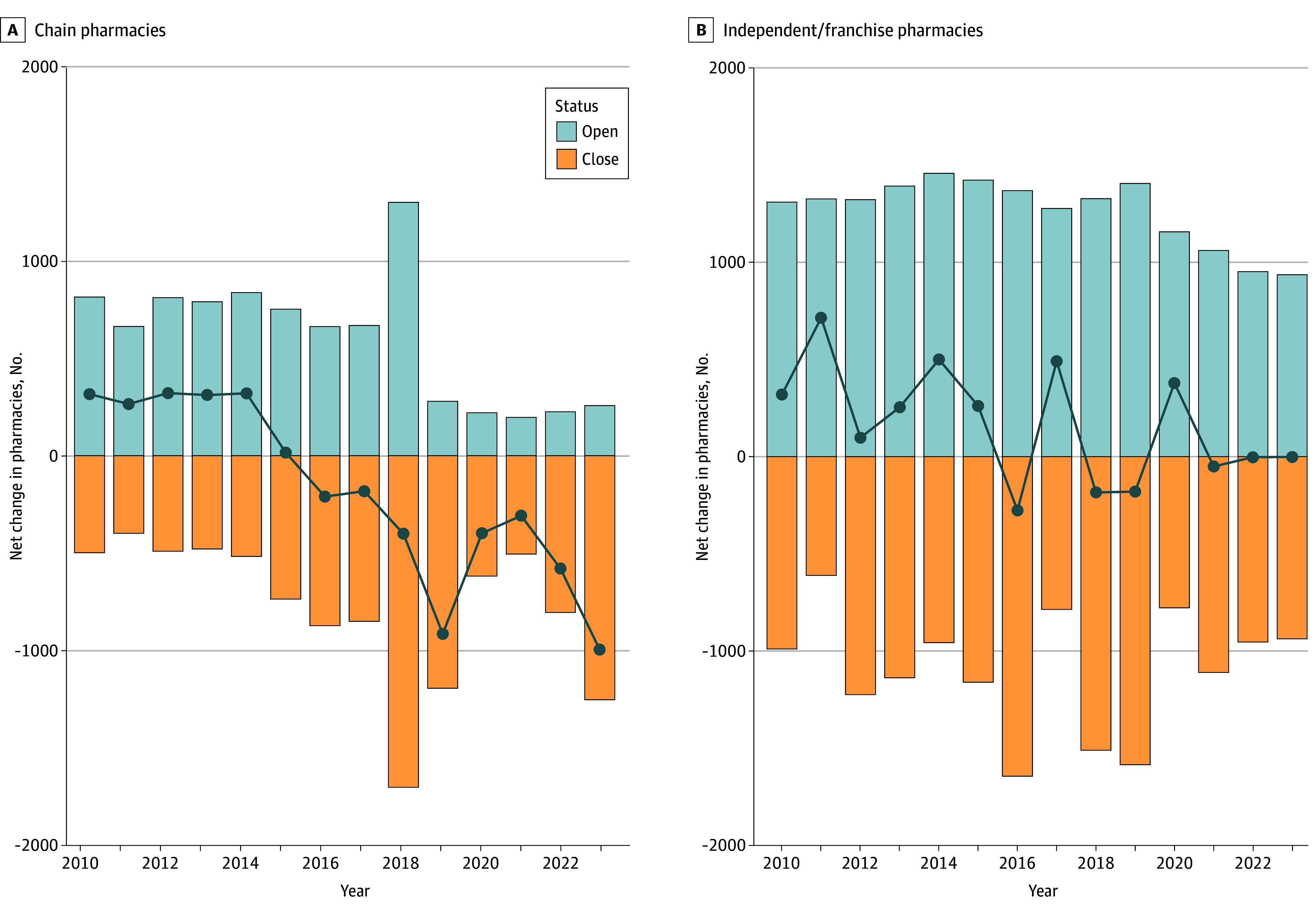

The analyses found that US pharmacy market turnover rate for this 14-year period was 86.8% (52 974 total openings and closures of 61 054 total pharmacies in 2010) or 6.2% annually. When comparing across pharmacy types, independent pharmacy turnover was substantially higher (152.7%) than chain pharmacy turnover (49.9%) across the entire US. Counties with high turnover were associated with net increases in pharmacies from more independent pharmacy openings over the period. Turnover rates for all businesses were higher in counties with both low and high pharmacy turnover, even when adjusting for population size.

This cross-sectional study found that the community pharmacy market in the US has an annual turnover rate of approximately 6.2%, with independent pharmacies opening and closing more frequently than chain pharmacies.

虽然社区药房提供许多有价值的处方药和专业服务,但它们也是零售企业。通过零售业务框架的视角评估药房关闭情况,可能会为该行业正在发生的事情提供更多背景信息,并确定解决关闭和/或短缺问题的潜在解决方案。

评估美国社区药房随时间推移以及按所有权类型划分的营业额(开业和关闭情况)。

这项对2010年至2023年美国所有社区药房开业和关闭情况的横断面分析,使用了来自美国国家处方药计划委员会数据库的药房层面数据。利用商业动态的经济指标,如总人口、人口增长、家庭收入、所有行业的企业总变化以及净就业创造,评估国家、州和县层面的营业额。

药房类别类型,根据美国国家处方药计划委员会的分类,定义为连锁药房(共同所有权下有4家或更多药房)或独立或特许经营药房。

2010年至2023年的药房周转率,计算方法为整个研究期间药房开业和关闭的总数除以该时期开始时(2010年)市场上的药房总数。

分析发现,在这14年期间,美国药房市场的周转率为86.8%(2010年61054家药房中,开业和关闭总数为52974家),即每年6.2%。在比较不同药房类型时,整个美国独立药房的周转率(152.7%)大幅高于连锁药房的周转率(49.9%)。周转率高的县在此期间因更多独立药房开业而药房数量净增加。即使在调整人口规模后,药房周转率低和高的县所有企业的周转率都更高。

这项横断面研究发现,美国社区药房市场的年周转率约为6.2%,独立药房的开业和关闭比连锁药房更频繁。